Wall Street Still Has Too Many Potholes for My Liking

Sure, AI is back, the producer price index got the market riled up, and recession fears are dissolving. But here's why I'm cautious.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We got some market catalysts, no doubt. Artificial intelligence came back with a vengeance. Inflation seems to be under control -- by recent standards -- which has helped markets. Even investors were excited over the producer price index.

Suddenly, recession fears seems to be evaporating.

But I'm not completely sold that risks are gone. Indeed, one thing makes me very cautious on position size right now. It's the lack of liquidity in both directions. Moves up and down seem amplified relative to the data or catalyst for the moves.

Let's break this down.

We get Jackson Hole this week. During the financial crisis, this event provided a great forum for then-Fed head Ben Bernanke and others to set out policy shifts (sometimes radical policy shifts). But don't expect much this time around. The topic is “Reassessing the Effectiveness and Transmission of Monetary Policy.” While we could glean some information about future Fed decisions, they will likely try to avoid that and focus on how the Fed will behave in some more distant future. Personally, I think quantitative easing should be categorized as a “nuclear option,” and only used when absolutely necessary, and on the smallest possible scale, for the shortest period of time, but that is unlikely to occur.

The Fed minutes might tell us how close the group was to cutting in July (we think it should have), but again, that seems largely priced in now.

With the market pricing in cuts at a pace only marginally faster than our base case, I’m not expecting a lot of movement in bonds or stocks based on the Fed this week.

Earnings. Nvidia NVDA isn’t until Aug. 28. Other earnings will matter. Artificial intelligence is important, and it was incredibly important that in a recent earnings release Walmart WMT highlighted how important AI had been in driving its performance. The one thing we’ve been looking for is “AI Success” stories. Not from the companies that benefit from AI adoption, but from AI users. That note fit the bill and more notes like that will convince us that valuations might not have gotten ahead of themselves in the space. The other thing we will all be looking for is anything that points to the direction of the economy and the consumer.

The U.S. Election. I remain wedded to the view that as the campaign heats up and policies get announced, we will realize that large annual budget deficits are on the horizon regardless of who wins.

Geopolitical Risk. The risks of some accident occurring between China and the Philippines has decreased. Iran seems to have decided not to retaliate and there are signs that we may see a calming in the Middle East. It remains to be seen how Russia decides to retaliate against Ukraine for their incursion into Russia.

The Economy. This is probably the most important thing for markets, but we don’t get that much information this week. Suddenly the market has convinced itself that recession risk is back to being off the table.

