Treasury Hacked, Chicago PMI Whacked and ... Santa Hopes Dashed?

Let's look at a major cybersecurity breach, how the Santa Claus rally might be skipping Wall Street, weakness in a key Institute for Supply Management indicator, and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

News broke on Monday afternoon that the U.S. Treasury Department had notified legislators that the agency had been hacked by a Chinese state-sponsored actor through a third-party software provider in what the department described as a "major cybersecurity incident." The hacker was able to access certain Treasury workstations and some unclassified documents.

According to Bloomberg News, the U.S. Treasury Department was notified on Dec. 8 by the software provider, BeyondTrust, that a hacker had broken through and had gained unauthorized access to "a key used by the vendor to secure a cloud-based service" providing tech support to users at the department. BeyondTrust currently holds contracts worth more than $4 million with the federal government, specifically working for the departments of the Treasury, Defense, Justice, Veterans Affairs and other agencies.

This comes at a time that the White House is investigating what is described as a vast cyber-espionage campaign against U.S. telecommunications companies by Chinese state-sponsored actors. According to the White House, nine telecommunications companies have been impacted by these attacks by a group nicknamed "Salt Typhoon." In response to this news, the Chinese embassy in Washington said in a statement: "The US needs to stop using cybersecurity to smear and slander China and stop spreading all kinds of disinformation about the so-called Chinese hacking threat."

The New York Times has reported that the Salt Typhoon hackers had also targeted smartphones used by Vice President Kamala Harris campaign staffers as well as President Elect Donald Trump, Trump family members and Vice President Elect JD Vance.

... About the Debt Limit ...

This news came after Treasury Secretary Janet Yellen warned on Friday that the Treasury Department will likely have to begin making special accounting maneuvers in mid-January, perhaps around the 14th of the month, to avoid breaching the U.S. debt limit. Apparently, the debt ceiling will be re-established on Jan. 2 and according to Yellen in a note written to several congressional leaders, on that date, "The new debt limit will be established at the amount of outstanding debt."

Total U.S. debt is set to decrease by $54 billion on that date as well, thanks to the expected redemptions of securities held by a federal trust fund. As of Dec. 26 (last Thursday), the Treasury had a cash position of $689 billion. Incredibly, the U.S. still announced on Monday, almost $5.9 billion in additional military and economic aid to the Ukrainian government with $1.25 billion coming from U.S. military stockpiles, $1.22 billion coming from the Ukrainian Security Assistance Initiative and a $3.4 billion disbursement in direct budget support from the US Treasury Department.

The Selloff

It appeared that the selloff that has hit U.S. equity markets has materialized out of a need or inclination to take profits and tax losses ahead of the new year. Certainly, the above news that the Treasury Department is less secure than it should be did not help. News that the Treasury is running out of its ability to borrow did not help. News that the Department continues to allocate what cash it has in ways that should probably be highly discretionary ahead preparing to move toward having to take special measures just to run the government did not help.

The macro really did not have that much of an impact on Monday. Home prices were hotter than expected in October, according to both Case-Shiller and the Federal Housing Finance Agency. November Pending Home Sales were much stronger than expected. Then there were two real surprises that almost contradicted each other. The Dallas Fed Manufacturing Index printed in a state of expansion in December for the first month since April of 2022. That's right, manufacturing as a business in the Fed's Dallas district had contracted for 31 consecutive months from the month prior. Until now. A 32nd month of contraction had been expected.

No such luck in Chicago. The Chicago PMI, as measured by the Institute for Supply Management and which covers business activity, which is far broader than merely covering the manufacturing or services sectors alone, printed at an incredibly weak 36.9. This was the 13th consecutive month for decreasing business activity in the Chicago region and the third month among those 13 that the headline number fell below 40, which is seen as a sign of extreme economic weakness. December was also the 27th month in the past 28 that economic activity decreased from the month prior in the Chicago area. Don't forget, the economy is surprisingly strong, they said.

About that Economy...

