CPI Data Shows Step in the Wrong Direction

Tomorrow brings the October PPI report, but it’s this data that will likely decide a December rate cut.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

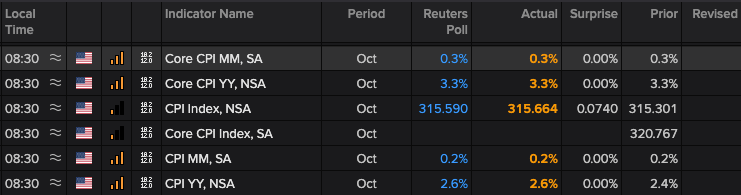

The October Consumer Price Index is out and, across the board, as you can see in the below table, the reported figures matched consensus forecasts. Because there was no headline surprise in the October CPI data, the initial market reaction saw the 10-year treasury yield dip and that helped lift equity futures. While there may be a sigh of relief from some, digging into the data that we see, at a minimum, core inflation remains sticky and still quite a distance from the Fed’s 2% target.

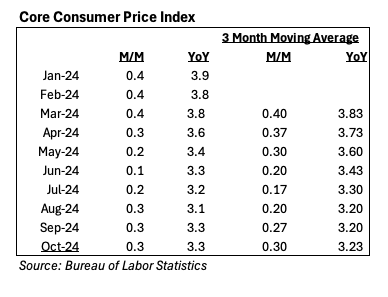

We see that when we examine reported core CPI figures on a month-over-month and year-over-year basis. In the table below, we see sequential core CPI data is hovering well above the June 2024 low of 0.1% while the trend in the three-month moving average analysis shows October sequential core CPI was back at May levels. Turning to the year-over-year core CPI data, the October data points to little progress while the tick higher in the year-over-year three-month moving average is a step in the wrong direction.

With five Fed speakers making the rounds today, we’ll be interested in how they frame today’s data in their comments, assuming they do at all. Tomorrow brings the October PPI data, which is expected to show core PPI ticking higher on both a sequential and year-over-year basis. If tomorrow’s data matches market forecasts like today’s October CPI data did, it would help build the case for the Fed to potentially take a policy pause at its December 18 meeting.

Following tomorrow’s PPI data, we will be keenly interested in what Fed Chair Powell has to say, but we recognize that he may not say much following last week’s policy press conference and the ample number of data points coming before the Fed’s December policy meeting.

Our view on whether the Fed ultimately decides to make a December rate cut or forego one will hinge on upcoming data that includes:

S&P Global Flash November Manufacturing & Services PMI (November 22)

PCE Price Index – October (November 27)

ISM Manufacturing Index – November (December 2)

ADP Employment Change Report – November (December 4)

ISM Non-Manufacturing Index – November (December 4)

Employment Report – November (December 6)

Consumer Price Index – November (December 11)

Producer Price Index - November (December 12)

As that data is had, we’ll update our thinking and the potential market reaction and position the Portfolio accordingly.