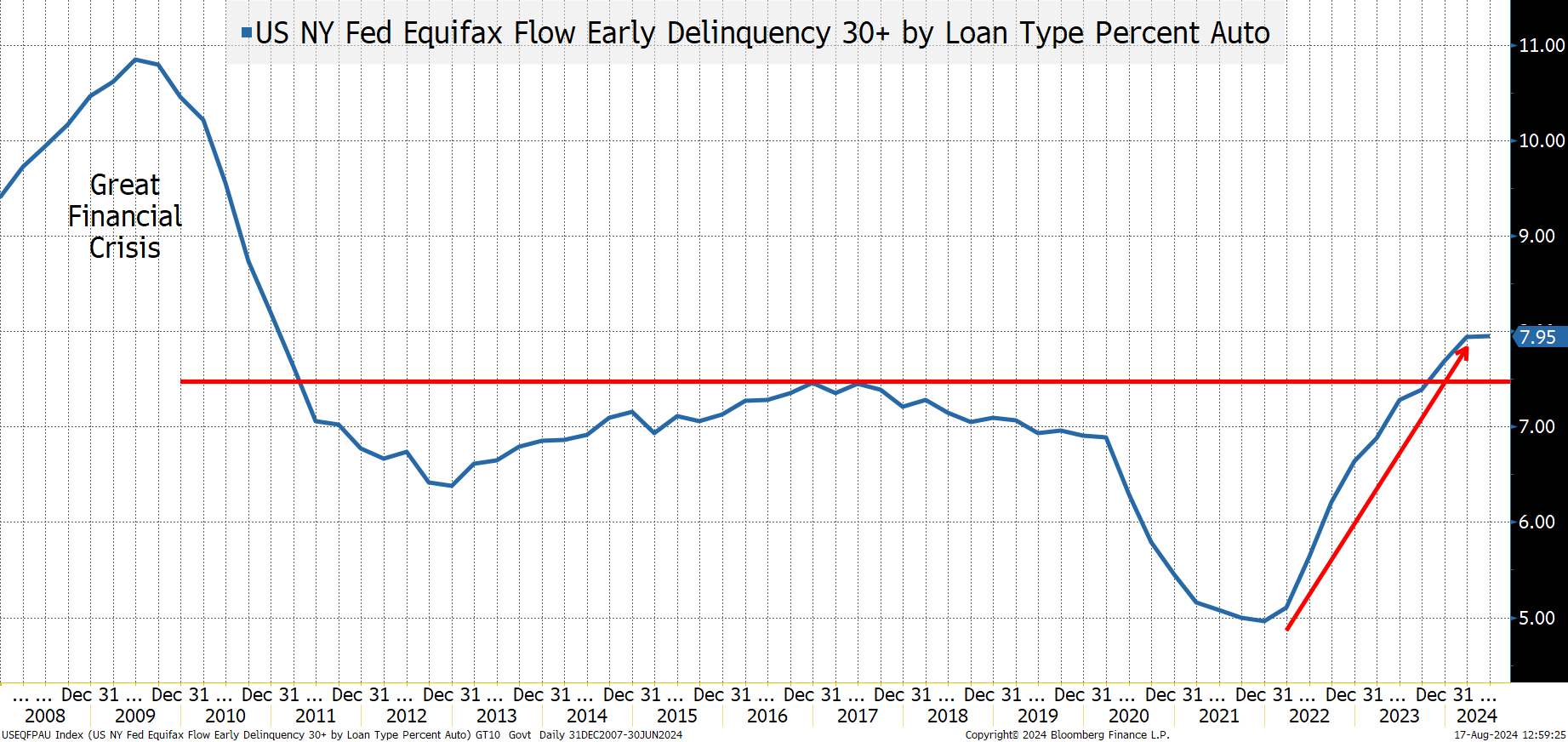

While retail sales did rebound, the control group weakened and we have seen mostly downward revisions on this economic series (like many others). This period also covered “Amazon Prime Day,” which may have pulled forward demand as not only were there sales on Amazon, but there were many other competing sales occurring to compete. Finally, much of the boost to sales was due to autos, an industry, where the stocks have been struggling and I’m hearing more about dealer inventory issues than outsized demand.We are seeing delinquency rates on auto loans creep above levels seen since after the great financial crisis.