The Atlanta Fed's GDPNow model for the fourth quarter is running at growth of 3.1% quarter over quarter, at a seasonally adjusted annual rate. The model has not been updated since Christmas Eve, but will be revised this Thursday on the first business day of the year. Atlanta, however, is something of an outlier among its peers. Among other regional Fed districts modeling fourth quarter gross domestic product in real-time, New York is at growth of 1.86%, Cleveland is at growth of 1.85% and St Louis is at growth of 1.27%.

Currently, Fed Funds Futures trading in Chicago are pricing in an 89% probability that the Federal Open Market Committee stands pat on Jan. 29, but a 54% probability that the Fed implements a quarter-percentage point rate cut on March 19. There is just a 58% likelihood that the Fed even cuts the Fed Funds Rate more than once in 2025.

There is not yet a market for a rate hike, despite the renewed acceleration of consumer-level inflation. The Cleveland Fed sees December headline consumer price index at growth of 2.86%, while Hedgeye's model shows December around 2.94% with a range. Readers will recall that the CPI bottomed at 2.4% in September.

Marketplace

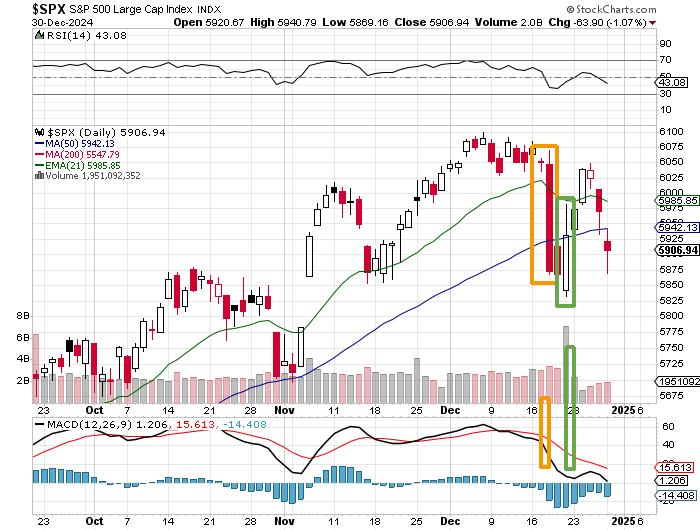

Is Santa dead? He may be. The S&P 500 is down 1.1% since the start of the Santa rally period. This would be the second year in a row that Santa did not show if this beat-down holds through Friday. Prior to that, Santa had seven consecutive winning seasons. On Monday, stocks were weak, despite strength in longer dated U.S. Treasuries. The risk-off move coupled with the safety move on the Treasury side, was likely a side effect of sloppy congressional fiscal policy that in turn has been mismanaged by the Treasury Department.

The S&P 500 gave up 1.07% on Monday as the Nasdaq Composite surrendered 1.19%. This was a third consecutive losing session for both of our major indexes. The S&P 500 is now in negative territory for the month of December. The selloff on Monday was broad, as small- to mid-cap stocks, the Dow Transports, and tech stocks all caught a beating. All 11 S&P sector SPDR exchange-traded funds closed in the red for a second-straight day.

Losers beat owners at the NYSE by a little less than 2 to 1 and at the Nasdaq by a rough 7 to 4. Here's where it gets a little interesting. Advancing volume took just a 27.8% share of composite NYSE-listed trade, but a surprising 54.2% share of composite Nasdaq-listed activity. Aggregate trade was about 8% higher on a day over day basis for names domiciled at both exchanges, but that advancing volume at the Nasdaq shows that there are interested buyers at these levels. Like I said, interesting.

Key To Note on the S&P ...

The S&P 500 lost its 50-day simple moving average on Monday, but did not break contact with that line.

There could be an attempt to rally the index this morning. The Nasdaq Composite is not quite in the same technical jam that the S&P 500 is. Keep in mind that the low of the upward change in trend day has not been taken out and that trading volume since that day has been just a fraction of what traded that day.

Economics (All Times Eastern)

08:55 - Redbook (Weekly): Last 5.9% y/y.

09:00 - Case-Shiller HPI (Oct): Expecting 4.1% y/y, Last 4.6% y/y.

09:00 - FHFA HPI (Oct): Expecting 0.5% m/m, Last 0.7% m/m.

16:30 - API Oil Inventories (Weekly): Last -3.2M.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle had no position in any security mentioned.