Bristol-Myers: Here's What Would Get Me Interested

The quarter was solid. The guidance was too. So, what's holding me back?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

This was a heavy week of earnings releases. Thank goodness, Friday, as is usual, brought with it a lighter slate.

Though I can't complain, I have defended myself well in a tough market, I am a little tired. I am glad that Friday is thin on corporate headlines.

The highlight of this lighter slate of performance-related data probably came from Bristol-Myers Squibb BMY. The company put together a better-than-decent second quarter coupled with some nice guidance — and the stock is trading sharply higher.

Second-Quarter Results

For the three-month period ended June 30, BMY posted adjusted EPS of $2.07 (GAAP EPS: $0.83) on revenue of $12.201 billion. The adjusted bottom-line print crushed Wall Street expectations, while the top-line number also beat the Street, reflecting year-over-year growth of 8.9%. The lion's share of the adjustment made to earnings was for the amortization of acquired intangible assets.

U.S.-driven revenue increased 13% to $8.8 billion, primarily due to the Growth and Legacy Portfolios. International-driven revenue decreased 1% to $3.4 billion due to a 7% negative impact of foreign currency exchange rates that was partially offset by sales of Opdivo. On a GAAP basis, gross margin narrowed to 73.2% from 74.4% due to marketed product rights and a one-time impairment charge. Adjusted gross margin actually improved to 75.6% from 75%.

Best selling drugs in the Legacy Portfolio were Eliquis for the treatment of blood clots and prevention of stroke for patients with AFib, and Revlimid for the treatment of patients suffering from myelodysplastic syndrome, multiple myeloma, and mantle cell lymphoma. The runaway best seller in the Growth Portfolio was Opdivo for the treatment of advanced stage lung cancer.

Improved Guidance

For the full year, Bristol is now looking for total revenue growth to print at the upper end of the low-single-digit range, up from prior guidance for simply low single digits. Gross margin for the full year is now seen at 74% to 75%, up from roughly 74%. Operating expenses are now seen as flat from last year as opposed to being up small.

All in all, full-year diluted EPS is now projected at $0.60 to $0.90, up from $0.40 to $0.70. Hey Sarge, Q2 diluted EPS printed at $0.83. What gives? Bristol posted a first-quarter GAAP loss per share of $5.89, adjusted to a loss per share of $4.40. The quarter included a one-time net impact of -$6.30 per share of Acquired IPRD charges from recently closed transactions. Hence, the entire year now looks skewed to the casual investor just happening upon these numbers.

More Good News

Bristol also cited top-line data for its Phase 3 trial of its experimental antibody therapy, cendakimab, for the potential treatment against an allergic condition known as eosinophilic esophagitis. The candidate apparently met both co-primary endpoints following 24 weeks of therapy.

There were no new safety signals and the therapeutic's tolerability over 48 weeks of treatment was in line with past data. Bristol will engage key investigators at a future medical event to share detailed data.

Fundamentals

For the first six months of the year, Bristol-Myers Squibb generated operating cash flow of $5.16 billion. Out of that number came capex spending of $546 million. That left free cash flow of $4.614 billion. Out of that number came cash dividend payments of $2.429 billion. Instead of repurchasing common shares for the company treasury, the company paid down some debt with the balance.

Turning to the balance sheet, Bristol ended the period with a cash position of $6.653 billion and inventories of $3.077 billion. That put current assets at $26.89 billion. Current liabilities printed at $23.265 billion, including short-term debt of $3.751 billion. That leaves the company with current and quick ratios of 1.16 and 1.02, respectively. Not awesome, but certainly strong enough to pass muster.

Total assets amounted to $94.646 billion, but that does include goodwill and other intangibles of $51.16 billion. At 54% of total assets, I do think this a bit much. It does make me somewhat uncomfortable. Total liabilities less equity comes to $77.577 billion, including long-term debt of $48.858 billion, which is a bit on the beefy side.

Bristol is OK for the short to medium term. Fortunately, this name is a free cash flow beast because to get this balance sheet in tip top condition, it's going to have to be.

My Thoughts

Is there a trade here?

The quarter was solid. The guidance is as well. BMY is trading at 91 times forward-looking earnings and 22 times trailing 12-month earnings. The stock trades at 5.6 times book. This is an expensive pharmaceutical stock. Even Eli Lilly LLY, which has gone bonkers this year trades at "just" 60 times forward-looking earnings.

This is a play on that Phase 3 candidate discussed above. The projected market for eosinophilic esophagitis is anticipated to grow significantly and by some estimates, could reach more than $10 billion by 2032. If you believe in this drug, you believe in BMY. If you don't, you're looking at an expensive stock that still yields 5.3% with its $2.40 per share annual dividend.

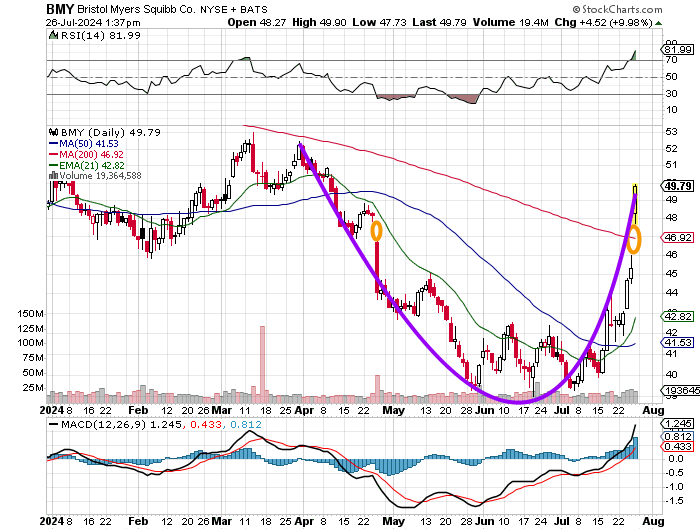

Note in the chart above that the gap from late April has now filled. Relative strength has entered into technically overbought territory. The daily Moving Average Convergence Divergence (MACD) appears to be quite extended as well.

If you see a triple bottom reversal, then the pivot is roughly $43, and the target price would be around $51. That does not sound all that interesting. If, however, you see a typical cup pattern, that would put the pivot at $52 and the potential target at $62. Far more interesting.

Keep in mind that the stock may add a handle, and when it does, the pivot will shift to the right side of the cup from the left. Also keep in mind that adding a handle could cost the stock it's 200-day simple moving average (SMA). Understand also that some portfolio managers are forced to act at that line. They are being forced in this morning. That exacerbates this rally. They'll be forced out if the line fails to hold.

I can wait. There will be a better day to buy BMY than Friday.

At the time of publication, Guilfoyle had no positions in any securities mentioned.