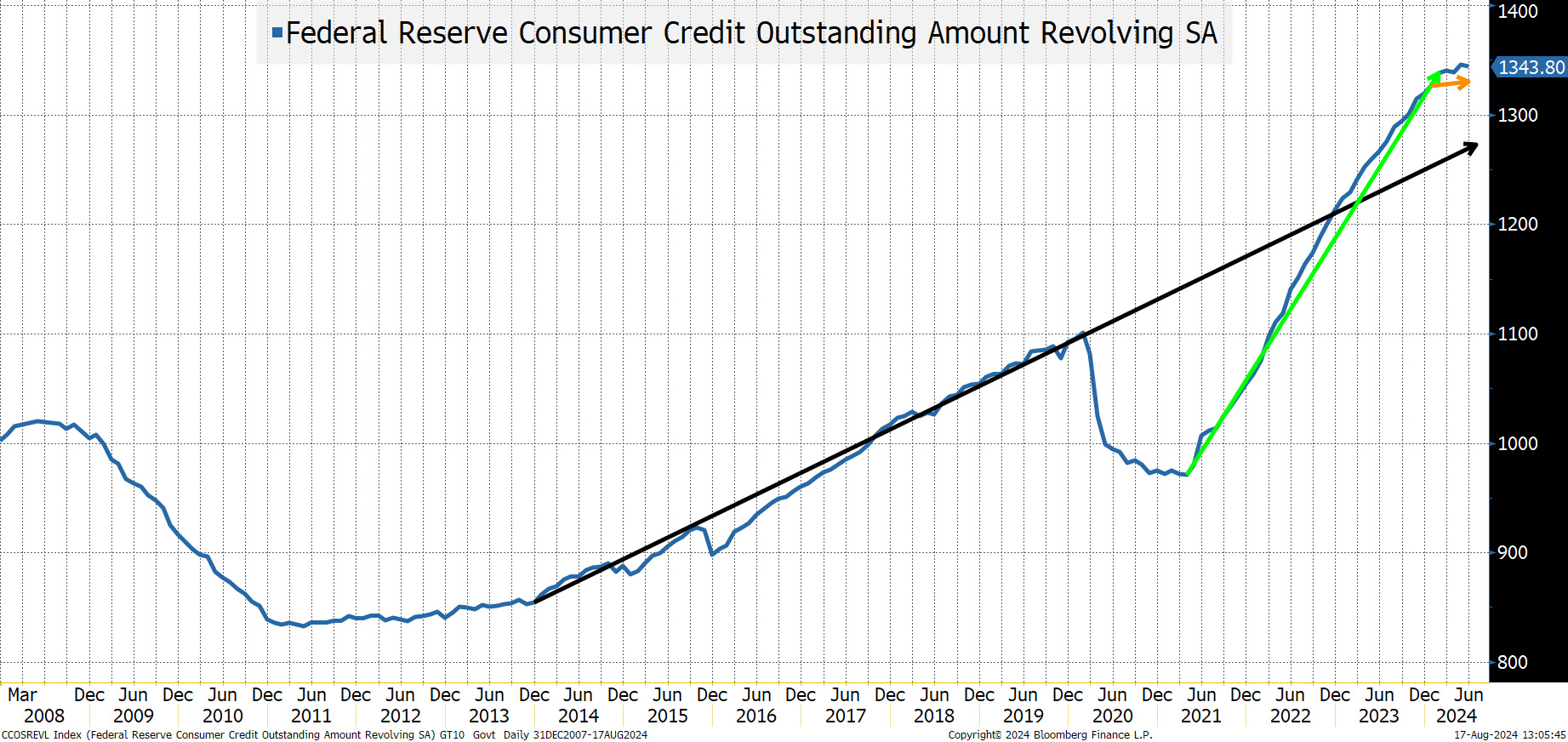

While we have seen delinquencies increase, we’ve seen consumer credit growth slow – possibly in response to delinquencies, or consumers that are getting tapped out. I think the consumer is in questionable shape and last week’s retail sales number is an anomaly rather than the norm. We won’t have much clarity on the economy until the first week of September when the jobs reports start hitting, but I am leaning towards investors getting concerned about recession risk.

Bottom Line

We're far from out of the woods on the economy and markets. Stocks staged an impressive rally last week but a lack of liquidity helped push markets further on data than they might have moved otherwise. We never saw panic - a touch of fear, but not panic. And while not back to full froth, it seems clear that we are back in greed mode.

The most bullish information that I’m trying to work into my analysis is the actual praise of AI by a user, which we had not seen enough of, and this could turn the tide.

I’m still in the crowd that says we'll get some sort of the “bumpy” landing on the economy.

I’m not doing much at these levels, in terms of repositioning my equity portfolio, which is currently underweight equities. I’m looking to sell some closed-end municipal bond funds, but patient there, too, as they didn’t rally as much as they could have when yields went to 3.8% on 10’s.