After Employment Report, We're Taking a Cautious Path

We see the same risks emerging as in April, when the Fed had to dial back rate cut expectations.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

*No surprise, the August Employment Report was weaker than market expectations, but it wasn’t a disaster

*Wage acceleration won’t go unnoticed by the Fed

*We see the report leading the Fed to start rate cuts with a 25-basis point move

*We disagree with the market seeing more than four rate cuts before the end of 2024

*The risk of the Fed walking back market expectations keeps us on a cautious path

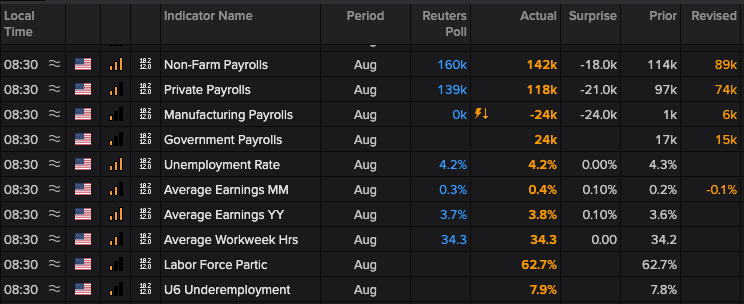

The report that the market has been waiting for is out and while it was a miss relative to the 160,000 jobs the market expected, the 142,000 jobs that were created tell us it wasn’t a total disaster.

Factoring in the revised July non-farm payroll figure of 86,000, the economy added 53,000 jobs in August, which was modestly ahead of the 46,000 that the market was looking for. As expected, the Unemployment Rate ticked lower, but what stands out was the rebound in average earnings, which rose 3.8% year over year, a tad warmer than July’s 3.6% figure.

That combination means the Fed’s likely course of action on September 18 will be a 25-basis point rate, but the lingering question will be how many additional cuts they pencil in with their updated set of economic projections.

Our thinking has been that one more rate cut is likely in the cards before the end of the year, and if that’s what the Fed depicts in its revised forecast, the odds of it upsetting the market are rising. We say this because, following the Employment Report, the CME FedWatch Tool now shows the market penciling in even more rate cuts for this year. Following the report, the CME FedWatch Tool shows the greatest probability for the Fed Funds rate to be 400 BPS to 425 BPS exiting 2024 versus the current range of 525 BPS to 550 BPS.

If you’re thinking that the market is once again out over its skis when it comes to Fed rate cuts, we’re right there with you. The more likely path is for the Fed to dial back policy over time, but to leave enough flexibility to act if the economy softening picks up speed. This opens the market to the downside risk that we’ve talked about and that we saw unfold last April when the Fed had to walk back the market’s expectation for rate cuts. That risk is going to keep us on the cautious path ahead of the Fed’s policy meeting.

As the Fed enters its blackout period on Saturday ahead of its September 18 policy decision, given the market’s reaction to the August Employment Report, we’ll want to pay extra close attention to Fed Governor Christopher Waller when he speaks at 11 a.m. ET. Waller is likely to agree the Fed is that much closer to start cutting rates and what we’ll want to listen for is any sense as to how big that first rate cut could be.

One call out in the data was the jump in construction employment, which added 34,000 jobs during August. That increase suggests a further pick up in construction activity as the un-seasonally wet July was put into the rearview. We see that offering support for our shares of Vulcan Materials VMC and United Rentals URI.

What’s not depicted in the summary table for the August Employment Report is the total revision to the June and July Employment Reports. The total change to those reports showed 86,000 fewer jobs were created than previously thought, and odds are that the number of jobs created in August will be revised lower as well. That would keep the trend of slower job growth intact and put it on closer footing with other data received this week.

At the time of publication, TheStreet Pro Portfolio was long VMC and URI.