Doug Kass: Investing in a Storm

When investors say 'times are different,' it is typically an attempt to rationalize high stock prices... and ends badly.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

If we have had one consistent message over the last two years, it is that there is a broadening list of uncertainties that could lead to a wide range of outcomes and result in lower stock market valuations.

I've compiled some of my Real Money Pro articles over the last month combined with a recent letter to my investors at my hedge fund (Seabreeze Partners), which outlines my ursine market views and attempts to deliver my honest and transparent review of how I am dealing with an extremely difficult market to navigate.

It should be clear that recent events support this message and underscore why I continue to manage my Limited Partners' capital conservatively.

"I'd keep playing, I don't think the heavy stuff is going to come down for quite a while."

-- Carl Spackler, Caddyshack (1980)

The 3 Questions

As mentioned a year ago in a monthly letter to our Limited Partners, I have three questions that I repeatedly ask myself when we invest your capital.

Unfortunately, I still don't like the answers to my questions:

1. In a paperless and cloudy world, are investors and citizens as safe as the markets assume we are?

2. In a flat, networked and interconnected world, is it even possible for America to be an "oasis of prosperity" and a driver or engine of global economic growth?

3. With the G-8's geopolitical coordination at an all-time low, how slow and inept will the reaction be if the wheels do come off?

Today there are obvious emerging and overarching levels of uncertainty that are being combined with shifting and worrisome paradigm shifts. The outcomes are potentially dangerous in an already fragile global economy filled with geopolitical strife and deep hate.

We learned a week ago, that these dangers are not restricted to the strained relationships between the U.S., China and Russia - discussed in previous notes. It provides another reminder of the expanded range of political, geopolitical, economic and market outcomes (many of them adverse), that could serve as a dampener on confidence, stability and on stock valuations.

Before discussing Seabreeze's positioning and market outlook I wanted to briefly discuss our thoughts on risk management -- a subject that is rarely discussed in hedge fund commentary.

Adhering to Strong Risk Management Remains Seabreeze's Mantra

"The first rule of an investment is don't lose [money]. And the second rule of an investment is don't forget the first rule. And that's all the rules there are."

-- Warren Buffett

Vince Lombardi, the legendary football coach of the Green Bay Packers famously said, "Winning isn't everything, it's the only thing." As it relates to managing a hedge fund, we respectfully demur from Lombardi's dictum which has been fully embraced in society.

Rather, to us, at Seabreeze, "Risk management isn't everything, it's the only thing." This is particularly true with the rising economic, political, geopolitical and policy uncertainties in an investment world dominated by passive products and strategies (e.g., risk parity) that know everything about price and nothing about value.

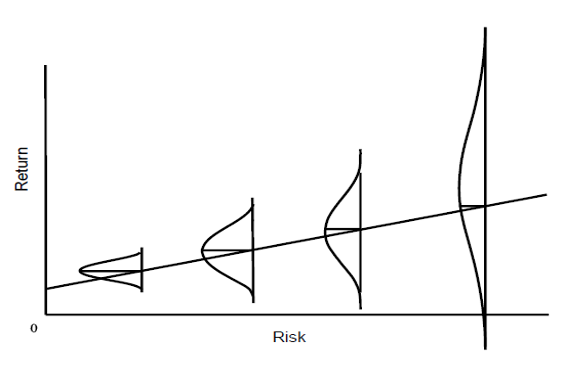

The graph above charts reward vs. risk. In periods when investors are risk averse and valuations low (in early 2000 as Covid hit), the riskier part of the curve (on the right) is the best place to be. But in periods (like late 2021 and June, 2023) when investors were ebullient (and bearing a lot of risk) and valuations high, the safer part (on the left) offers a superior route.

Our investment mantra is based on the intelligent bearing of risk -- judged by our assessment of reward vs. risk with a dose of "margin of safety."

Indeed, in an investing back drop in which the only thing that is certain is the lack of certainty - with a widening range of outcomes ever (in an interconnected and flat world) - we believe, for now, we should continue to err on the side of conservatism by embracing pairs investing and opportunistic trading.

