Disney Is Now a Wait and See Stock: Here's How to Play It

The lack of progress in managing the balance sheet is greatly disturbing.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Tuesday morning, the Walt Disney Company DIS released the firm's fiscal second quarter results. I am long this stock. The good news would be that I sold half of my stake at an average price of $119.97 after the Nelson Peltz proxy fight failed. I was betting on Peltz as much as I was on CEO Bob Iger.

The bad news would be that I hung on to the other half of that position through earnings. No tears. My net basis is in the low $80's so we're still playing with the house's money, but I could have traded this name a lot more effectively.

For the three-month period ended March 30th, the mouse posted an adjusted EPS of $1.21 (GAAP EPS: $-0.01) on revenue of $22.083B (+1.3%). The adjusted earnings print beat Wall Street by a dime. It looks like the GAAP earnings print missed, and the revenue print did miss, by just a smidge. The GAAP EPS print was down from $0.63 for the same period a year ago, largely thanks to a nominal loss due to goodwill impairments. The adjusted EPS number compares quite well to $0.93 for the year ago comp.

Operations

As revenue was growing 1.3%, costs and expenses combined decreased 1.7% to $19.204B. Restructuring and impairments charges increased from $152M a year ago to $2.052B. That's where the GAAP pain comes from. After accounting for interest, taxes and other income, GAAP net income printed at $216M (down from $1.488B).

After accounting further for net income attributable to noncontrolling interest, net income attributable to shareholders dropped all the way to $-20M, down from $+1.271B, or $-0.01 per diluted share versus $0.69. What to keep one's eyes on if one is a Disney bull, would be that total segment operating income outside of one-time items (impairments) printed at $3.845B, which was up 17% year over year.

Segment Performance

- Entertainment generated revenue of $9.796B (-5%), producing an operating income of $781M (+72%).

- Linear Networks generated revenue of $2.765B (-8%), producing an operating income of $752M (-22%). Decreases due to reduced subscribers leading to reduced advertising revenue.

- Direct-to-Consumer generated revenue of $5.642B (+13%), producing an operating income of $47M (up from $-587M)). Growth due to higher pricing model, subscriber growth at Disney+Core, and lower distribution rates. Disney+Core enjoyed 6% subscriber growth as well as 6% growth in average monthly revenue per paid subscriber.

- Content Sales/Licensing generated revenue of $1.389B (-40%), producing an operating income/loss of $-18M (down from $83M). Decreases due to the release of no significant title releases for the quarter.

- Sports generated revenue of $4.312B (+2%), producing an operating income of $778M (-2%).

- ESPN (domestic) generated revenue of $3.866B (+4%), producing an operating income of $780M (-9%). Margin reduced by higher costs associated with college football programming. Paid subscriptions suffered a 2% contraction at ESPN+. That was countered by a 3% increase in average revenue per paid subscription.

- ESPN (international) generated revenue of $341M (-7%), producing an operating income of $19M (flat).

- Star India generated revenue of $105M (-17%), producing an operating income/loss of $-27M (up from $-97M). Reduced losses were due to lower programming costs attributable to the loss of rights to broadcast Indian Premier League cricket matches.

- Experiences generated revenue of $8.393B (+10%), producing an operating income of $2.286 (+12%).

- Domestic parks & experiences generated revenue of $5.958B (+7%), producing an operating income of $1.607B (+6%). Improved performance was due to increased guest spending attributable to increased average ticket prices and increased prices at the Disney Cruise Line.

- International parks & experiences generated revenue of $1.522B (+29%), producing an operating income of $292M (+87%). Increases were due to higher ticket prices and increased spending on food and beverages.

- Consumer Products generated revenue of $913M (+3%), producing an operating income of $387M (+7%). Improvement was driven by increased game licensing revenue.

Outlook

For the full year, due to double digit percentage growth in adjusted earnings, the firm is now expecting full year 25% growth in adjusted earnings. The firm remains on track to generate approximately $14B of operating cash flow and more than $8B in free cash flow for the fiscal year. Disney also expects the firm's combined streaming businesses to be profitable by fiscal Q4 and be a driver of growth for the company into fiscal 2025.

