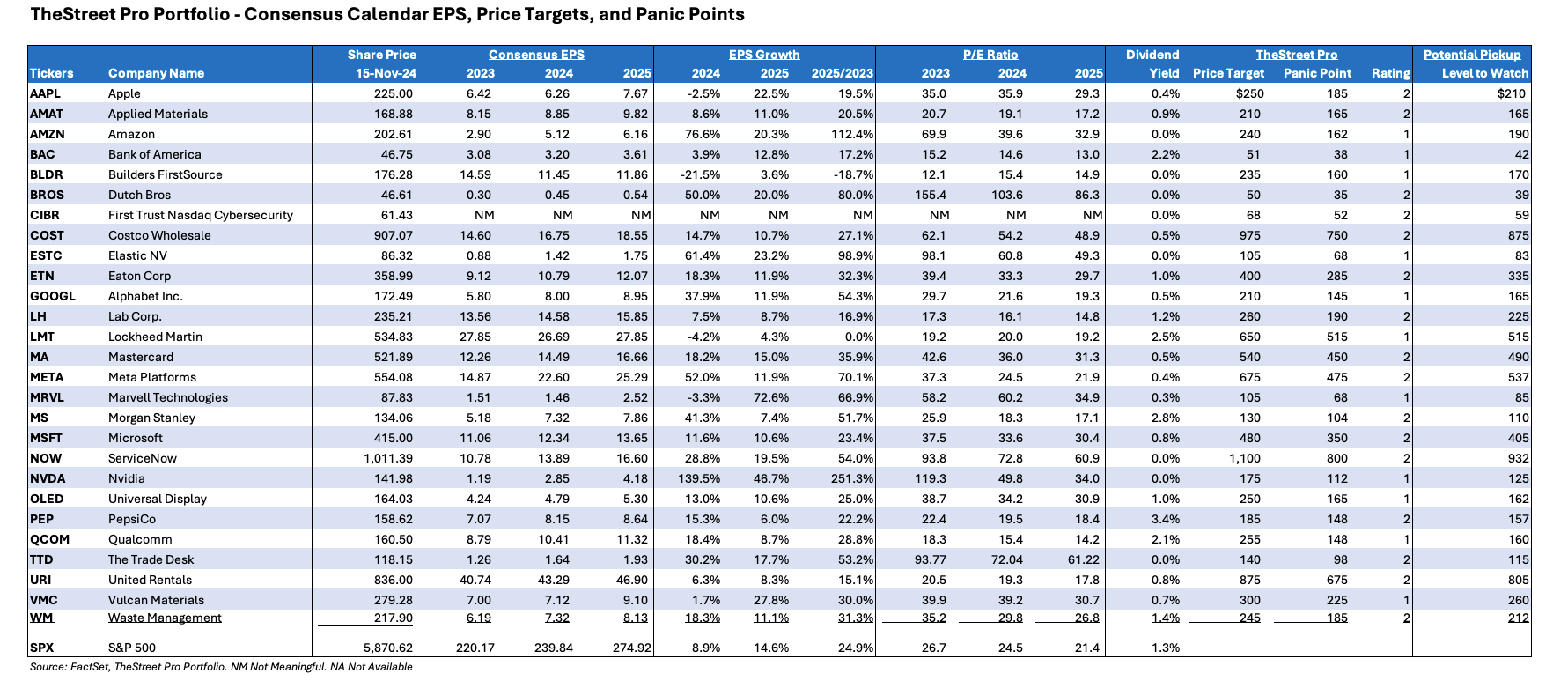

Updating Our Table for Panic, Potential Pickup Points

We will remain focused on companies with superior EPS growth as we approach 2025.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Consensus EPS Changes

As we near the end of the September quarter earnings season, we are seeing some adjustments to 2024 consensus calendar EPS, but we are also seeing some movement as it relates to 2025. Based on what we’ve seen so far, the 14.6% year-over-year consensus EPS jump for the S&P 500 next year is high by historical levels.

The bulk of that increase comes in 2H 2025, which also fits the historical pattern and means that we’ll be watching those expectations closely when companies give their first cut at 2025 EPS in January. As we evaluate new contenders for the Portfolio as well as our holdings on a go-forward basis, we’ll continue to use consensus EPS growth expectations for the S&P 500 as one of our yardsticks.

