The VIX Was Cruising at 65. Now Let's Send in the Reality Police

Here's what makes me nervous about how investors are interpreting the big move on Monday.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What does it really mean for the Volatility Index to hit 65 on Monday? You might be surprised.

The official VIX calculation clocked in at 65.73 on Monday at 8:34 a.m. ET. That level is now used by many people to justify long positions in equities. The theory seems to be that we had an “epic” spike in volatility indicating panic, and that panic has since receded – hence creating a buying opportunity. Notice, that we chose to use the word volatility here, partly because many seem to use VIX and volatility interchangeably – which is not accurate.

Normally I’d just leave this alone, but that so many people are taking comfort in a supposed volatility spike and that it is supposedly over, that it all makes me incredibly nervous.

Let me explain, starting with some background on the VIX.

Let’s go back to September 2017, when the Wall Street Journal published "Could Some VIX-Related Funds Go “Poof” in a Day?" It was one of the most interesting articles I’ve worked on. We were quite alone on the view and the author received major pushback, particularly from the exchange-traded fund providers.

We turned out to be correct, as on March 4, 2018, the WSJ published "A VIX-Related Fund Did Go “Poof’."

We got that right, partly because we had spent a lot of time on VIX calculations.

We used the CBOE VIX – Volatility Index Methodology as our guide. It is not for the faint of heart. I also spent some time with Robert E. Whaley, the creator of VIX. He was generous with his time, in part because he was (and is) a professor at Vanderbilt University, which I also attended.

There is one final piece to the "VIX 65" puzzle that we have been discussing here in the past. The VIX only includes options expiring between 23 and 37 days. So, as the market has gravitated to "zero days to expiration" options, a much smaller percentage of total option trades involves trades that impact the VIX.

Fear and Calculations

There was fear, I concede that, but there was no panic, with this move. Also, traded price, in size, is always the best mark to market. Observations and calculations, no matter how sophisticated, are rarely better or more useful than actual live-traded prices. Even think to elections on how many people now prefer to look at betting markets than polls?

