Wall Street: Russia Risk Is So Yesterday (or ... Is It So Tomorrow?)

We're seeing a risk-on mood on the market. Also, a look at political plays, the buck, breadth, jobs and home sales.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Is risk on? Sure. In a way. Markets overcame the escalation of the war in eastern Europe by both sides. One might have thought financial markets would stall as Ukraine strikes inside of Russia using Western missiles and as Russia sends NATO powers a clear message through the use of different weapons with longer maximum effective ranges. The market blinked overnight into Thursday morning and still showed caution as Thursday morning wore on.

After that, it was "game on," as Mr. Market decided these escalations might not be today's problem. Actually, if not pushed past a certain limit, these gyrations by both sides ahead of a transition of power in the U.S. that is expected to press for peace, might be considered a deadly form of negotiation. Perhaps markets are already thinking about pricing in some kind of peace premium along with expectations for a more pro-business, less regulatory environment in the U.S.

Such an environment would certainly lead to increased cross-border investment into the U.S., which would likely increase U.S. dollar valuations vs. reserve currency peers. That would be deflationary and could counteract the inflationary impact of whatever tariffs end up being more than negotiatory in nature. If all economic impacts are to be transactional in a Trump 2.0 economy, then maybe that's exactly what we are starting to see.

While likely volatile, at least during this pre-transitional period, this could ultimately develop into fertile ground for economic growth. Organic economic growth, born of private sector activity and a broad increase in velocity, not one artificially created through the expansion of money supply and fiscal recklessness.

Regardless of the zero-dark hour ramblings of your semi-favorite self-sufficient madman, overnight U.S. equity indices appear to be setting up for some Friday morning. We'll know for real in a few short hours, won't we?

On Gaetz

I've seen a few respected news outlets refer to the Matt Gaetz fiasco as a "Trump Loss." I mean, is that just posturing? If the media could not even recognize that the short-lived nomination of Rep. Matt Gaetz of Florida to the post of U.S. Attorney General was a Trojan Horse of sorts meant to get something in exchange or to better position the president-elect's "real" choice for the job, then why do we even read them or listen to them?

I am not trying to be political, and I am not showing favor, but I can recognize a game of chess when I see it.

Marketplace

Russia's intentional threat to U.S., British and EU assets did manage to put a bid under the U.S. dollar on Thursday. The U.S. Dollar Index, also known as the "dixie" popped on Thursday and into very early Friday morning. The index grazed the 108 level (which is very strong) overnight, as the euro, pound, yen, franc, and yuan all showed relative weakness.

U.S. Treasuries have also exhibited some overnight strength after showing some mild weakness on Thursday. Overnight, the yield for the U.S. Ten Year Note has dropped 4 basis points to 4.39%, as the yield for the U.S. Two-Year Note has dropped 3-basis points to 4.33%. This less than panicked form of haven seeking has allowed gold and especially Bitcoin to gain in dollar terms, which means that in almost any other terms these alternative investment vehicles are even stronger than they appear to us here in the states.

Domestic equity markets were strong on Thursday. Yes, mega-cap tech had an issue, as the Department of Justice officially threatened to break Alphabet GOOGL into parts. That stock was down 4.74% for the session as Amazon AMZN gave up 2.22% in sympathy. That left the Nasdaq Composite up just six pointy or 0.03%. Everything else did better. The S&P 500 gained 0.5% for the session as the smaller caps roared. The Russell 2000, S&P 600 and S&P 400 all gained between 1.65% and 1.66%. How's that for in-line, uniform performance? Algorithms can do that.

Breadth

Ten of the 11 S&P sector SPDR exchange-traded funds shaded into the green on Thursday as six of them gained more than 1% for the session. Perhaps oddly, on a "risk-on" day, the Utilities XLU led the way, followed less surprisingly by the Financials XLF and Industrials XLI. Communication Services was the only loser in the bunch thanks to the above-mentioned weakness in internet names.

Winners beat losers by a 7-to-2 margin at the NYSE and by roughly 2-to-1 at the Nasdaq. Advancing volume took a commanding 77.8% share of composite NYSE-listed trade and a 67.4% share of composite Nasdaq-listed activity. Most importantly, aggregate trading volume on a day over day basis, was up 12.1% for NYSE-listings and up 5.2% for Nasdaq-listings.

What Does That Mean?

Take a look...