That is not to say that being conservative will be a permanent condition at Seabreeze. In fact, with many of our potential concerns now slowly becoming more accepted -- the prospects for a better buy entry level for equities is improving as most stocks (save The Magnificent Seven) falter.

Our investment returns since the beginning of 2022 have been mostly characterized by staying on the left side of the risk curve in the chart above - with risk avoidance in pairs trades and opportunistic position trading over buy/hold investing.

We recognize that in a bull market risk avoidance equates to return avoidance. However, in the less certain and the less promising markets that have existed over the last 24 months, risk management/control (declining to take risks that exceed the quantum of risk we want to live with and/or Seabreeze wouldn't be well rewarded for bearing) has been our overriding strategy and mission.

Recently, investors have grown increasingly concerned about the challenges/headwinds we have outlined in our commentary to our Limited Partners over the past two years - the economic and market impact of interest rates "higher for longer," prickly inflation, political and geopolitical uncertainties, valuation risks and market structure issues. This is the first step in getting to more compelling valuations and entry points to buy. While, in the main, the markets remain overvalued, some sectors of the market are now approaching more attractive levels.

It is important to recognize that our returns in 2023 have been achieved despite taking minimum risk (as measured by our average monthly net exposure). As noted, insulating our Limited Partners from declines sows the seed for future gains.

Remember, short selling protects wealth and long buying generates wealth.

We are not Perma anything and look forward to the day that we can expand our exposure more aggressively. Our guess is that this might come sooner than later as stock prices fall to more attractive levels.

This Time It Really Might Be Different

Sir John Templeton, in an interview by Anise C Wallace in The New York Times in early October 1987, warned that when investors say times are different, it is typically an attempt to rationalize high stock prices... and ends badly.

Just days after that interview, the Dow Jones Industrial Average dropped by -22% on Black Monday.

What is not as well known is that Templeton also admitted that things might really be different some 20% of the time. During those periods when fundamentals do change, there can be significantly different investment implications.

We might be in that 20% of the time in which things might really be different... and more difficult!

To paraphrase Bob Dylan, The (Economic and Market) Times They Are A-Changin'.

As another poet, Oaktree's Howard Marks recently wrote - we are now likely undergoing a sea change in fundamentals and, with it, new investment strategies should be considered:

* In late 2008, the Federal Reserve took the fed funds rate to zero for the first time ever in order to rescue the economy from the effects of the Global Financial Crisis.

* Since that didn't cause inflation to rise from its sub-2% level, the Fed felt comfortable maintaining accommodative policies - low interest rates and quantitative easing - for essentially all of the next 13 years.

* As a result, we had the longest economic recovery on record - exceeding ten years - and "easy times" for businesses seeking to earn profits and secure financing. Even money-losing businesses had little trouble going public, obtaining loans, and avoiding default and bankruptcy.

* The low interest rates that prevailed in 2009-2021 made it a great time for asset owners - lower discount rates make future cash flows more valuable - and for borrowers. This in turn made asset owners complacent and potential buyers eager. And FOMO became most people's main concern. The period was correspondingly challenging for bargain hunters and lenders.

* The massive Covid-19 relief measures - combined with supply-chain snags - resulted in too much money chasing too few goods, the classic condition for rising inflation.

* The higher inflation that arose in 2021 persisted into 2022, forcing the Fed to discontinue its accommodative stance. Thus, the Fed raised interest rates dramatically - its fastest tightening cycle in four decades - and ended QE.

*For a number of reasons, ultra-low or declining interest rates are unlikely to be the norm in the decade ahead. Thus, we're likely to see tougher times for corporate profits, for asset appreciation, for borrowing, and for avoiding default.

Bottom line: If this really is a sea change -- meaning the investment environment has been fundamentally altered -- you shouldn't assume the investment strategies that have served you best since 2009 will do so in the years ahead.

Like Howard Marks, we see a sea change ahead.