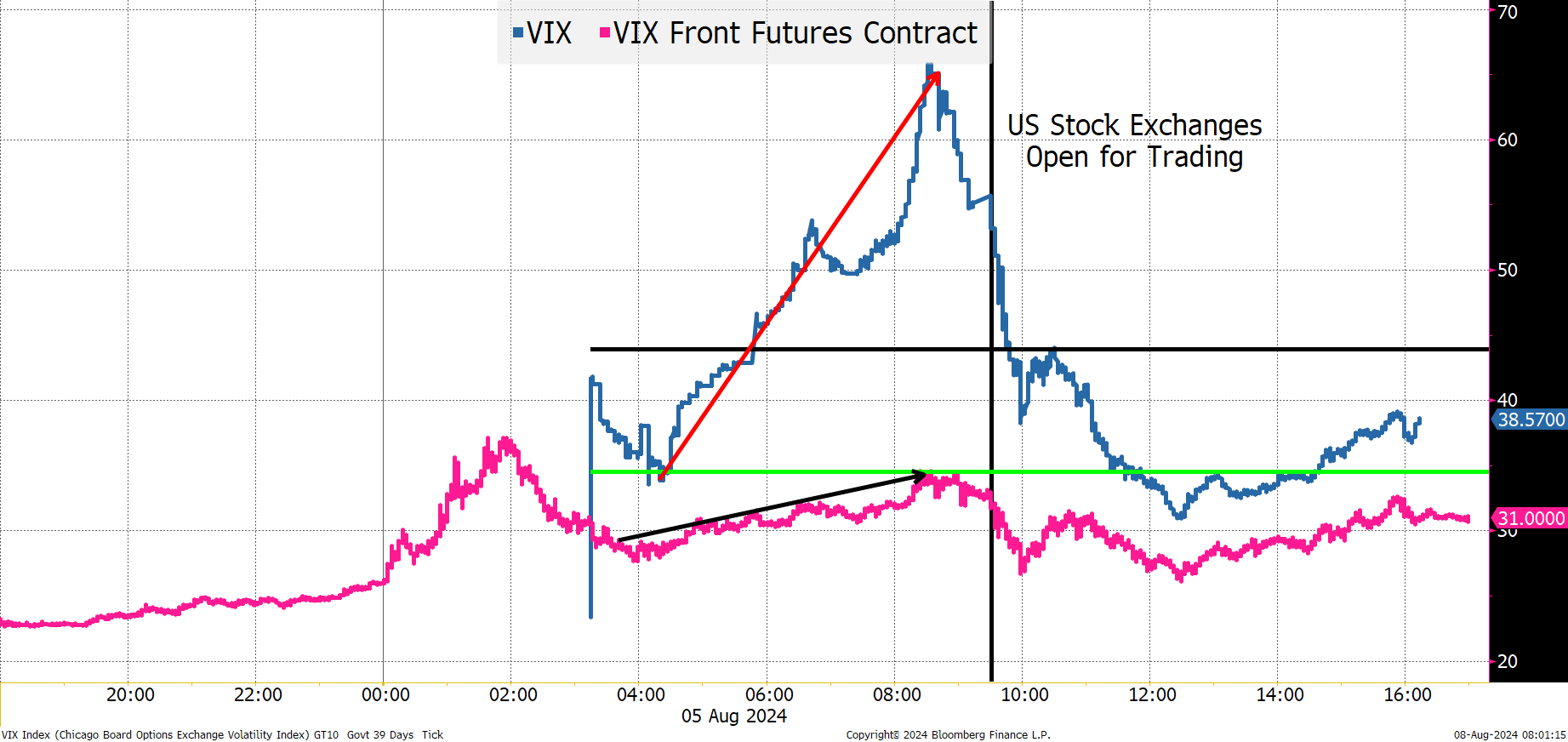

So let's examine the front VIX futures contract vs. the VIX calculation. What we see is that most of the time, the front futures contract follows the VIX calculation reasonably closely. The deviations are likely easily explained by future mechanics and the like, and are pretty negligible in the grand scheme of things.

The VIX calculation hit a high around 8:35 a.m. ET. It was going higher in a straight line from 4 a.m. until 8:30 am. The VIX futures contract, where people risk actual money, barely budged during that period.

VIX futures hit a local high around that same time, but it was only 34.2, up from 21.8 on Friday’s close. So, I’m supposed to trust a calculation rather than a traded price?

Let’s go further.

As the U.S. stock market opened, we see the VIX calculation drop rapidly. The gap between traded volatility (VIX futures) and some calculated amount dissipates rapidly.

The S&P futures did hit their low at 8:30 a.m., at a level of 5120. That market recovered as we neared the open and was at 5182 just after 10 am. So maybe, the fear in the markets subsided as we didn’t see “panic” selling on the open, but the moves in the VIX futures seem much more in line with what was occurring in the stock market than the VIX calculation.

Many of the avid options traders I know were complaining about abysmal liquidity in options that morning.

Wider bid/offer spreads affect the VIX calculation. Maybe relying on VIX calculation based on options markets before the U.S. cash markets officially open for the week is an issue? Pre-open (especially on Sunday night/Monday morning) and post-close markets can be thin and incredibly volatile. Super Micro Computers SMCI popped from roughly $620 to $727 to $550 in less than an hour after it released earnings Tuesday.

I am highly skeptical that the options prices going into the calculations for the VIX were even remotely accurate (away from the biggest, most active contracts) and that is why VIX spiked to seemingly incredibly levels (because they were incredible –- in the not-real sense -- while VIX futures seemed to behave much more like the market felt.

The same thing did not occur during the Covid peak where the difference between VIX at 82 and VIX futures at 73 seems pretty reasonable. We can argue that VIX and VIX futures were much more in line back during Covid, both showing real fear. The fear was extended over days as well.

Also, note the QQQ, SPY, TQQQ, SQQQ, ARKK and NVDL showed more signs of greed than fear.

The Bottom Line

There was no panic on Monday (nor should there have been). As a current bear and a contrarian, I would have liked to see panic. People are saying there was panic and are buying the market based on that. That scares the heck out of me. I’m going to stick with my argument that VIX futures and exchange-traded fund flows tell the real story – some fear, and a decent amount of greed.

At the time of publication, Tchir was long SQQQ and short QQQ.