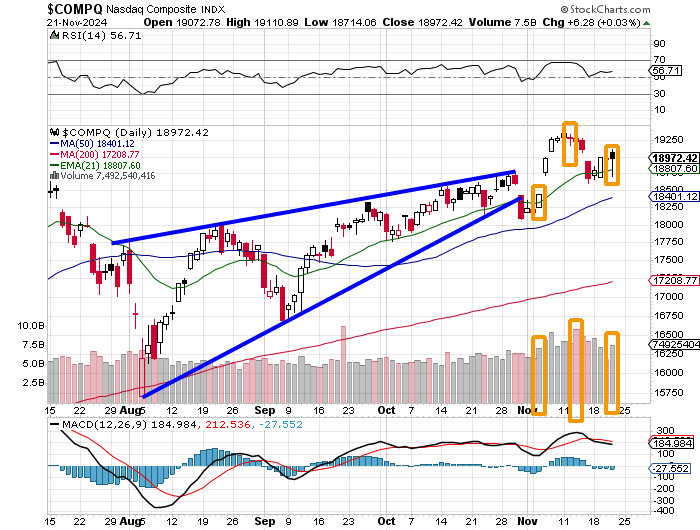

For the third time since the start of November, or really since the three-month rising wedge pattern closed, the Nasdaq Composite has presented us with a potential "Day One" changing of trend. The first two of these, while not really changing the landscape for investors, have worked marvelously for traders.

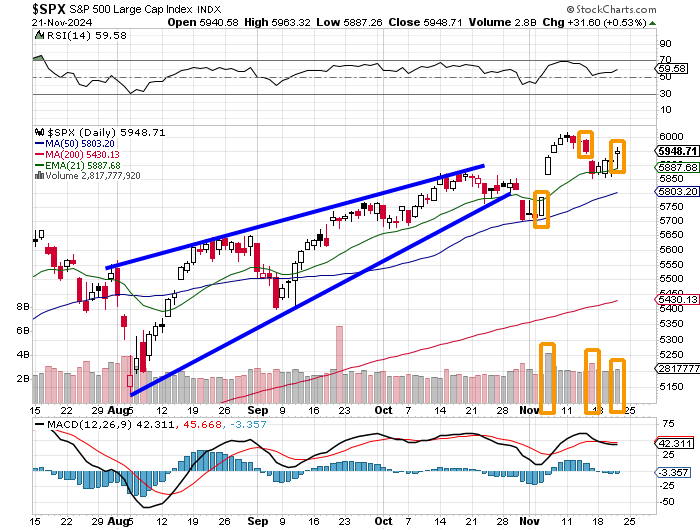

The chart of the S&P 500 is very similar in that it now provides a potential third "Day One" of November. There is a slight difference in the timing of the second Day One between the two indices, but the stories in place are similar.

The Macro

Is the economy gaining momentum or losing steam? Really, even for those of us who love this stuff, different stories are told by each data-point. The weekly print for Initial Jobless Claims fell for a fifth week in six on Thursday and is now back down to levels that Wall Street economists seem more comfortable with. That's positive.

The weekly print, however, for continuing jobless claims ripped much higher to 1.908 million people. While initial claims have remained subdued, continuing claims are now at their highest level since November 2021. What that means is that while layoffs have not really hit a torrid pace just yet, once unemployed, folks are staying unemployed. That's awful.

