Stocks Pointed for the Sun. Then the Fed Pulled Them Back to Earth

The Fed now sees more economic activity, increased inflation and less unemployment than it had anticipated a mere three months ago. Here's what that means for the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Flight of Icarus

As the sun breaks, above the ground

An old man stands on the hill

As the ground warms, to the first rays of light

A birdsong shatters the still

His eyes are ablaze

See the madman in his gaze

Fly on your way, like an eagle

Fly as high as the sun

On your way, like an eagle

Fly and touch the sun

- Smith, Dickinson (Iron Maiden), 1983

The Ugly Stick Unleashed

We all know how the "Flight of Icarus" turns out. If I keep going, we will get to the lyrical line "Now his wings turn to ashes to ashes hid grave" and so it is. Did stocks get too high? Did risk assets reach for the sun? On Wednesday afternoon, the Federal Open Market Committee released both its policy statement and quarterly economic projections, and a few things became readily apparent. For one, the committee is no longer nearly as confident that it has won or is winning the battle with consumer-level inflation.

Like the wheatfield at Gettysburg, this is ground that the Fed expects to have to take and retake more than once. In short, the Fed sees 2024 ending on greater economic strength and with lower unemployment than expected just three months ago. Therefore, the committee cannot take short-term rates as low in 2025 as it had projected just three months later. Debt and equity markets were caught offside and thus forced to price in a new reality for not just 2025, but over the next few years and beyond as the economic projections show a group expectation for higher rates than had already been priced in going out indefinitely.

Yes, The FOMC Did Cut

In a move that had been anticipated by all, the Fed's FOMC reduced the target range for the overnight Fed Funds Rate by a quarter percentage point to 4.25% - 4.5%. This move took the Fed Funds Rate down 1 percentage point from where it had peaked (5.25% to 5.5%) for the post-pandemic era and had remained through this past September when the committee kicked off an ill-advised shift towards easier policy with a half percentage point cut.

As soon as Wednesday's policy statement and economic projections were released, equities sold off hard as did Treasury debt securities. This U.S. Dollar Index ran higher as gold, silver and Bitcoin moved toward its session lows. This is that story. The U.S. Dollar Index stood below 107 going into the event and moved above 108 overnight. The U.S. Ten Year Note paid 4.38% going into these releases and paid as much as 4.54% overnight.

The Meat & Potatoes

The deal is this. For year-end 2024 gross domestic product, the FOMC's median expectation moved up to growth of 2.5% from just 2% in September. While taking the group's expectations for economic growth significantly higher, the committee also revised its year-end median expectation for the unemployment lower to 4.2% from 4.4%, while nudging personal consumption expenditure inflation up to 2.4% from 2.3%, and core PCE up to 2.8% from 2.6%. These are things that we have been discussing for months. It appears that the Fed was the last to know, but that unfortunately the algorithms that now control the point of sale, had bought into the Fed's September story hook, line and sinker. Wall Street had humans making these decisions at one time and chose another route, so it is.

Bottom line? The Fed now sees more economic activity, increased inflation and less unemployment than it -- as a group -- had anticipated a mere three months ago. After considering all of this, the committee left its year-end projection for the fed funds rate at 4.4%, which is where it had been in February. This is where the committee essentially took that target range (4.25% to 4.5%) for that rate today.

That's not what hurt our marketplace. What did slap financial markets around on Wednesday afternoon was the FOMC's median projection for the fed funds rate at year's end 2025, 12 months from now. The FOMC took that median expectation up to 3.9% from 3.4%. To dumb it down, the FOMC cut its full-year 2025 projection from four quarter-point rate cuts down to just two quarter-point rate cuts.

As the FOMC was revising its 2025 interest rate projections higher, it also took its median projections for 2025 PCE (consumer level inflation) higher ... from 2.1% to 2.5% at the headline level and from 2.2% to 2.5% at the core. Unemployment for 2025 was taken slightly lower while GDP for 2025 was taken slightly higher. It became clear to traders, investors and algorithms alike that the Fed is no longer confident that the central bank can continue to ignore the inflation side of its dual mandate for very long. It has finally acknowledged that inflation has accelerated again into the final months of 2024.