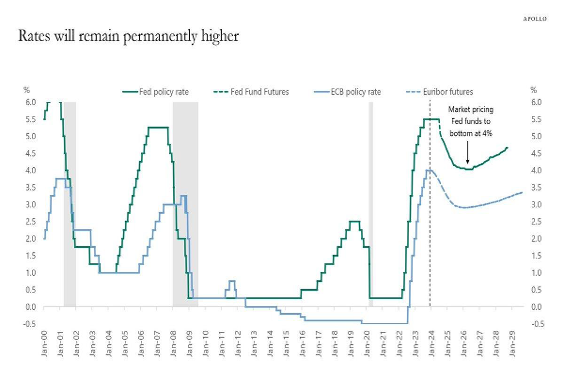

Most notably, over the last year interest rates have risen measurably and are likely to stay higher for much longer than the consensus expects. Higher interest rates/inflation (relative to the consensus expectations) and inflated valuations have formed the foundation of our market negativity since late 2021:

View Chart »View in New Window »

US Treasury Yields

- 3-Month: 5.62% (highest since Jan '01)

- 1-Year: 5.49% (highest since Dec '00)

- 2-Year: 5.15% (highest since Jul '06)

- 5-Year: 4.80% (highest since Jul '07)

- 10-Year: 4.81% (highest since Aug '07)

- 30-Year: 4.95% (highest since Sep '07)

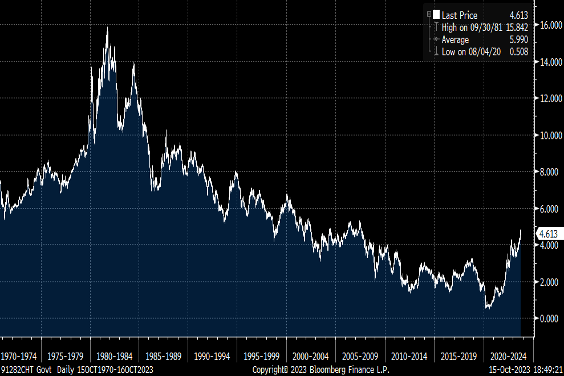

10 Year Treasury Yield (1970 to present)

View Chart »View in New Window »

Source: Peter Boockvar

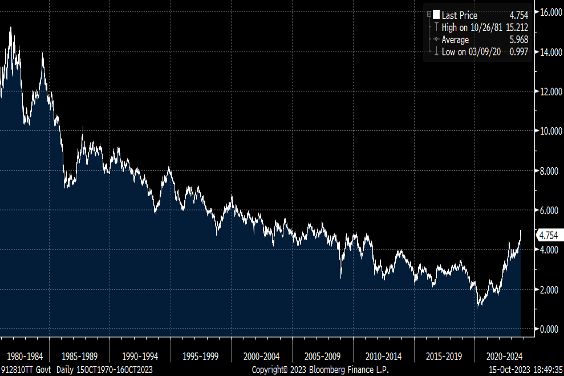

30 Year Treasury Yield (1980 to present)

View Chart »View in New Window »

Source: Peter Boockvar

I strongly agree with Howard's view that declining and/or ultra-low interest rates of the easy money period (since 2008) aren't going to be the rule in the time ahead. This leads to this set of obvious consequences:

- economic growth may be slower;

- profit margins may erode;

- default rates may head higher;

- asset appreciation may not be as reliable;

- the cost of borrowing won't trend downward consistently (though interest rates raised to fight inflation likely will be permitted to recede somewhat once inflation eases);

- investor psychology may not be as uniformly positive; and

- businesses may not find it as easy to obtain financing.

Positioning

Tactically, we continue to be fully invested (in gross terms) but lightly invested (market neutral) in net terms.

