Tensions Grow Globally, Earnings Pile Up, and What's Up With the Economy?

Let's look at fighting in the Middle East and Russia and the uncertain economic numbers as we brace for earnings from Google, Microsoft, Apple and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Very early Saturday morning, local time, Iranian media outlets started reporting explosions in the capital city of Tehran and nearby. It did not take long for the Israeli Defense Forces to confirm it made hits against Iranian air defense capabilities and missile and drone manufacturing facilities as well as other military targets. The attack was apparently carried out in three waves, over several hours. Nuclear and oil infrastructure-related areas were intentionally avoided in what was a limited response to Iran's failed large-scale attack on Israel almost four weeks ago that included the use of multiple ballistic missiles.

When all was said and done, the IDF confirmed that it had targeted 20 sites, claiming precise strikes, and Israeli Prime Minister Benjamin Netanyahu announced that Iran's defenses had been severely damaged. Iran, for its part, said that the Israeli attack had killed five individuals and not done much else. Iranian President Masoud Pezeshkian was quoted by the state-owned IRNA news agency, as saying, “We do not seek war, but we will defend the rights of the people and the nation, and we will give an appropriate response to the Zionist entity’s aggression.”

Is that it? Hope so. Does the war go back to where it was, a regional war fought mostly by Iranian proxies against the state of Israel? That depends on what happens from here. I would not let my guard down, though. These are dangerous times, and with Israel and Iran now hitting or trying to hit each other directly and with North Korean troops on Ukrainian soil, the times I refer to are now more dangerous than they were just a week or two ago.

What is probably the greatest threat to our lives and our treasure? I think it likely that the expansion of any of these wars beyond what areas they are now confined to is that threat. What might be worse would be the actual initiation of hostilities between mainland China and the island nation/province of Taiwan. What are the chances that any of these hot wars or smoldering tensions draws in the U.S. and with the U.S., American allies into a much larger conflict?

That's something I don't like to think of, though we must. That's why I hang on to most of my defense contractor type names, even in a time that calls for an elusive level of fiscal discipline. Even in the wake of Lockheed Martin's LMT lousy post-earnings weekly performance.

The Week That Was

Equity markets remained in the game last week, but for the most part gave up some ground, as gold continued its march toward what seems like a preordained date with the $2,800 per ounce level. As the U.S. Ten Year Note paid as much as 4.25% on Wednesday and even more than that last (Sunday) night. And as the VIX took back the 20 level for the first time in a couple of weeks. As a matter of fact, as the zero-dark hours pass, and European equity markets open in the green, U.S. Ten Year paper pays a rough 4.28%

The S&P 500 saw its six-week winning streak come to a screeching halt as the index posted four red daily candles in five sessions over the last full week of October. The Nasdaq Composite was able to post a small win for the week, but that was good enough to make for a seven-week winning streak for the home of big tech as we head into a new week. This new week that will be full of mega-cap, high-tech earnings releases. Small caps have been skating on thin ice for a while now. The Russell 2000 has posted six red candles over the past seven sessions and three losing weeks in the past four.

Tough Week for the Macro...

The Conference Board kicked things off on Monday with their once closely followed Index of Leading Indicators release for September. That release crossed the tape at -0.5% on a month-over-month basis. This data-point has now printed in a state of month-over-month contraction for seven consecutive months and has now incredibly printed in a state of month over month growth for precisely one of the past 30 months. Nice two and a half years. Not. Don't worry, the economy's fine. They said so on the news. Sell-side analysts even confirmed it. I feel better.

On Tuesday, the Richmond Fed Manufacturing Index printed at -14. That's 12-straight months with no growth or outright contraction in manufacturing from Richmond. Remember when Richmond was considered the second most important regional manufacturing survey in the country? They don't say that anymore? Wonder why.

September existing home sales hit the tape on Wednesday at a 14-year low. We're talking about the year 2010 now. Not a misprint. There was good news on Thursday when September new home orders actually beat the consensus view and showed growth from August. Huzzah.

Then came September durable goods orders. At the headline, durable goods printed down 0.8% from April, but up 0.4% from August not including transportation. That's positive. Core capital good orders printed up 0.5% from August. That's really positive. There is a but, though. Not including defense, durable goods order printed at -1.1% month over month for August. Hmm. That's kind of awful. How is business spending up 0.5% if ex-defense orders were down 1.1%. Don't ask me, I just work here. Not the first-time government data has left me scratching my head.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the third quarter down to growth of 3.3% (q/q, SAAR) from 3.4%. Among other central banks running close to real-time GDP models for the current quarter, the New York Fed revised its Q3 estimate down to 2.91% from 3.0%, remaining modestly less optimistic than Atlanta. The Cleveland Fed left its gross domestic product estimate at growth of 1.45%, while the St. Louis Fed took its estimate for the third quarter down just a smidgen to growth of 1.77% from 1.78%. We still have four Fed GDP models that for the third quarter are all telling us something very different. None of the four are that close to each other and estimates span almost 200-basis points from top to bottom.

