While Large-Cap Indexes Head North, More and More Stocks Head South

Here's why market risk may outweigh potential right now.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A warning signal?

While major equity indexes closed closed near their session highs Tuesday, we would highlight the fact that the new closing highs are occurring with cumulative market breadth bearish and at near-term lows for the All Exchange, NYSE and Nasdaq. We regard this deterioration as a warning signal that while the large-cap indexes may be making new highs, more and more stocks are heading south, weakening the underlying market structure.

Two of the three sentiment indicators (contrarian indicators) continue to caution as the “crowd” remains overly bullish while forward valuation of the S&P 500 remains very extended above ballpark fair value.

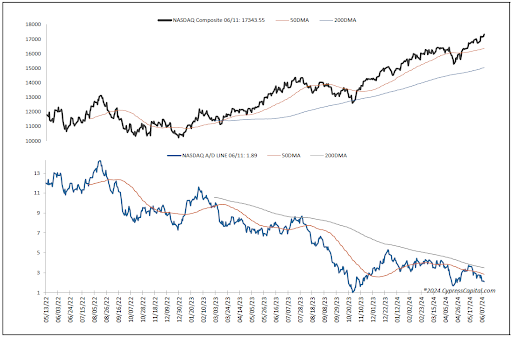

S&P at New High as Breadth Deteriorates Further

On the charts, the major equity indexes closed mixed Tuesday with negative NYSE internals while the Nasdaq’s were mixed. Most closed near their session highs with three of the indexes posting new all-time highs with the rest either in neutral or bearish near-term trends.

The Nasdaq saw negative breadth but positive up/down volume.

So, while the S&P 500, Nasdaq Composite and Nasdaq 100 made new closing highs, largely due to one mega-cap name, the rest declined, leaving the S&P, Nasdaq Composite and Nasdaq 100 in near-term bullish trends, the DJIA and Dow Jones Transports neutral and the MidCap 400 and Russell 2000 bearish.

We would highlight that while the high visibility indexes continue to grab headlines, cumulative market breadth is flashing red with the advance/decline lines for the All Exchange, NYSE and Nasdaq bearish and making new near-term lows suggesting the underlying structure continues to erode and worthy of concern.

No new stochastic signals of import were generated.

Investor Sentiment Remains Cautionary

Overall, the data remain mixed.

The 1-Day McClellan Overbought/Oversold Oscillators are neutral except for the NYSE being oversold (All Exchange: -45.85 NYSE: -61.18 Nasdaq: -37.42).

The percentage of S&P 500 issues trading above their 500-day moving averages (contrarian indicator) slipped 44% staying neutral.

However, the detrended Rydex Ratio (contrarian indicator) remains bearish with the leveraged ETF traders leverage long at 1.13.

This week’s AAII Bear/Bull Ratio (contrarian indicator) rose to 0.68 and is neutral.

The Investors Intelligence Bear/Bull Ratio (contrary indicator) is bearish at 18.2/57.2 as bulls well outweigh bears.

The Open Insider Buy/Sell Ratio remains neutral at 36.4.

Leveraged ETF sentiment is -3.8, remaining neutral.

Valuation Concerns

The 12-month consensus earnings estimate for the S&P 500 from Bloomberg dipped to $253.11 per share. Of note, its forward P/E multiple is 21.2x and remains well above the “rule of 20” ballpark fair value at 15.6x. This remains an important concern for us as a 500-basis point premium remains significant.

The S&P's earnings yield is 4.71%.

The 10-Year Treasury yield dipped to 4.4%. Support is 4.32% and resistance is at 4.47%. Its intermediate-term trend is neutral.

The U.S. dollar, via the UUP ETF, closed higher at $28.88. It is neutral with support at $28.59 and resistance at $28.90.

Bottom Line

Market breadth, sentiment and valuation continue to suggest caution for equities in general.

We honor sell signals on individual names while being extremely selective on the buy side. In our opinion, overall market risk outweighs potential.

At the time of publication, Ortmann had no positions in any securities mentioned.