Now, let’s share the updated 2024 consensus EPS expectations for the Portfolio’s positions:

Amazon’s AMZN 2024 EPS now sits at $5.12, up from $4.99; 2025 has been lifted to $6.16 from $5.99, pointing to significant EPS growth prospects compared to 2023.

2024 EPS for Builders FirstSource BLDR was lifted to $11.45 from $11.37, but the impact of a few rate cuts in 2025 has led consensus 2025 EPS to be trimmed back to $11.86 from $12.05.

Coming off its beat and raise quarter, consensus 2024 EPS for Dutch Bros BROS was boosted by $0.05 to $0.45 while the figure for next year now sits at $0.54, up from $0.49.

We saw no movement in 2024 EPS for Eaton ETN but the consensus 2025 EPS figure has been increased to 412.07 from $11.92, likely reflecting the favorable outlook for data center construction.

With the 2025 consensus EPS being dialed back to $27.85 from $28.50, the market is taking a more conservative view on Lockheed Martin’s LMT prospects. This likely reflects renewed calls to end the Ukraine-Russia conflict as well as a potential resolution between Israel and Lebanon. However, NATO countries are still ramping up their defense spending as a percentage of GDP, and Lockheed’s revenue and EPS stand to benefit from increased F35 shipments next year and the year after. The company’s multiyear delivery schedule, which should be delivered in early 2025, should bring some EPS clarity.

Following its recent Investor Day, consensus 2024 EPS for Mastercard MA shares moved up $0.05 to $14.49, but the outlook for 2025 was revised to $16.36 from $16.61. While the year-over-year EPS growth is still ahead of expectations for the S&P 500, the downward revision is another reason why we think some of the recent price target adjustments for MA shares are overly aggressive.

Calendar consensus EPS for Meta Platforms META was lifted once again for 2024 and 2025. For this year the new consensus now resides at $22.60, up from $22.09, while for next year it how hangs at $25.29, up from $25.13.

Ahead of Nvidia’s NVDA earnings later this week, the market now sees it delivering EPS of $4.18 next year, up from the prior view of $4.06 and $2.85 in calendar 2024.

While there was no change for consensus 2024 EPS at Universal Display OLED, we did see the 2025 figure move to $5.30 from $5.65. This likely reflects a more cautious stance on the smartphone market but gives only modest credit for the adoption of organic light-emitting diode displays in other markets outside of smartphone and TVs. As it relates to the 2025 smartphone market, we’ll be looking to see if upcoming software updates stimulate the upgrade cycle. We’ll also be watching CES 2025 in January for new applications using this display technology as well as announcements for new foldable product offerings.

Consensus EPS for Trade Desk TTD was bumped up to $1.64 and $1.93 for 2024 and 2025 from $1.60 and $1.90, respectively.

With the announcement Waste Management WM has closed the pending acquisition of Stericycle, we’ve seen some initial movement in 2025 EPS expectations to $8.13 from $8.07. We expect Waste will provide a more detailed view of Stericycle’s integration and cost-saving opportunities when it reports the December quarter.

Panic Points Adjustments

Following the market’s overall move in the first half of November, we are making the following panic point adjustments. Ahead of Qualcomm’s QCOM Investor Day this week as well as earnings from Nvidia and Elastic ESTC, we will revisit those panic points later this week.

Bank of America: Our panic point is lifted to $38 from $34

Eaton: Boosted to $285 from $275

Marvell MRVL: Upped to $68 from $64

Morgan Stanley MS: Reset at $104, up from $95

ServiceNow NOW: Lifted to $800 from $775

United Rentals URI: Increased to $675 from $650

Potential Pickup Points

Included in this updated table are potential price points at which we may consider picking up more shares of that particular holding. The indicated levels offer favorable risk-to-reward entry points, and we recognize the odds of all the positions hitting those levels are low. As we share these potential levels, a decision to act or not will reflect any new data or information as well as what is unfolding in the market.

We would suggest members see these levels as a guide and not something carved in stone. We expect to update these levels as we move through the coming weeks and get ready for 2025.

More Pro Portfolio

- We're Closing Out This High-Flying Position With a Triple-Digit Gain

- Weekly Roundup: A Big Week for the Market, But Caution Lights Are Flashing

- In Case You Missed It: Reports That Held Clues for Our Holdings Amid Busy Week

At the time of publication, TheStreet Pro Portfolio was long AMZN, BLDR, BROS, ETN, LMT, MA, META, NVDA, OLED, TTD, WM, QCOM, ESTC, MRVL, MS, NOW and URI.