Marketplace

As we approach election day with many having already voted, there is for the first time in over a month, some visible weakness in U.S. equities as higher yielding debt securities compete for investor dollars. This week brings with it Halloween and the end of October. Historically, November and December are positive months for U.S. equities. That's great, except that September usually is not. but was. October is usually volatile, and even last week, really was not. There's always these last four days.

Can we even think of market norms, when there is a national election being held or really completed (voting has already started) next Tuesday even if we don't know the outcome by then, and then the Federal Open Market Committee makes a policy decision next Thursday coming off a what you know I think was a "too aggressive" first step in their transition toward an easier monetary stance.

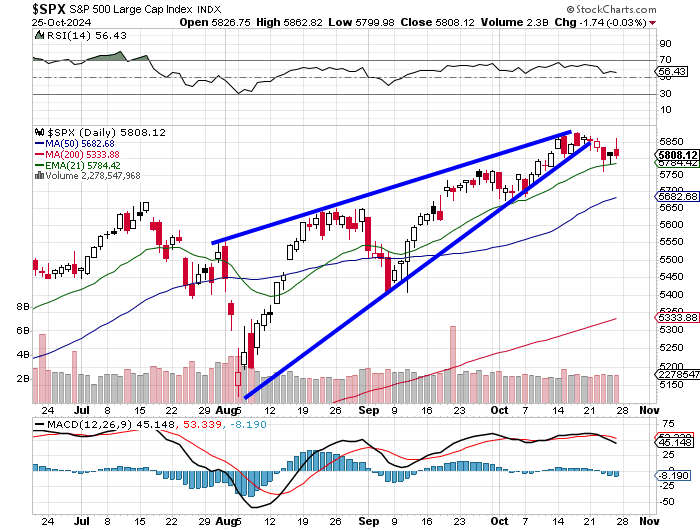

A week ago, I warned that the S&P 500 had developed a "rising wedge" pattern, which is a pattern of bearish reversal. We start to see that here. Just look at that daily moving average convergence divergence indicator? That's a bearish posture right there.

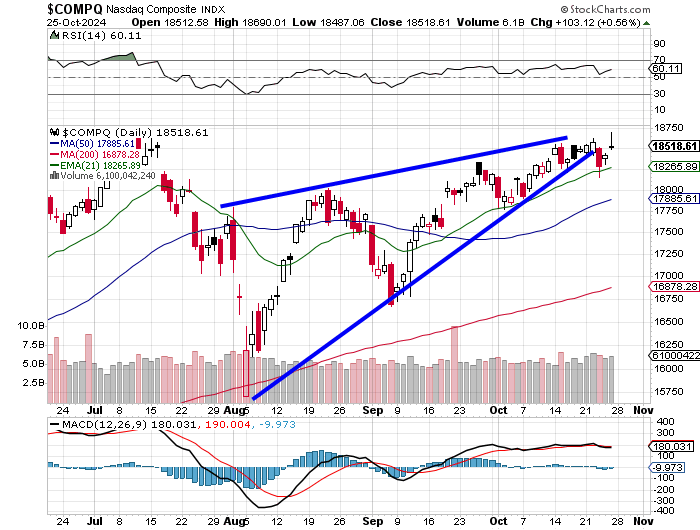

Then we see this. The Nasdaq Composite last week, rolled out of that closing wedge and looked like it was in trouble, until the "Mag 7" came to the rescue. All five members of the "Magnificent Seven" that will report this week, were up on Friday as the Nasdaq Composite made a new record intraday high.

As for the major to mid-major U.S. equity indexes last week:

- The S&P 500 gave up 0.03% (unch?) on Friday to close the week down 0.96%.

- The Nasdaq Composite gained 0.56% on Friday to close the week up 0.16%.

- The Nasdaq 100 gained 0.59% on Friday to close the week up just 0.14%.

- The Russell 2000 gave back 0.49% on Friday, to close the week down 2.99%.

- The S&P Small Cap 600 gave back 0.5% on Friday and closed the week down 3.1%.

- The S&P Mid Cap 400 gave up 0.65% on Friday, closing the week down 2.84%.

- The Dow Transports gained 0.17% on Friday but closed the week down 1.7%.

- The Philly Semiconductors gained 1.07% on Friday to close the week up just 0.08%.

- The KBW Bank Index gave up 1.37% on Friday, closing the week down 1.47%.

On Friday, just three of the eleven S&P sector SPDR exchange-traded funds closed in the green, with Technology XLK out in front at +0.52%. The Financials XLF and Utilities XLU both gave up more than 1% for the day.

