Stocks Look Hot but Index Charts Do Not

We're seeing green right now, but I'm still cautious on the near-term outlook for several reasons.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Futures looked strong this morning and now 90 minutes or so after the opening bell, stocks are climbing.

I'm still cautious, however, on the near-term outlook, as the index charts remain bearish and the data is flashing yellow lights.

Let me explain, but let's first check the stats:

The major equity indexes closed mixed yesterday with positive internals on the New York Stock Exchange and Nasdaq, as NYSE volumes rose and Nasdaq volumes dipped from the prior session. Most closed near their midpoints of the day that saw two of the indexes close below support, leaving most of the charts in bearish near-term trends as rotation from the mega-caps to mid-caps continued. Cumulative market breadth remains bearish, as well.

Checking Under the Hood

The McClellan one-day overbought/oversold oscillators remain neutral (All Exchange: 4.45; NYSE: -2.66; Nasdaq: 10.71), lacking oversold readings, while investor sentiment data and valuation continue to be disconcerting. The overbought/oversold oscillators, to be clear, are not oversold

On the charts, the major equity indexes closed mixed yesterday with positive internals with most closing near their session midpoints.

Importantly, the Nasdaq Composite and Nasdaq 100 closed below support and remain bearish as are the S&P 500 and Dow Jones Transports.

The Dow is the only bullish chart with the mid-caps and Russell 2000 small caps, neutral.

The action suggests the rotation form mega-cap stocks to small- and mid-caps remains active.

The positive internals were insufficient to alter the current bearish trends for the cumulative advance/decline lines for the All Exchange, NYSE and Nasdaq.

Some stochastic levels are now oversold but bullish crossover signals have yet to appear.

Meanwhile, the percentage of S&P 500 issues trading above their 50-day moving averages, a contrarian indicator, rose to 61% and also neutral.

But the "detrended" Rydex Ratio (also a contrarian indicator) remains bearish, rising to 1.05, as the typically wrong leveraged exchange-traded fund traders remain overexposed and leveraged long. We still need to see some fear on their part.

That leaves all three of the sentiment indicators bearish as the “herd” is all on the band wagon.

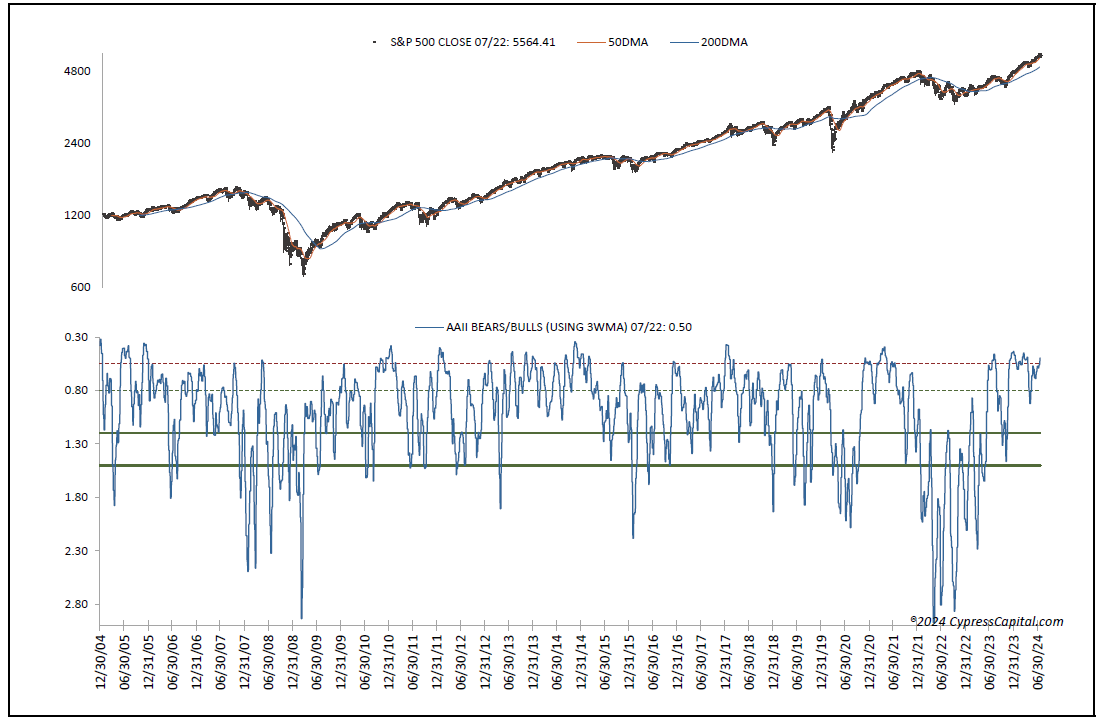

This week’s American Association of Individual Investors Bear/Bull Ratio (contrarian indicator page 8) turned bearish at 0.50 as the Investors Intelligence Bear/Bull Ratio (another contrary indicator) stayed bearish at 16.7/63.6, as bulls continued to outweigh bears by a wide margin. There is no “wall of worry” to climb.

The Open Insider Buy/Sell Ratio is neutral at 29.5. Leveraged ETF sentiment is 0.2 and neutral.

Valuation Concerns

Valuation remains a concern. The 12-month consensus earnings estimate for the S&P 500 from Bloomberg rose to $252.42. But that leaves its forward price-to-earnings of 21.4 still well above the “rule of 20” ballpark fair value at 15.7. Its almost 600-basis point premium remains significant.

Its earnings yield rose to 4.68%.

The 10-year Treasury yield slipped to 4.26. Support is 4.21% and resistance at 4.3%. Its near-term trend is bearish.

The U.S. Dollar, via the Invesco DB US Dollar Index Bullish Fund UUP, closed flat at $28.84. Its trend is neutral with support at $28.70 and resistance at $28.87.

Bottom Line

All the data we're seeing is still sending warning signals. We do not see enough evidence to suggest a shift in our current cautious macro-outlook for equities that remains cautious. Continue to honor sell signals on individual names while staying very selective on the buy side.