Our Take on May PCE: Surprises and 'Hmmms' in the Data

Real wage growth continued in May, a positive for spending in the second half of 2024.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* The May PCE price index data came in largely as expected, showing further progress on inflation.

* The market will like the larger drop in PCE Service ex-energy and housing.

* The upward revision in the April core PCE figure will keep the Fed attuned to head-fake risk.

* Here's the list of next week’s data we’re watching for signs of more inflation progress in June.

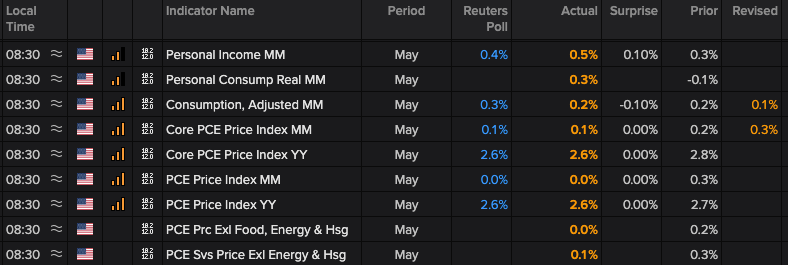

The much-awaited May PCE price index data was published Friday morning and as we can see in the table below, for the most part, it was encouraging. As we've discussed this week, in the May PCE data we were looking for confirmation of the May CPI and PPI reports – and we got it. While headline and core PCE figures showed the expected progress the market was looking for, the positive surprise was found in the PCE Service ex-energy and housing that came in at 0.1% sequentially, down from 0.3% in April and 0.4% in March.

Next week brings the start of June data, and what we find in the final June PMI reports from ISM as well as S&P Global will tell us if even more progress was made. Our thinking, especially after last night’s presidential debate, remains that the Fed is not likely to deliver a September rate cut, but if the ensuing data point to further improvement, our thinking for two potential rate cuts late this year could increase.

Getting back to Friday's report, in the “hmmm” camp, the core PCE price index figure for April was revised to 0.3% month over month (MoM) from the initial 0.2% figure. That revision means the core CPI was unchanged at 0.3% in February, March, and April. Yes, the initial print for the May core PCE of 0.1% MoM suggests considerable progress compared to those three months, but remember the Fed wants to be convinced inflation is indeed falling on a sustainable basis.

While the market is going to take the May report as another positive step, the Fed will likely want to see the revisions to the May data before climbing on board. Odds are that will be the message delivered by the two Fed speakers Friday – Fed Governor Michell Bowman at noon ET and San Francisco Fed President Mary Daly at 12:40 PM ET.

Alongside the May PCE data, May personal income not only strengthened compared to April but was ahead of market expectations. Parsing the figures, we also see real wage growth accelerated during the month. However, folks didn’t consume as much as expected, not much of a surprise given the May Retail Sales report. Parsing the data, we are seeing the savings rate tick higher in May to 3.9%, up from 3.7% in April and 3.5% in March. The question we’re pondering is if we’ll see this continue in June and July, with Amazon’s AMZN 2024 Prime Day scheduled for July 16-17.

At the time of publictaion, TheStreet Pro Portoflio was long AMZN.