This Deterioration in the Market’s Foundation Shouldn't Be Ignored

Breadth is souring as sentiment turns more cautious.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Thursday brought more new closing highs for several of the major equity indexes. Excuse us if we aren't celeberating.

We are becoming more concerned regarding the possibility of a near-term break in the markets as cumulative breadth continues to deteriorate. Thursday’s advance/decline data was broadly negative as the underlying structure of the market weakened further. More stocks are declining in price opposed to what the weighted averages are suggesting.

Meanwhile, investor sentiment (contrarian indicator) finds two of the three data points back on red lights with the crowd overly bullish. So, while we may have been sounding a bit like “Chicken Little” lately, the caution signals continue to intensify.

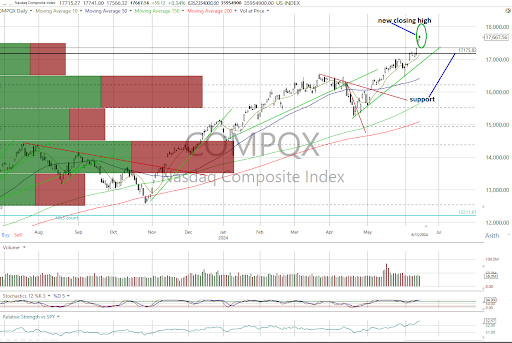

More New Closing Highs on Negative Breadth

On the charts, the major equity indexes closed mixed Thursday with new closing highs being achieved on the S&P 500, Nasdaq Composite and Nasdaq 100 as the rest posted losses.

We believe it important to emphasize that the large-cap indexes advanced with both the NYSE and Nasdaq advance/decline data negative by an almost 2:1 margin. Cumulative market breadth has continued to weaken to the point that the a/d lines for the All Exchange and Nasdaq are in deepening bearish trends with the NYSE neutral. Such deterioration implies the market’s foundation continues to deteriorate and should not be ignored.

While there were no changes on the index near-term trends that left the S&P, Nasdaq Composite and Nasdaq 100 bullish, the DJIA, Dow Jones Transports and MidCap 400 neutral and the Russel 2000 bearish, both the MidCap and Russell violated their 50-day moving averages as the Dow Transports closed below support.

We do not find the technical picture encouraging.

No stochastic signals of import were generated.

Breadth Sours as Sentiment Turns More Cautious

The data remain mixed.

The 1-Day McClellan Overbought/Oversold Oscillator are neutral (All Exchange: -35.36 NYSE: -43.96 Nasdaq: -29.93).

The percentage of S&P 500 issues trading above their 50-day moving averages (contrarian indicator) dipped to 46% staying neutral.

Of note, the detrended Rydex Ratio (contrarian indicator) shifted back to bearish at 1.13.

This week’s AAII Bear/Bull Ratio (contrarian indicator) rose to 0.68 and is neutral.

The Investors Intelligence Bear/Bull Ratio (contrary indicator) is bearish at 18.2/57.2 as bulls well outweigh bears.

The Open Insider Buy/Sell Ratio remains neutral at 40.0.

Leveraged ETF sentiment is 5.1, remaining neutral.

Elevated Valuation

The 12-month consensus earnings estimate for the S&P 500 from Bloomberg rose to $253.20 per share. However, its forward P/E multiple rose to 21.5x and remains well above the “rule of 20” ballpark fair value at 15.8x. It remains an important concern for us as a 500-basis point premium remains significant.

The S&P's earnings yield is 4.66%.

The 10-Year Treasury yield dropped to 4.24%. Support is 4.22% and resistance is at 4.41%. Its intermediate term trend is neutral.

The U.S. dollar, via the UUP ETF, closed higher at $28.86. It is neutral with support at $28.59 and resistance at $28.90.

Bottom Line

Market breadth, sentiment and valuation continue to suggest caution for equities in general.

We see the tide as shifting, which requires further honoring of sell signals on individual names while staying very selective on the buy side