Bloomin' Brands Stock Can Fall Even Further as CEO Vows to Improve

There could be a short opportunity as foot traffic falls and costs rise at brands like Outback Steakhouse and Carrabba's.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

For all things there is a season and, as we all know, seasons change. There is the bloom of spring, the flourishing through summer and then ultimately comes autumn. The leaves fall. The petals fall. The bloom of a hopeful spring becomes little more than memory. Bloomin' Brands BLMN released the firm's third quarter financial results on Friday morning. One might say that the bloom is off of that rose, or we should say, off that onion.

For the three-month period ended September 29, the parent company of Outback Steakhouse, Carrabba's Italian Grill and Bonefish Grill posted an adjusted EPS of $0.21 (GAAP EPS: $0.08) on revenue of $1.039 billion. The sales print was in line with expectations, despite reflecting a year-over-year contraction of 3.7%, as the adjusted earnings line beat by a penny. Adjustments were made primarily for the impairment of assets and store closing.

There really is no way to sugarcoat this... comparable U.S. store sales were down 1.5% from the same period one year ago. By brand, Outback Steakhouse same-store sales were down 1.3%, Carrabba's same-store sales were down 1.5%, Bonefish same-store sales were down 4.1%, and the lone bright spot, Fleming's Prime Steakhouse & Wine Bar same-store sales were up 1.2%. Outside of the U.S., Outback Steakhouse same store sales were down 3.6% in Brazil.

Brand Performance

The above are same-store sales. When including new and closed locations, performance is as follows:

- Outback Steakhouse (U.S.): Traffic is down 3.9%, while the average check is up 2.6%.

- Carrabba's: Traffic is down 3.4%, while the average check is up 1.9%.

- Bonefish: Traffic is down 8.5%, while the average check is up 4.4%.

- Fleming's: Traffic is down 7.3%, while the average check is up 8.5%.

- Outback (Brazil): Traffic is down 7.7%, while the average check is up 3.4%.

Operations

While revenue was contracting 3.7%, total costs of sales and operating expenses together, contracted fractionally to $1.022B billion. This left the firm with a GAAP operating income of $17.21 million (-70.4%). After accounting for interest, other income and expenses, taxes and a small loss on the extinguishment of some debt, income attributable to shareholders printed at just $6.912 million, which was down 84.5% from the same period one year ago. This works out to $0.08 per fully-diluted share, down from $0.45.

Fundamentals

I have not yet been able to find a Form 10Q for Bloomin' Brands for the quarter. I do not think that one may have been filed, at least not yet. In the press release, the firm does list some supplemental balance sheet information. Currently, the firm has a cash position of $83.6 million, down from $111.5 million at the start of the year. The firm has net working capital of $-587.9 million, total assets of $3.434 billion, total net debt of $1.092 billion and stockholder equity of $244.9 million, down from $412 million over nine months. I have no proper balance sheet nor a statement of cash flows to go over for you.

Guidance

For the current quarter, Bloomin' Brands sees U.S. comp sales down 2% to 1%. GAAP EPS is projected at $0.31 to $0.41 with adjusted EPS at $0.32 to $0.42. This is way below the $0.67 or so that Wall Street had in mind.

For the full year, Bloomin' is lowering guidance. U.S. comp sales goes from -1% to flat, down to -1% to -0.5%. GAAP EPS is changed from $0.25 to $0.45 to $-0.26 to $-0.16, while adjusted EPS is reduced from $2.10 to $2.30 to $1.72 to $1.82. Wall Street was thinking something in between $2.05 and $2.10.

My Thoughts

You have declining sales, falling same-store comps, less foot traffic and guidance that has been cut quite severely. The firm also has not yet released its key financial documents. Not a lot to like. What they do have is a new CEO. That individual, Mike Spanos, commented in the press release: “As I continue listening and learning during this evaluative period, it is clear to me that our path to sustainable sales and profit growth will be enabled by our team members executing a consistent and elevated guest experience, focusing first on Outback Steakhouse. Our full-year guidance has been updated to reflect our results and near-term trends. We are committed to improving our performance.”

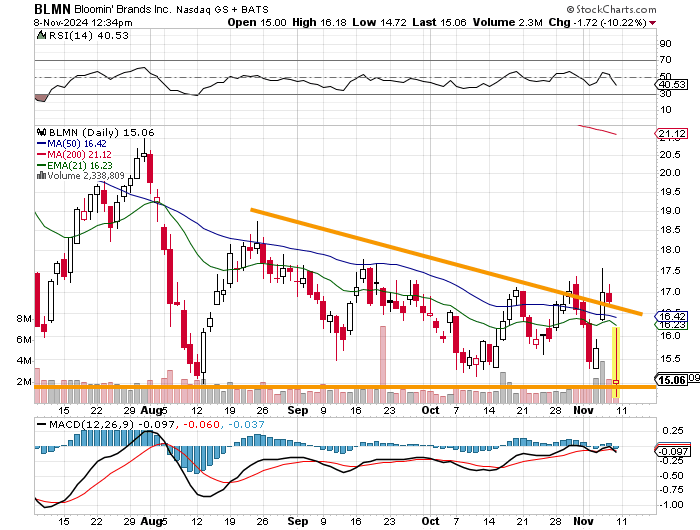

Readers will see a loose descending triangle on this chart, which unfortunately is a bearish pattern. Yes, the stock could fall further. Relative strength is weak, but not awful. The daily MACD is still bearish looking but has improved its appearance over the past two months.

I would think that a short might still work, even with the stock down 10% today. The reason that I won't go there is that I do not short stocks where more than 8% of the float is already held in short positions. For Bloomin' Brands at this time, that number is 9.5%. A trader could go out two months and pick up some January 17 $12.50 puts for a mere $0.35.

That's a low risk, low-to-medium probability trade that would require the stick to trade below $12.15 by expiration in order to turn a profit. This may not be worth the effort, but it probably won't hurt the trader either.

At the time of publication, Guilfoyle had no positions in any securities mentioned.