Latest Economic Data Points to Manufacturing Resurgence

New orders strength bodes well for more, but the Fed will still focus on these two revelations.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

For the uninitiated, we track the monthly Purchasing Managers Indices from the Institute for Supply Management (ISM) for a few reasons.

The biggest is the insight that the data brings about the speed of the economy, as well as insights on inflation and job creation, and the data does so for both the manufacturing economy (10% to 15% of GDP) and the services one (85% to 90% of GDP). Another reason is that this data from ISM is factored into those GDP calculations for their corresponding quarterly period.

Setting the Stage

One of the more common trackers of GDP expectation is the Atlanta Fed’s GDPNow model, but that tracker is still showing expectations for Q4 2025. And as of Monday morning, it’s calling for a robust 4.2% GDP print for that quarter.

Turning to the NY Fed’s GDP Nowcast model, as of Friday’s its forecast for Q4 2025 was 2.74%, which still points to above trend growth. However, because we will be assessing January data this week, starting with Monday's January PMI from ISM, we’re more interested in what the New York Fed’s model has to say about the current quarter. Ahead of Monday's data and as of Friday, January 30, it called for a 2.73% GDP print for Q1 2026.

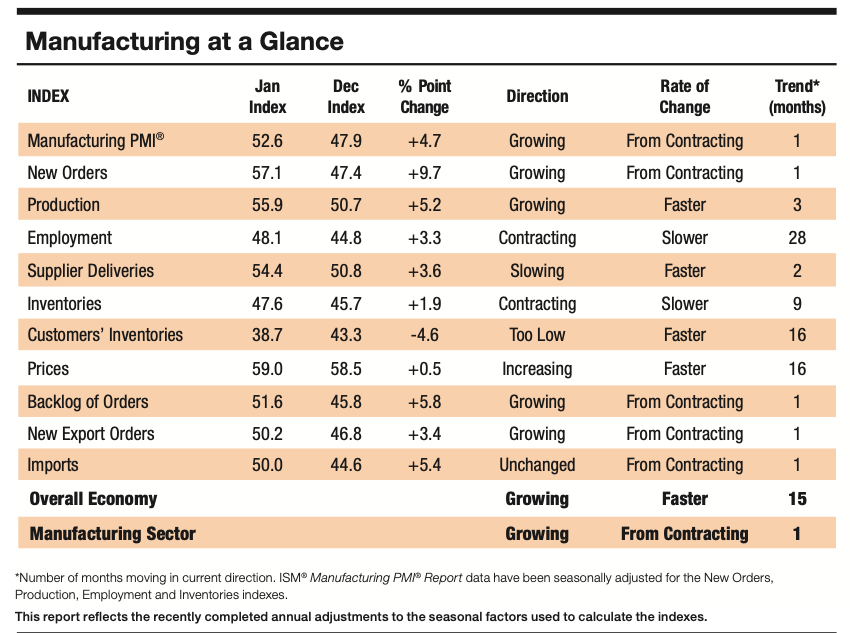

The January Manufacturing PMI From ISM

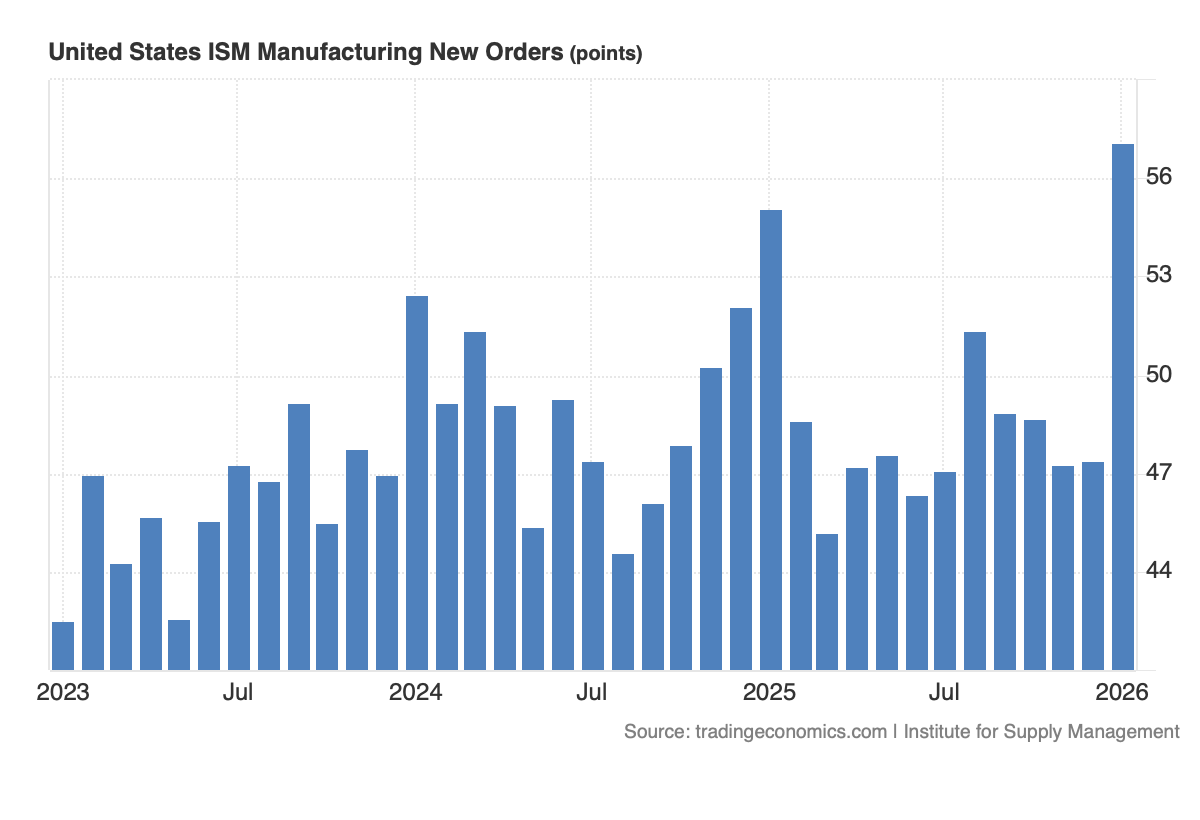

As we can see in the table above, ISM’s findings for the headline January Manufacturing PMI, production and new orders point to the new year seeing a resurgence in manufacturing activity, and it should continue. We can say that based on the sharp jump in the New Order component, which hit the highest level in three years.

