As Small Caps Strengthen, I'm Eyeing This Stock

Time for an update on ADMA Biologics.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The market started off with mild gains on Thursday morning, but is cooling a little bit. Small caps, as represented by the Russell 2000 fund IWM are leading, and that is helping to keep breadth positive.

The million-dollar question is whether the pattern of strong closes and narrow big-cap strength will continue. As I discussed in my opening post, it is premature to talk about a change in the character of the market action until we see some late-day weakness and poor closes. The conventional wisdom is that smart money institutional investors tend to act at that close, and currently, they are staying quite bullish. Once they start to back off, the risks of some corrective action will increase.

A number of smaller stocks that I favor have been drifting lower due to the Russell 2000 weakness and are struggling to find support. I'll be looking for some buys, but I'm not rushing until I see some better price action. The biggest problem right now is that if the big-cap technology names finally start to correct, it will likely weigh on the broad market, even though the broad market isn't anywhere close to extended like the Magnificent Seven names.

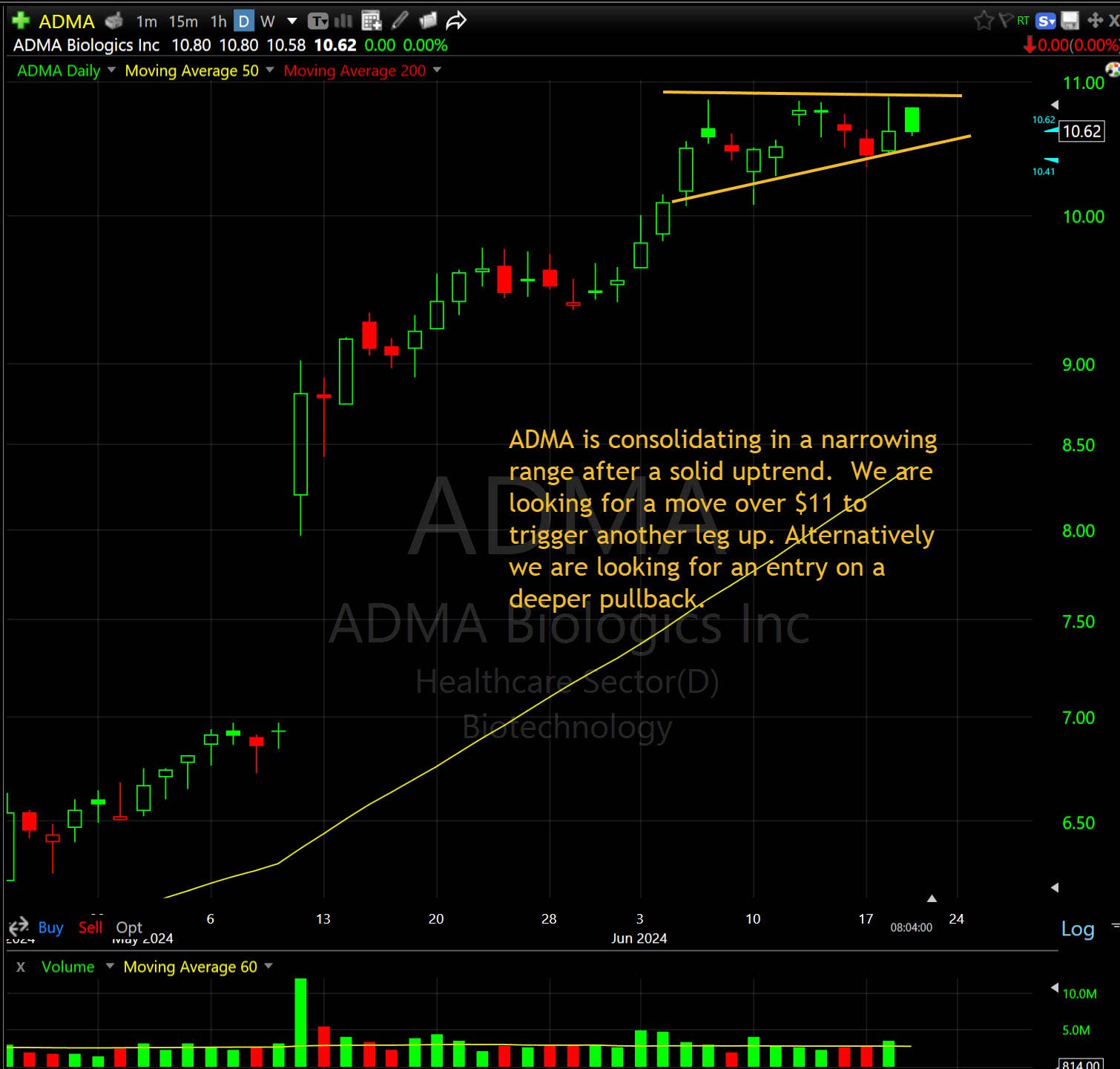

One name I want to update today is ADMA Biologics ADMA. I introduced this stock on Feb. 29, 2024, when it was trading at around $5.40. It is now up a little over 100% in 3 ½ months and continues to look quite good.

Since I initially discussed it, ADMA has posted very strong earnings, increased guidance, and seen a number of price target increases from analysts. Just this morning, analysts at Mizuho increased their target price to $14 from $12 and commented, hyper top-line growth and profitable therapeutics comps "suggests premium multiples are warranted to reflect the scarcity value around the story."

Technically, the stock has been taking a little rest recently and consolidating gains. I'm still holding a core position and would like to add to it on a pullback in front of the next earnings report or a big volume break-out.

ADMA has positive "CANSLIM"characteristics with an earnings per share rating of 80, a Relative Strength rating of 99, and an Accumulation rating of A+. Revenues grew 44% last quarter, and EPS should increase to $0.36 in 2024 from just one cent in 2023. The stock has both operational and technical momentum.

There aren't many small caps acting like ADMA. If the Russell 2000 ever starts moving again, then it should see renewed attention.

At the time of publication, DePorre was long ADMA