GameStop May Not Be a Worthy Investment, But It Is Certainly a Tradable Stock

You might be a little shocked to learn just how well-managed the company's balance sheet is.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday evening, former meme trading darling GameStop GME released its fiscal fourth-quarter financial results.

For the three-month period ended February 3, GameStop posted GAAP EPS of $0.21 (adjusted EPS of $0.22) on revenue of $1.794B. These top and bottom-line results both fell well short of expectations, while the sales print reflected a year-over-year contraction of 19.7%.

The lone bright spot would be that the EPS print of $0.21 was actually up from $0.16 for the year-ago comparison. For the full year, GameStop's GAAP EPS improved to $0.02 from a loss of $1.03. So, there is something positive here.

As for quarterly operations, as revenue contracted 19.7%, the cost of sales decreased to $1.374B (-20.4%). This left a gross profit of $419.2M, down 16% from $499.8M for the year-ago period. GAAP gross margin did improve to 23.4% from 22.5%. Operating expenses dropped 20.8% to $359.2M.

After accounting for 44.8M in asset impairments, GAAP operating income actually improved to $55.2M (+19.5%). Once we work through interest and taxes, the firm's GAAP net income printed at $63.1M, which was up 30.9% from the year-ago comparison. Not all that bad for a company that suffered a 19.7% decrease in sales.

Sales Mix

- Hardware & Accessories generated net sales of $1.095B (-11.9%), comprising 61% of total sales, up from 55.8%.

- Software generated net sales of $465.3M (-30.6%), comprising 26% of total sales, down from 30.1%.

- Collectibles generated net sales of $233.7M (-25.4%), comprising 13% of total sales, down from 14.1%.

Fundamentals

For the quarter reported, GameStop generated operating cash flow of $11M. Tack on Capex spending of $7.7M and the firm was left with free cash flow of -$18.7M, down from a whopping $326.6M in free cash for the year-ago quarter. Full-year free cash flow dropped -$238.6M from $52.3M. That's not good. It obviously does not return capital to shareholders.

Checking out the balance sheet, GameStop ended the period with a cash position of $1.199B, which was down from a year ago by a little less than the cash burn expressed in the full-year free cash flow print mentioned above. Inventories stand at $632.5M (-7.3%), leaving current assets at $1.974B. Current liabilities add up to $934.5M, including just $10.8M in shorter-term debt. This puts the firm's current ratio at 2.11, which is very strong. Its quick ratio stands at 1.43, which is also strong.

Total assets amount to $2.709B, including absolutely no goodwill or any other intangible asset. Total liabilities less equity comes to $1.37B, including long-term debt of just $17.7M.

Folks who do not follow GameStop very closely or just think of the name as a business in decline or the stock as a meme stock, are probably a little shocked to learn just how well-managed this balance sheet is. That long-term debt is limited to a low-interest, unsecured term loan associated with the French government's response to the pandemic. Otherwise, there would be no long-term debt on the books.

Wall Street

Analyst Michael Pachter of Wedbush is rated at one star out of five by TipRanks, but may be the only analyst on Wall Street still covering GameStop. In response to these earnings, Pachter reiterated both his "sell" rating and $6 target price on GME.

Pachter was blunt in his assessment of the firm's prospects. He pointed out several sustained headwinds that are likely to impede growth. These include the many years in progress now shift in consumer preference from physical to digital game sales, the ongoing rise of subscription services, and an also likely decline in hardware sales due to advancements in game streaming technology.

Pachter also sees a lack of coherent strategy from GameStop to pivot into something new, and potentially high growth. Despite this quarter's improved profitability generated by higher-margin software sales and cost discipline, Pachter sees these problems impeding the company’s future sales performance.

My Thoughts

As has been the case since Ryan Cohen, the current Chair, has been running the firm, there is a real dearth of communication between management and shareholders. Again, no conference call. That said, the strength of the balance sheet and Cohen's continued involvement are positives. So is the improved cost discipline.

The stock was down more than 12% on Wednesday evening's release. It's awfully hard to forget, though, that about 22.5% of the stock's entire float is still held in short positions.

I do not think GME is a worthy investment unless its core business changes, or it changes its core business. We know that GME has tried to shift in a few directions now, and they have not really turned into anything sustainable.

The stock is tradable. With so many shares still short, I can see buying some shares on this dip, with a short-term horizon.

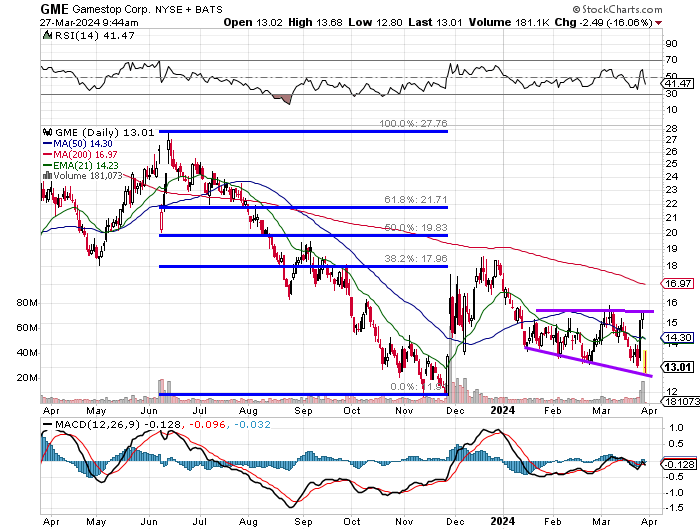

Readers will see that late last year GME hit resistance at a rough 38.2% Fibonacci retracement of the stock's June through late November selloff. Since about mid-January, GME has formed a descending, broadening wedge that suggests stiff resistance around $15.85.

That's your pivot, if you're long the shares. This pattern also suggests support just about where the stock is trading now. Either support breaks here and it gets really ugly, or the short sellers start covering here at support. That's the idea that I'm leaning towards.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.