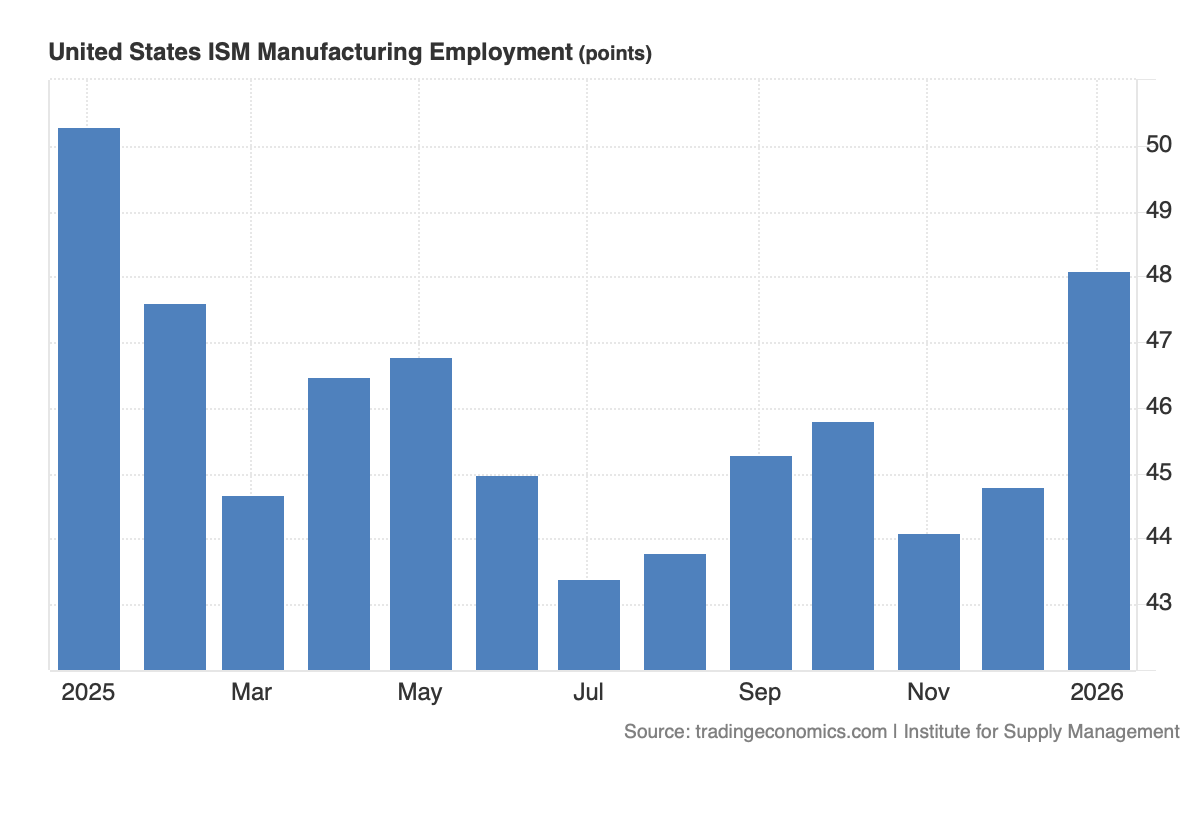

The same report also showed the employment picture and, while still contracting in January, the level of that contraction wasn’t as steep in 2H 2025. That's somewhat of a relief, but the reality is we will want to see the full employment picture from ISM, and that will happen on Wednesday, February 4, when we get ISM’s January Service PMI.