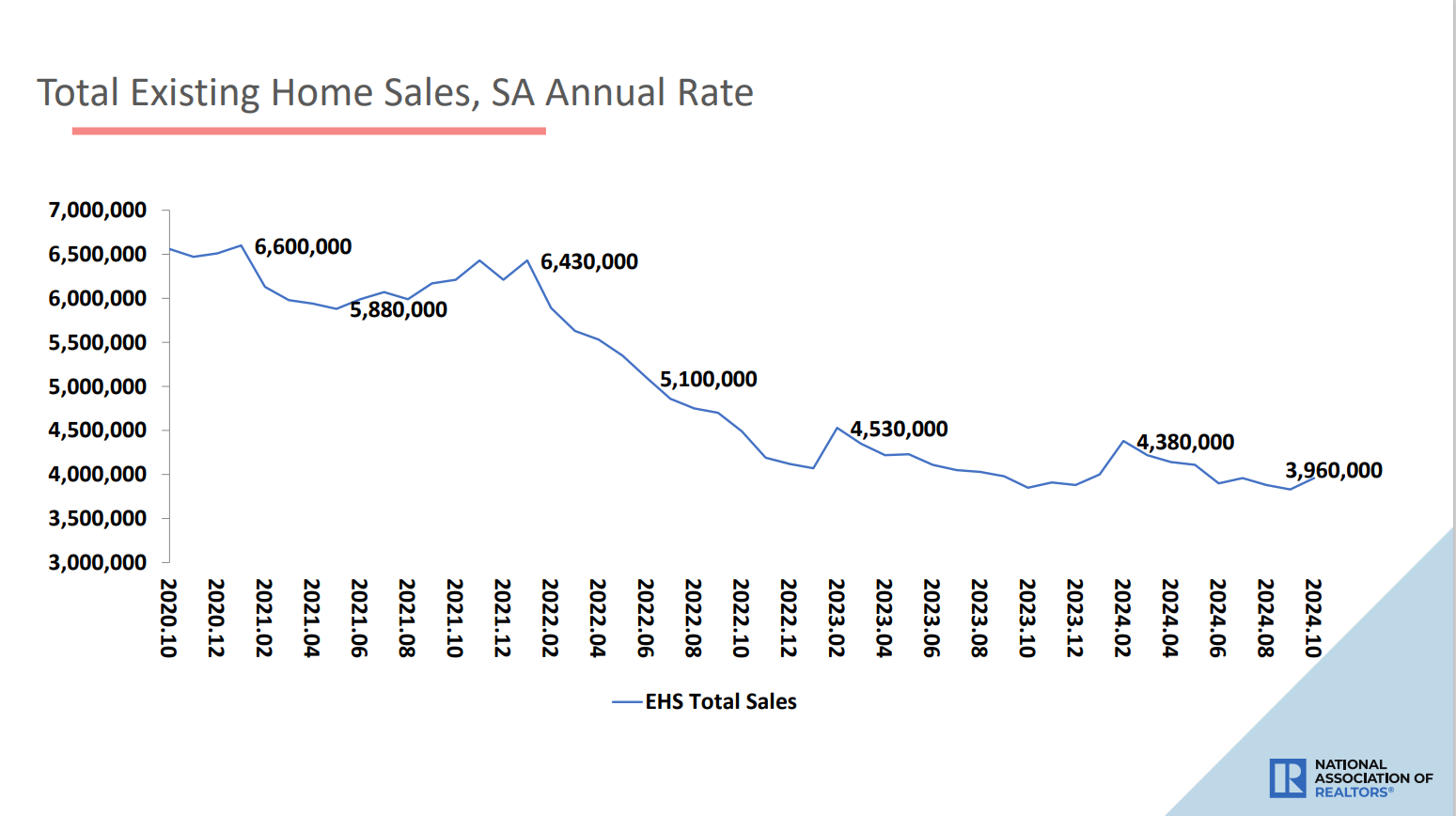

October existing home sales printed at an annualized and seasonally adjusted 3.96 million. That was up 3.4% month over month and as my pal Chris Versace pointed out to his crew at the Portfolio, up year over year. It had been more than three years since we had seen year over year growth for any month for this series. Still, this is what the chart for this series looks like since the year 2021, as provided by the National Association of Realtors in the material...

Again, this is awful. That brings us to the Conference Board's Index of Leading Economic Indicators, which for October printed at -0.4% month over month. This index, meant to give an overall picture of economic health or the lack thereof, has now printed in month over month contraction for eight consecutive months, and has exhibited month-over-month expansion for exactly one month in the past 31. That's right. According to the Conference Board's data, the U.S. economy went into recession more than two and a half years ago and has still shown no sign of climbing out of the mire. Remember, the Conference Board is not a government agency. Not that it means that the government agencies are not trustworthy, but this does need to be pointed out as government released data is often wildly inaccurate at first and then revised more than once over the following months.

Anyone Else Notice ... Bitcoin?

Bitcoin has retained its strength throughout the week, trading close to $99,500 per token overnight. That said, MicroStrategy MSTR took a 16% beating on Thursday, while Coinbase Global COIN was slapped around for almost 8%.

Did I Ever Tell You?

About the IT guy that worked for me about 17 or 18 years ago? He was buying Bitcoin, which I had never heard of, and he encouraged me to get involved. Bitcoin was trading at about $240 a token at the time. He had four of them in possession and wanted to buy more. I, of course, was too smart to follow his lead. He was a good guy. I wonder where he is now. He had served in the Czech Army during the Cold War, and we shared some anti-Soviet stories back and forth at the time. Wonder if he did buy more. Wonder if he held on or took profits. That guy was way ahead of his time. Would love to bump into him one more time.

Economics (All Times Eastern)

09:45 - S&P Global Manufacturing PMI (Nov-Flash): Expecting 48.8, Last 48.5.

09:45 - S&P Global Services PMI (Nov-Flash): Expecting 55.3, Last 55.0.

10:00 - U of M Consumer Sentiment (Nov-F): Flashed 73.0.

10:00 - U of M One Year Inflation Expectations (Nov-F): Flashed 2.6%.

10:00 - U of M Five Year Inflation Expectations (Nov-F): Flashed 3.1%.

1:00 p.m. - Baker Hughes Total Rig Count (Weekly): Last 584.

1:00 - Baker Hughes Oil Rig Count (Weekly): Last 478.

The Fed (All Times Eastern)

6:15 - Speaker: Reserve Board Gov. Michelle Bowman.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BKE (.90)

At the time of publication, Guilfoyle was long AMZN, XLU.