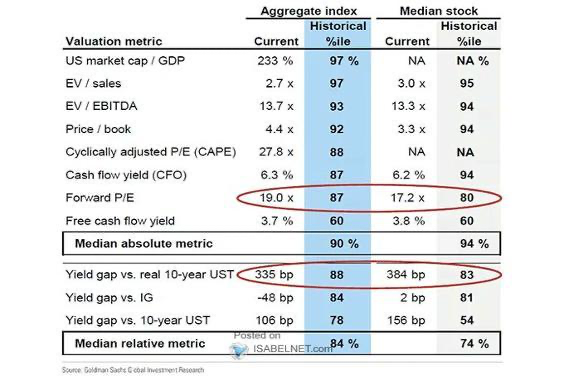

Above all, valuations remain elevated:

View Chart »View in New Window »

We remain of the view that credit is more attractive than equities; "slugflation" (sluggish growth and prickly inflation) lies ahead; political and geopolitical problems are intensifying; our leaders have never been more partisan (and their fiscal discipline never more uncontrollable - leading to a burgeoning annual deficit and a U.S. debt load whose service will serve to crowd out some domestic growth); interest rates will be "higher for much longer" (it is meaningless to me that we are at or close to the last Fed rate hike)...

Earnings per share expectations (high single digit/low double digit growth in 2024) and upbeat economic forecasts (within the context of rising real interest rates) seem fanciful; the strengthening U.S. dollar portends corporate-profit vulnerability; the move away from globalization and towards nationalization likely holds a future of lower than expected corporate profits (and margins) as well as producing more inflationary impulses.

Finally, the yields available in the fixed income markets (the one-year Treasury bill yields 5.40%) provides an equity-like return with little volatility of risk and compares favorably to the S&P dividend yield of only 1.62%. Resultingly, the equity risk premium is paper thin and at multi-decade lows - historically consistent with an extended period of lower future stock market returns.

As noted in our prior commentaries, market leadership continues to be narrow as the S&P Index's advance in 2023 has been dominated by seven large-cap technology equities. While those stocks continue to perform relatively well, many other companies' shares have moved lower. Though we continue to view the broader Indexes negatively, a few improving reward vs. risk opportunities are now developing away from The Magnificent Seven.

We have expected a sea change and have been of the belief that the successful strategy of being net long since The Great Financial Crisis (in 2007-2009) would not be the desirable strategy since late 2021. Rather, pairs trading (going long the most attractive and going short the least attractive stocks in an industry) and opportunistic trading remain our favored approaches during these uncertain times. In the last several months our returns have reflected the success of implementing these strategies.

Despite the expected sea change, long opportunities can emerge. Seabreeze is currently market neutral in our positioning - as we steadily reduced our net short exposure during the market weakness in September.

To be sure, when markets and individual equities become more attractive - on a reward vs. risk basis - we will enthusiastically be net long. And based on our assessment of the markets, this opportunity may finally become present in 2024 as the markets are slowly embracing many of our long-standing and multiple concerns.

Much like Alfred Winslow Jones (the father of the hedge(d) fund industry), Seabreeze differentiates itself by running a true long/short book. Unlike most hedge funds (which run leveraged long books), and unlike A.W. Jones (who greased his overall portfolio with borrowings) we never use leverage.

We strive for alpha (and superior stock selection in both our longs and shorts) over beta, in delivering superior investment returns.

We are equally as comfortable on the short side as the long side. Short selling mandates some degree of creativity. It is time consumptive as it requires a lot of primary research (as sell-side research staffs are geared towards longs). Importantly, as I have often discussed in my past lectures at Yale's School of Management, short selling mandates strong risk management skills.

If you look at our short positions listed below, you will find an interesting stable of well researched companies that face numerous fundamental challenges to their business models and competitive landscapes. I would venture to write that most of these companies are not in a typical hedge fund's short book and portfolio.

We Currently Have About 25 Longs and 28 Shorts

Here is a partial list of our longs -- Lilly LLY , St. Joe JOE , Occidental Petroleum OXY , Petroleo Brasileiro PBR , Paramount Global PARA , Warner Brothers Discovery WBD , Nike NKE , Green Brick Partners GRBK , TerrAscend TSNDF , Freshpet FRPT , Aercap AER , Goldman Sachs GS , Morgan Stanley MS , Bank of America BAC , Wells Fargo WFC and Schwab SCHW .