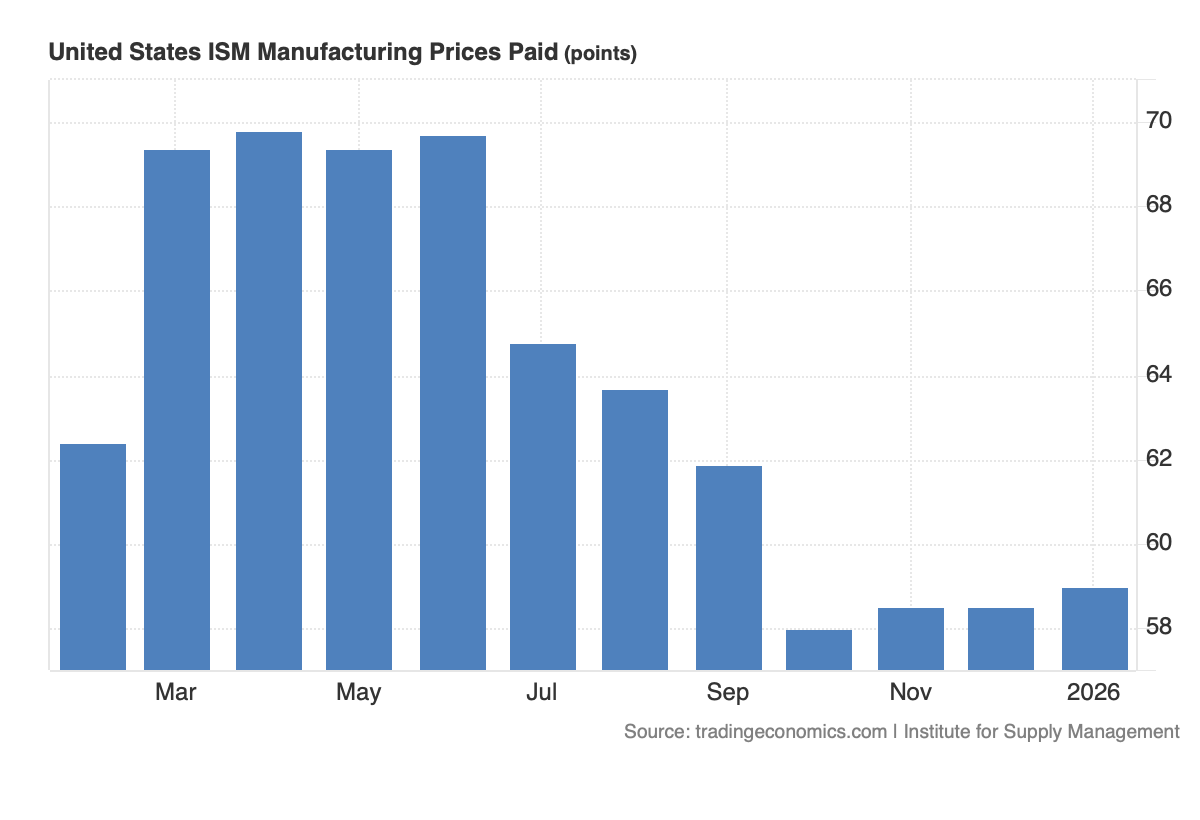

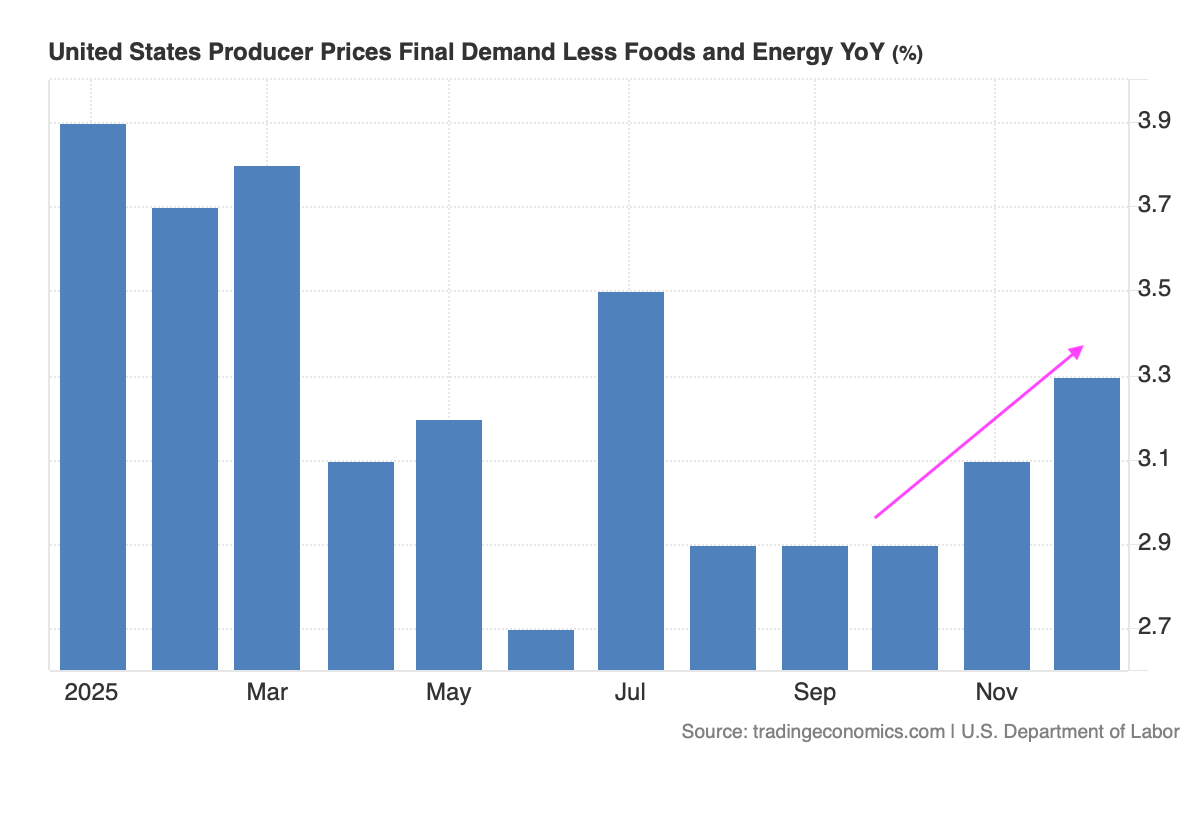

On the inflation front, well, what we got from ISM, and by that we mean the January jump increase in the Price subindex to 59.0 from 58.5, isn’t constructive, especially after the hotter print we saw in Friday’s December core PPI.

Again, we’ll have a more complete picture come Wednesday morning, but the takeaway from Monday's PMI data is that the employment market could be stabilizing in slow growth mode, but inflation doesn’t appear to be backing down. More data like this and Fed Chair Powell's replacement may have an unpleasant surprise for President Trump.