To make matters worse for net long equity and risk asset investors, the FOMC also took the committee's median projections for the fed funds rate at year's end for 2026, 2027 and for the longer run higher. This implies that at no time in the future will the perceived loss of those two rate cuts next year be made up down the road.

Just an FYI

The Cleveland Fed's model projects December headline consumer price index up at year-over-year growth of 2.86%. Readers may recall that actual CPI for November printed at growth of 2.7%, after October printed at 2.6% and September printed at 2.4%. My trusted source, Hedgeye Risk Management shows a base case for December CPI at 2.94%, with a possibility for a 3 handle.

Fed Funds Futures

This morning, Fed Funds Futures trading in Chicago are no longer pricing in a rate cut in March and another rate cut later in the year, despite that the FOMC is still projecting two rate cuts in 2025. This market is now pricing in just one rate cut of a quarter-percentage point for all of 2025 in May. That would take the range for a potential terminal rate for this period of panic stricken and probably ill-advised policy easing down to 4% - 4.25%. The probability for a second rate cut of a quarter-percentage point at any point in 2025 has dropped to 44%. In fact, according to this market there is now a 19% likelihood that there will be no rate cuts at all in 2025.

Equities

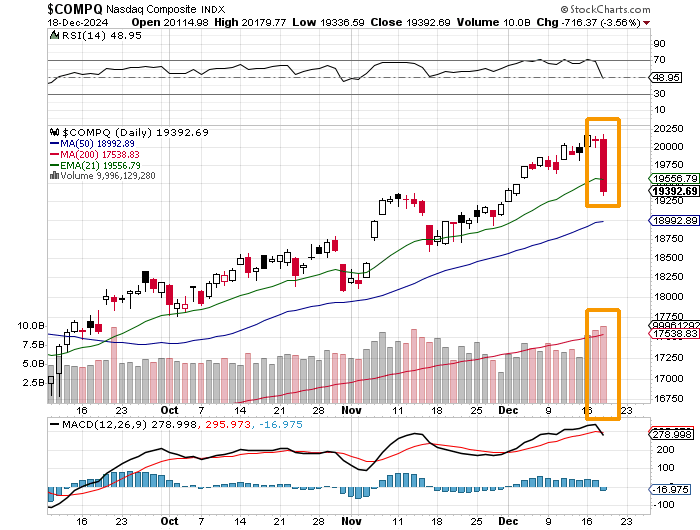

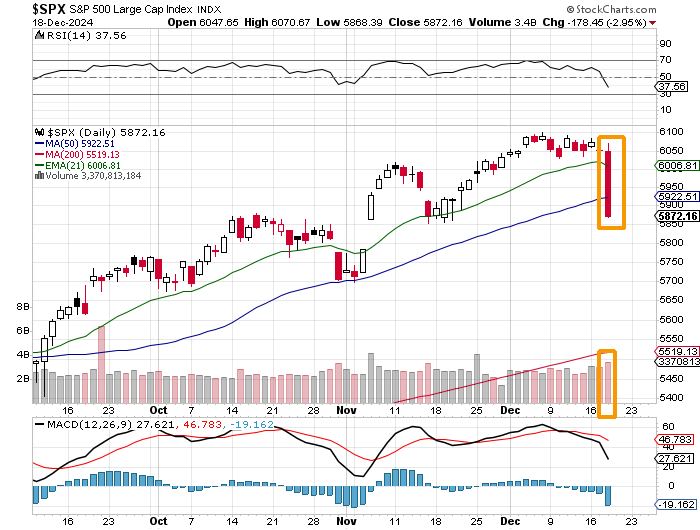

To think almost all of the damage was done in less than two hours. On Wednesday, the S&P 500 gave back 2.95%, as the Nasdaq Composite surrendered 3.56%. The small caps were hit hardest as the Russell 2000 lost 4.39%, as the Dow Industrials proved to be the day's top performer at -2.58%. Despite being the least severely beaten index on Wednesday, the Dow Jones Industrial Average posted a tenth consecutive red candle session, which is its worst run since an eleven-day losing streak in 1974. The KBW Banks also had a private meeting with the "Ugly Stick," giving up 4.28% as the Fed shooed away the idea of suppressing short-term rates. This would have provided for the banks, an environment ripe for improved net margins as long as the central bank did not go as far as actually buying longer-term U.S. paper.

