Trends Still Grumbling Despite Rally

Date is mostly neutral as valuation concerns continue.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

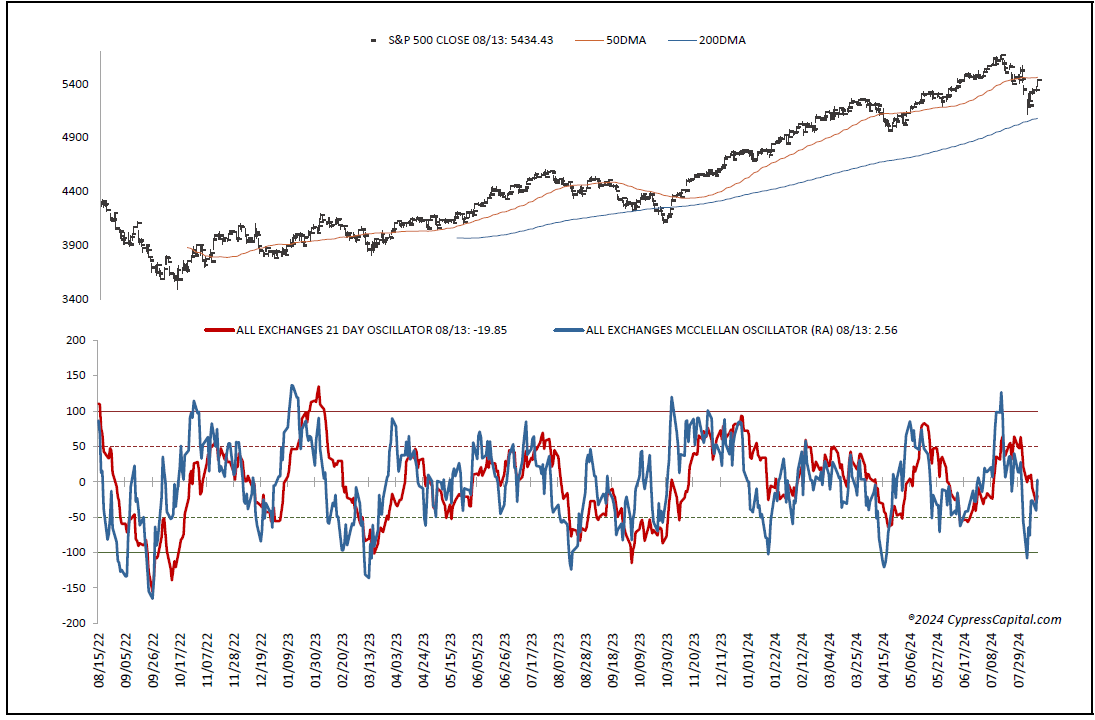

Yesterday’s release of the producer price index data pushed the major equity indexes higher, with positive internals on higher trading volume. But we're still seeing trends as bearish.

As a recap, all indexes closed near their highs of the session, but the gains were not strong enough to alter their near-term trends. Now, we'll have to see the response to the consumer price index report, which turned out a 0.2% month-over-month rise for the headline and core.

The Technicals

Cumulative breadth saw some encouraging movement, as it turned bullish from neutral.

On the charts, all the major equity indexes closed higher yesterday with positive internals on heavier trading volume. All closed near their session highs with all but the Dow Jones Transports closing above resistance.

Yet the rally was not strong enough to shift any of the index near-term trends that remain bearish on all but the mid-caps and Russell 2000 small caps that are neutral.

On the other hand, breadth was strong enough to shift the cumulative advance/decline lines for the All Exchange, New York Stock Exchange, and Nasdaq to bullish from neutral.

The data overall is largely neutral, including the one-day McClellan overbought/oversold Oscillators (All Exchange: 2.56; NYSE: 11.78; Nasdaq: -4.22).

The percent of S&P issues trading above their 50-day moving averages, a contrarian indicator, rose to 59% and is neutral.

The detrended Rydex Ratio, also a contrarian indicator, rose to 0.72, but remains neutral as well.

This week’s American Association of Individual Investors Bear/Bull Ratio, a contrarian indicator, also stayed neutral at 0.73.

But the Investors Intelligence Bear/Bull Ratio, a contrary indicator, stayed bearish at 26.15%, with investment advisor bulls continuing to outweigh bears by a wide margin. We continue to believe the “wall of worry” still needs to see some further strengthening.

The Open Insider Buy/Sell Ratio dipped slightly to a neutral 45.1%.

Valuation and the Buck

Valuation remains a concern. The forward valuation of the S&P based on Bloomberg’s forward 12-month earnings estimates took another hit that leaves it still very extended above ballpark fair value. The 12-month consensus earnings estimate for the S&P from Bloomberg dropped to $250.55 from $250.83. That leaves its forward price-to-earnings of 21.7 still well above the “rule of 20” ballpark fair value at 16.2. We believe this premium remains significant.

Its earnings yield declined to 4.61%.

At the same time, the 10-year Treasury yield slipped to 3.85%. Support is 3.79% and resistance at 3.97%. Its near-term trend is bearish.

The U.S. Dollar, via the Dollar Index Bullish Fund UUP, closed lower at $28.42. Its trend is bearish with support at $28.30 and resistance at $28.60.

The Bottom Line

At this point we continue to believe that we are still lacking enough evidence to suggest the current market correction has seen its lows, despite the recent improvements. We're watching the response to the CPI, but we remain cautious in our near-term expectations until more evidence is presented to suggest a change.