Fundamentals

For the first haft of Disney's fiscal year, the firm has generated $5.851B in operating cash flow. Out of that number came $2.558B in Capex spending to include investing in the parks. That left a six-month free cash flow print of $3.293B, which was up from $-168M for the year ago comparison. Out of that free cash flow print, the firm repurchased $1.001B worth of common stock for its treasury and paid out $549M in cash dividends to shareholders.

Glancing at the balance sheet, Disney ended the period with a cash position of $6.635B and inventories of $1.948B. This puts current assets at $24.636B. Current liabilities add up to $32.874B. Shorter-term debt comes to $6.789B, but also $7.287B in deferred revenue, which we know is not a true financial obligation. This puts the firm's headline current and quick ratios at 0.75 and 0.69. That would be close to unacceptable in my world.

However, once adjusting for those unearned revenues, these ratios rise to 0.96 and 0.88. Guess what? Still not so hot. This balance sheet/current situation is not as strong as I would like for a firm that is buying back stock and reinstating dividends.

Total assets amount to $195.11B, including $85.388B in goodwill and other intangibles. At 43.8% of total assets, I am somewhat uncomfortable with the level of intangible assets being this high. I know, Disney does have a lot of actual intangible assets that are real and could be sold. Still, I don't love it. Total liabilities less equity comes to $91.347B. There's another $39.51B in longer-term debt here.

I do not like that the firm's cash position comes to less than its short-term (due in less than one year) debt-load. That means that Disney will have to borrow this year at elevated interest rates in order to keep the ball rolling unless they make smarter use of their cash flows... which is unlikely.

My Thoughts

Anyone who reads me or has read me for a long while knows that I am a Disney fan. I like the parks. I like the moves. I like the streaming services. I love Star Wars and I love the traditional Disney characters. I am very capable of being bullish on Disney's stock due to an unintentional bias.

I have no doubt that CEO Bob Iger is resurrecting the brand and the businesses. Is that enough? I told you that I made a really smart sale after Nelson Peltz failed to win board representation.

There is no doubt in my mind that with cash flows like this, the firm should be further along in improving the quality of what has to be termed as a "poor" balance sheet. I do not like sloppy cash flow discipline and if anything, Disney has always shown sloppy discipline in this part of their business and still is. In that, I am disappointed.

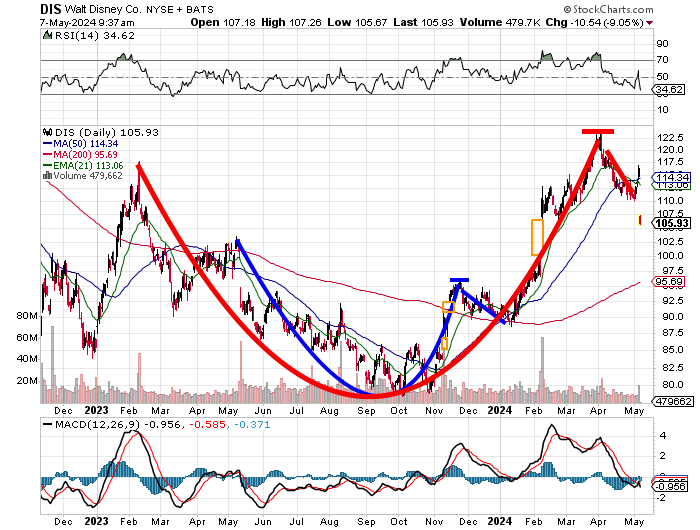

Readers will see that DIS came into this report with a better-looking RSI (relative strength index) and a better looking daily MACD (moving average convergence divergence). That will change early this morning.

We have a cup with handle pattern that stretched from May 2023 to December 2023 that produced a nice breakout that we took full advantage of. Now that cup with handle neatly fits in a much larger cup with handle pattern that stretched from February 2023 into the present. This could have set up another nice run with a $123 pivot with a target price conservatively in the low $140's.

The lack of progress in managing the balance sheet disturbs me greatly. I have profits here to protect, as I told you above. I am downgrading DIS to a "sell" and will work towards extracting myself from the name intelligently, until the shares reach a point where they once again look attractive to me. That might be the 200-day SMA (simple moving average). We'll have to see.

At the time of publication, Stephen Guilfoyle was long DIS equity.