FIVE Is Way Below But It's Also Nearly a Buy

I'm bargain hunting right now, and waiting for the moment to pounce.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Five Below FIVE is trading down around 20%. I saw shares before the open bouncing around with an $86 handle after going out last night at $102.07. These shares had traded with a $212 handle as recently as March. What happened? Earnings? Not quite, though earnings have and will matter to how this story came about. Five Below, for those unaware, is a Philadelphia-based specialty value retailer targeting the tween and teen demographics, selling a variety of varied products for between $1 and $5.

After the close on Tuesday, the company announced that total sales for the 10-week period ended July 13 had increased by 9.5% vs. the year-ago similar period. But FIVE

now expects second-quarter sales ending Aug. 3 to land in a range spanning from $820 million to $826 million. The retailer had previously provided guidance of $830 million to $850 million. Wall Street was looking for something close to $836 million. Additionally, FIVE is now expecting to see comparable sales for the quarter decrease by 6% to 7%, while producing diluted earnings per common share of $0.53 to $0.56. It had previously guided the quarter's earnings per share toward $0.57 to $0.69, with Wall Street looking for a rough $0.62.

The 'Sack' Exchange

That's not all. Tuesday afternoon it was revealed that CEO Joel Anderson had stepped down from his roles as president and CEO and from the board to pursue other interests. Yeah, that's precisely when I pursue other interests, as my company issues a pre-earnings warning. It's not being said, but one can't help but wonder if the "stepping down" was more of a "kicking out." Remember, first-quarter earnings were pretty awful as well.

Running of the Bull

Kenneth Bull will now act as interim president and CEO, effective immediately and the board has already launched an executive search for a permanent replacement for Anderson. Thomas Vellios, who is a co-founder and former CEO, and had been serving as non-executive chairman of late, will assume the role of executive chairman, also on an interim basis in support of Bull as Bull tries to move the firm through this period of transition.

Fundamentally Speaking...

With earnings expected out Aug. 30, let's check the numbers. Over the 12 trailing months ended in February, FIVE had posted free cash flow of about $23 million. Not great, but not negative. The balance sheet showed a cash position of $369.6 million, inventories of $630 million and current assets of $1.15 billion. Current liabilities added up to $741.6 million, including no short-term debt, but about $292 million in short-term lease obligations. That puts the firm's current and quick ratios at 1.55 and 0.7. Both are really rather healthy for a retailer, though the true value of those inventories is probably questionable, given that sales are running below expectations.

Total assets amounted to $3.947 billion, which to the company's credit, included no goodwill or any other kind of intangibles. Total liabilities less equity amounted to $2.363 billion, which again is heavily composed of lease obligations. There is no long-term debt, either. Sales might have suffered, but there is cash flow, and the balance sheet was well-managed.

My Take

I like companies with clean balance sheets. I like companies with positive free cash flow. I like companies with current ratios that start out with a full digit. I also like companies that have kept their debt-load under control and really, really like ones that run with no debt. Five Below is all of these things.

Readers may have noticed that analysts from Mizuho Securities, Evercore ISI, Truist, Morgan Stanley, Citigroup, and William Blair have all downgraded their ratings on FIVE from "buy" to something lower than "buy. Readers may have noticed that analysts from both Bank of America and JP Morgan significantly reduced their target prices for the name. Follow along. The algorithms certainly will.

Don't forget, these folks copy each other's homework and none of them foresaw the issues now facing Five Blow. I do not want to buy this dip just yet. I want to let Wall Street have their little tantrum. Let the algos do what they must.

I expect to buy this dip once I'm convinced that this dip might have reached a point of stabilization. That might be later today. That might be later this week. I am not in the habit of trying to catch falling knives. I do like, however, when I smell panic at the "no skin in the game" broker / dealers who just want out.

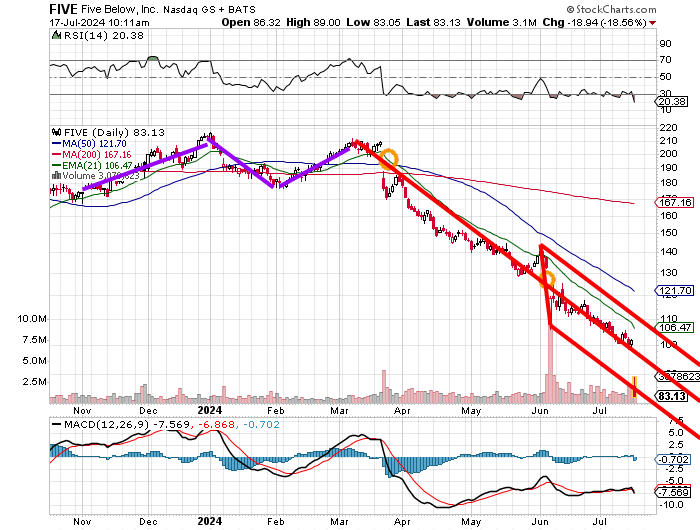

Readers will note that late 2023 into early 2024, FIVE suffered a double-top reversal and it has been all downhill from there. The stock has surrendered a rough 61% since that second top in March. Today creates a third unfilled gap on the way down as well. The stock now flirts with cracking the lower trendline of our Pitchfork model after having slid atop the central trendline for months.

Relative strength had been on the verge of being technically oversold. Now, there is no doubt. The daily moving average convergence divergence indicator has looked terribly bearish since late March. Nothing new there. This chart is ugly as heck.

My guess is that Bull and Vellios find a way to engineer a modified beat in late August or at least come up with something positive to say. Five Below is closer to being a buy, in my opinion, than it has been in a long while. Right now, I'm thinking about writing Oct. 18 $75 puts for about $6.60 and purchasing October 18th $65 puts for roughly $3.50 just so I don't get my face ripped off.

That would pay me a net credit of $3.10 in premiums now and expose me to potentially being long the shares in mid-October at a net basis of $71.90. Should the stock trade all the way down through my lower stock price, I would face a loss of $6.90 on the options trade. The real idea is to try to make some lunch money while I watch the equity for a potential basing process. Of course, prices will change, and the actual trade may have to evolve by the time this piece is published, but I think you get the idea.

At the time of publication, Guilfoyle had no positions in any security mentioned.