For the week, just one of the 11 S&P sector SPDR ETFs closed in the green as the Consumer Discretionaries XLY were the only winner thanks to a 22% run by Tesla TSLA. The Materials XLB gave up a whopping 3.76% for the week, while three other sector funds gave up more than 2% and three more beyond that gave up more than 1%.

Earnings

According to FactSet, which as readers know, is my "go-to" for all things earnings-related, third quarter results perked up a bit last week. Right now, for the third quarter, S&P 500 earnings are showing blended (results & expectations) year-over-year growth of 3.6% up from 3.4% a week ago. That's still down from 4.2% three weeks ago, and down from 4.9% five weeks ago. Revenue growth is currently running at blended 4.9%, down from 5.1% three weeks ago.

Results and expectations for the third quarter are impacting the consensus view for both the fourth quarter and the full year. Fourth-quarter earnings growth is now seen at 13.4%, down from 14% last week and down from 14.6% the week prior, while full year earnings growth is now seen at 9.3%, down from 10.2% four weeks ago.

For the third quarter, double-digit earnings growth is now only expected from the technology and communication services sectors. Expectations for health care sector earnings growth have dropped from all the way from 11.1% to just 5.8%. The financials, industrials and energy sectors are all expected to post year-over-year earnings contraction, with close calls expected for both the staples and discretionaries. Energy earnings, by the way, are now seen as down an incredible 27.3% year over year.

The S&P 500 goes into this week trading at 21.7-times forward looking earnings, down from 21.9 times a week ago...which is well above the five- and ten-year averages for the index of 19.6 and 18.1 times, respectively. The S&P 500 also trades at 27.2 times trailing twelve months' earnings, down from 27.4 times a week ago...which is also well above the five- and ten-year averages of 23.9 times and 21.8 times.

The Week Ahead

Well, at least the Fed has gone into their media blackout ahead of the Nov. 7 policy decision. We won't have those folks speaking and getting in the way this week. Remember when we thought of Federal Reserve Board Governors as accomplished economists? Incredible how much that perception has changed.

This is going to be a busy week, gang. Both on the macro and on the earnings sides. As far as the macro is concerned, this is September jobs week. The Bureau of Labor Statistics will release the very likely to be highly inaccurate results of their two monthly labor market surveys this Friday and the algorithms that control price discovery in 2024 will act as if those numbers are gospel because the guys with the common sense that used to take things like that in stride have all been replaced by automation.

Wonder why we have been trained to accept daily price discovery overshoot in both directions? Simple, those traders who used to do that job were highly paid individuals who also received a yearly bonus. The algorithms will work tirelessly for free once up and running and provide more consistent profits for the market makers. Accurate price discovery is not the primary goal here. The guys who fix the algos when they break down are paid, but are also more easily replaced than those traders who kept their cool with the world on fire around them used to be.

Before we get to Jobs Day on Friday, we'll get our first look at Q3 GDP on Wednesday and September PCE Prices on Thursday. The ISM Manufacturing PMI for October will also hit the tape on Friday after the Employment Report is released.

Turning to corporate earnings, prepare to hear from five of the Mag 7 names this week. Alphabet GOOGL, Microsoft MSFT, Apple AAPL, Meta Platforms META and Amazon AMZN. Other high-profile names reporting will be Ford Motor F, McDonald's MCD, PayPal PYPL, SoFi Technologies SOFI, Advanced Micro Devices AMD, Chipotle Mexican Grill CMG, Eli Lilly LLY, Mastercard MA, Uber Technologies UBER and Exxon Mobil XOM.

What Else?

OK, so there were no major surprises that came out of last week's BRICS summit. That said, it remains clear that the group is growing and probably has its sights on re-setting the world economic order that to our benefit has relied upon the U.S. dollar as its leading reserve currency really since the end of World War II.

Aside from the now-nine full members of BRICS, an additional 26 nations sent delegations. There appears to be no current push to form a monetary bloc such as the Euro-Zone, but they did print up some ceremonial BRICS currency just to make sure that they sent a message.

No, the BRICS are not (yet) a military alliance either. What they are, are those nations that either feel left out, or think they can create an edge by forming a direction for international trade or in global affairs that does not rely on the US or NATO for leadership. We should be watching this develop over coming years much more closely than our leadership in DC appears to be. Hopefully, we are already gaming out various scenarios.

Economics (All Times Eastern)

10:30 - Dallas Fed Manufacturing Index (Oct): Expecting -1, Last -9.

3:00 p.m - US Treasury Refunding Estimates.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ON (0.97)

After the Close: F (0.48), WM (1.88)

At the time of publication, Guilfoyle was long LMT, XLU, AMZN, MSFT, MCD, SOFI, AMD, XOM. Short TSLA.