Here is a partial list of our shorts -- Tesla TSLA , FMC FMC , Starbucks SBUX , Lee Enterprises LEE , Harmony Biosciences HRMY , Samsara IOT , Berkshire Hathaway BRK.B , Winnebago WGO , Digital World Acquisition DWAC , Petco Health and Wellness WOOF , Chegg CHGG , Figs FIGS , Medical Properties Trust MPW , Freedom Holding FRHC , B. Riley Financial RILY , Nuvei NVEI , Sleep Number SNBR , DR Horton DHI , Rollins ROL , F45 Training FXLV and Xponential Fitness XPOF .

Finally, this is a follow up I sent to our investors a week ago. In this commentary I highlight the importance of transparency/communication, our tactics in navigating a difficult market and the possible timing of some emerging investment (not trading) opportunities I see in 2024 (after the current downturn runs its course):

While it was only last week that we conveyed to you our monthly commentary, these are volatile times - politically, geopolitically, economically and from a stock market standpoint.

As you have entrusted your capital to us, during such times, we feel an obligation to be transparent and more frequent in the transmission of our views and positioning.

Good communication builds trust. Indeed, I view the dialogue with our investors as the glue that binds us together with understanding of thought and investment process.

As some have noted by our rather lengthy monthly commentaries (!) I personally would rather err on the side of too much communication than too little communication. But, with these today's unprecedented and uncertain conditions we wanted to make some brief comments.

To quote an old Irish proverb, in this communique we will try to "say a little and say it well."

Though the markets have adopted a new regime of heightened volatility and have been moving steadily lower, I am happy to write that our Partnership's investment returns for the month of October to date continue to be positive and, as of Friday's close, our Net Asset Value is at a new 2023 high.

We remain fully invested in gross terms, but we are (cautiously) positioned market neutral in net terms.

For now, our strategy mostly involves pairs trading with opportunistic trading (long and short) as well, as longer-term investing. The later, maintaining longer term investment positions, continues to be deemphasized in light of the volatility, uncertainties and economic/market challenges discussed monthly since late 2021.

When I appeared with Charlie Munger and Warren Buffett as their invited "credentialed bear" several years ago at Berkshire Hathaway's Annual Meeting in Omaha (in which I peppered both of them with some hard-hitting questions) we had a discussion over the merits of trading vs. investing over lunch. Notably, Warren's investing timeframe is "forever," so Warren's response to trading over that lunch was predictable. He said to me, "calling someone who trades actively in the market an investor is like calling someone who repeatedly engages in one-night stands a romantic."

That said, the strategy of pairs and opportunistic trading has served us well and has allowed us to produce positive absolute and relative performance since the market top in December 2021.

Our defensive tactical position is not expected to be a permanent one as, in all likelihood, as stock prices decline, a terrific setup to position Seabreeze with longer term holdings is likely to develop and we can be expected to move back into a buy and hold investing strategy.

Being well positioned for the market's downturn and making (and not losing) money has sowed the seeds for Seabreeze's future investment returns when the market stabilizes and turns higher. At that point of stabilization, to quote Warren Buffett (again) we will be well positioned:

"Cash combined with courage in a time of crisis is priceless."

As noted previously we are not Perma Bulls nor are we Perma Bears. We assess equities dispassionately - our fundamental analysis gauges upside reward vs. downside risk with an attending view towards a "margin of safety."

One doesn't discover new lands without consenting to lose sight of the shore for a very long time. We look forward to shifting strategy and seeking the opportunity of establishing longer term investment positions when the above calculus becomes attractive.

(BAC is a holding in the Action Alerts PLUS member club. Want to be alerted before AAP buys or sells this stock? Learn more now.)

(This commentary originally appeared on Real Money Pro on October 25. Click here to learn about this dynamic market information service for active traders and to receive Doug Kass's Daily Diary and columns from Paul Price, Bret Jensen and others.)

At the time of publication, Doug Kass was:

Long JOE, OXY, PARA, WBD, NKE, PBR, AER, GRBK, TSNDF, FRPT, GS, MS, BAC, WFC, SCHW.

Short TSLA, FMC, SBUX, LEE, HRMY, BRK.B, WGO, IOT, DWAC, WOOF, CHGG, MPW, FRHC, RILY, NVEI, SNBR, ROL, FXLV, XPOT.