All 11 S&P sector SPDR exchange-traded funds closed sharply lower on Wednesday, led by the Consumer Discretionaries XLY at -4.51%. Three of these funds gave up more than 3% and nine of these funds gave up more than 2%. Only the defensive Health Care XLV and Staples XLP sectors managed to lose less than 2% for the day. Both lost more than 1%.

Breadth was, as expected, awful. Losers beat winners by a 13-to-1 margin at the NYSE and by a rough 11 to 2 at the Nasdaq. Advancing volume took just a 10.7% share of composite NYSE-listed trade, as aggregate volume for names domiciled at 11 Wall Street popped 15.5% higher on a day over day basis. Advancing volume took a 38.9% share of composite Nasdaq-listed activity on aggregate volume for names domiciled up at Times Square that increased 4.9% day over day.

That, my friends, is meaningful. The sharp move on elevated trading volume means that there was conviction in the move and that professional money moved out of equities.

Readers will see that above what is really a two-day sell-off on increased trading volume. This whole two-day period counts as a Day One of any potential change of trend to the downside. Both the Relative Strength Index and the daily Moving Average Convergence Divergence indicator for the Nasdaq Composite have clearly re-postured themselves more bearishly. In order to confirm the shift, keep in mind that we need to see a relief rally of sorts that puts some space between this initial move and the next shoe that drops. Should there be a continuation of the sell-off today that would only be seen as more of the same move. There has to be a break, and then another sell-off on convincing volume. This would give the appearance of more thought, and less emotion involved in any next risk-off day.

Readers will also see a Day One set-up for the S&P 500, with the exception that the selling on increased trading volume all happened in one session. For the S&P 500, both the RSI and the daily MACD are also bearish. The difference here, and quite possibly a mark against the S&P 500 that is not yet true for the Nasdaq Composite is the fact that the S&P 500 surrendered its 50-day SMA on Wednesday without a fight. The Nasdaq Composite can still try to hold that line. The entire equity market closed near its lows for the regular session.

What Else?

- The CDC reported on Wednesday that a patient in Louisiana had been hospitalized with a severe case of the Avian (H5N1) Bird Flu. This is the first known instance of severe bird flu illness in the U.S. This is not the same strain that had been detected in wild birds, poultry, dairy cows and some humans in other states.

- Micron Technology MU gave up more than 4% during Wednesday's regular session and then another 14% or so after the closing bell as the firm released earnings that met expectations, but guidance that certainly did not.

- Did some light buying late Wednesday. Added to existing long positions in SoFi Technologies SOFI, SentinelOne S, Palantir Technologies PLTR and Dell Technologies DELL on weakness.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 240K, Last 242K.

08:30 - Continuing Claims (Weekly): Last 1.886M.

08:30 - GDP Growth Rate (Q3-Final): Flashed 2.8% q/q, SAAR.

08:30 - Philadelphia Fed Manufacturing Index (Dec): Expecting 2.2, Last -5.5%.

10:00 - Existing Home Sales (Nov): Expecting 4.03M, Last 3.96M, SAAR.

10:00 - CB Leading Indicators (Nov): Expecting -0.1% m/m, Last -0.4% m/m.

10:30 - Natural Gas Inventories (Weekly): Last -190 Bcf.

11:00 - Kansas City Manufacturing Index (Weekly): Expecting 4, Last -4.

16:00 - Net Long-Term TIC Flows (Oct): Last $216.1B.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ACN (3.42), KMX (.60), CTAS (1.01), CAG (.68), DRI (2.02), FDS (4.28), LW (1.03), PAYX (1.12)

After the Close: FDX (3.95), NKE (.64)

At the time of publication, Guilfoyle was long SOFI, S, PLTR, DELL equity.