Here's Why We're Keeping Eaton in the Bullpen

The stretched valuation reflects the barrage of headlines and news stories about power needs.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* Here’s when the Portfolio may initiate a position in Eaton shares.

Since adding the shares of Eaton Corp ETN to the Bullpen, we’ve been doing some follow-up work to determine potential entry points for the shares as a play on electrical power demands for data center, EV charging, and other drivers.

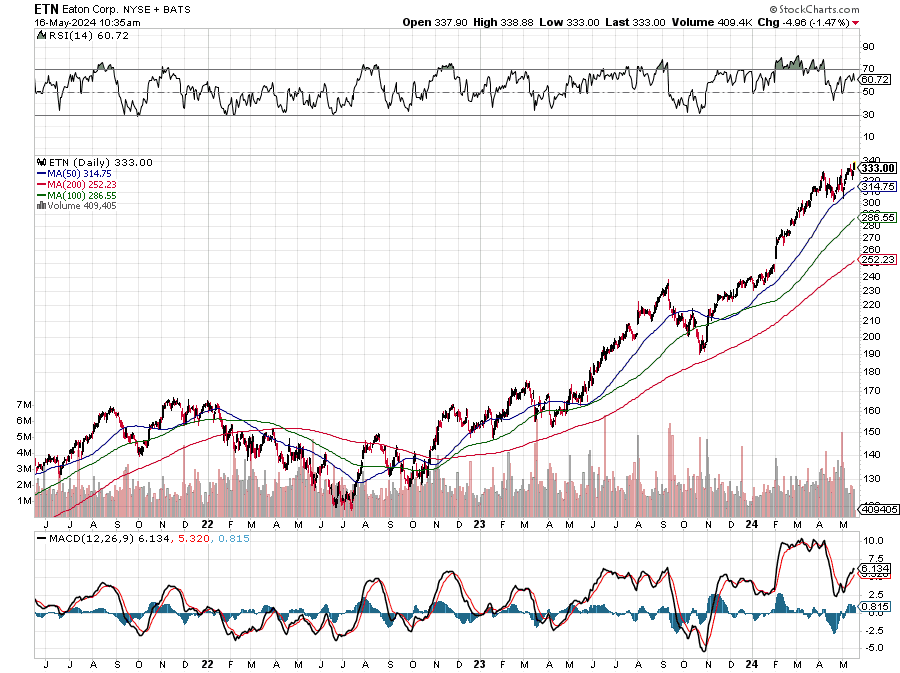

As we look back at the chart below, ETN shares have been a strong performer starting in April 2023 when the topic of AI took hold, driving the Magnificent 7 higher. The 2023 year-end rally lifted ETN shares further, and the wave of articles about power constraints and company capital spending on AI/data pushed ETN shares up even further this year.

Currently, ETN shares are trading at near $334, about $2 above the Wall Street consensus price target.

From a valuation perspective, ETN shares are trading at just under 32x expected EPS of $10.50 this year, and 28.7x on 2026 consensus EPS of $11.64. When we look at those figures, they are up 27.6% compared to the $9.12 Eaton posted in 2023, which is only marginally higher than the expected EPS growth of 26.2% for the S&P 500 over the same period. By comparison, the S&P 500 is trading at ~22x consensus 2024 EPS and 19x expected 2025 EPS.

We recognize the expected demand ramp for Eaton’s electrical business, which accounts for ~60% of its revenue and 75% of its operating income, and that should drive additional multiple expansion compared to the peak multiple of 25x averaged in 2021-2023.

However, when we factor in the prospect for EPS growth of 10%-13% per year between 2025-2027, the ensuing P/E to growth multiple of 2.45x on current year earnings looks rather rich. We’ve seen this before when the herd gets overexcited and breaks out the hopium for a particular company or sector.

In our view, that stretched valuation reflects the barrage of headlines and news stories about power needs. When we look at 2024 capital spending from several large electric utilities, including Dominion Energy D, Duke Energy DUK, American Electric Power AEP, Southern Co SO, Edison International EIX, Exelon Corp. EXC, Entergy ETR, and First Energy, the aggregated amount is up only 3.5% compared to 2023.

That is another reason to think the near-term valuation for ETN shares is stretched, especially given its exposure to the aerospace and vehicle markets.

To call ETN shares up to the portfolio, we would need to see either 2024 and 2025 EPS expectations jump considerably, see the shares pull back to a level that offers sufficient upside to get involved or a combination of both.

Closer to the $300 level would be a good place to begin a position in ETN shares as it would offer ~10%+ upside, and if the shares traced their way back to the 100-day moving average, currently near $287, we would likely become greater buyers of ETN shares.

At a minimum, with that same group of electric utilities poised to boost their capital spending by just over 10% in 2025, we will keep ETN shares in the Bullpen and on our radar.

More Pro Portfolio

- We're Adding to 3 Positions After the CPI and Retail Sales Reports

- Weekly Roundup: An Upward Drift Amid a Light Slate of Data

- Signals From Our Investing Notebook

At the time of publication, TheStreet Pro Portfolio had no positions in the securities mentioned.