After Breaking Near-50-Year Record, the Market Is All About Rotation

There's a big question about what the shift to small caps might mean for mega names and money on the sidelines.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

After the assassination attempt on the former president and with the upcoming Republican National Convention, there is a lot of talk about the “Trump Trade” — stocks as a whole do well, some sectors excel, crypto does great and bonds, especially the long end, struggle.

The real story is much simpler and started last week: The Fed will cut in September at the latest and 75 bps of cuts for this year seem highly likely. Signs of life appeared in small caps, both on Thursday and Friday.

But what is less clear is if the shift to small caps will come at the expense of mega caps (investors selling one group of stocks to buy another group) or the much anticipated “money on the sidelines” (investors moving money out of money market funds and into stocks).

Earnings will certainly play a role as well.

Yes, I think about the election and potential implications, but for now, it is a second or third order effect. We don’t know for certain who is running — Donald Trump seems like a certainty, but questions on Joe Biden remain. We don’t know vice presidential candidates yet, which may be important. We are in “campaign promise” mode, where I think it is difficult (and usually wrong) to extrapolate promises into actions. And I continue to see no evidence of fiscal restraint from either side, and expect that to weigh on bonds over time.

So, I’m leaving “election” trading in the background for now. Back to the rotation.

Thursday was an incredibly unusual day. Not only was the outperformance of the Russell 2000 versus the S&P 500 quite high, it is extremely rare (once in 45 years, prior to Thursday) for the Russell 2000 to be up 3% or more, while the S&P closed down — and that was in October 2008. October 2008 was a time of confusion and heightened volatility. Thursday started more or less with “normal” reactions to a good CPI print.

Thursday had all the makings of a “rotation” where there was selling of one type of stock to make room for another group.

Friday seemed like “money on the sidelines” as all stock indices did well, but that faded, quite aggressively, for the Nasdaq 100, into the close.

We start seeing a divergence shortly after the “official” launch of ChatGPT and “generative AI capabilities” in early 2023 (a version was released in November 2022, but it didn’t seem to resonate as much then).

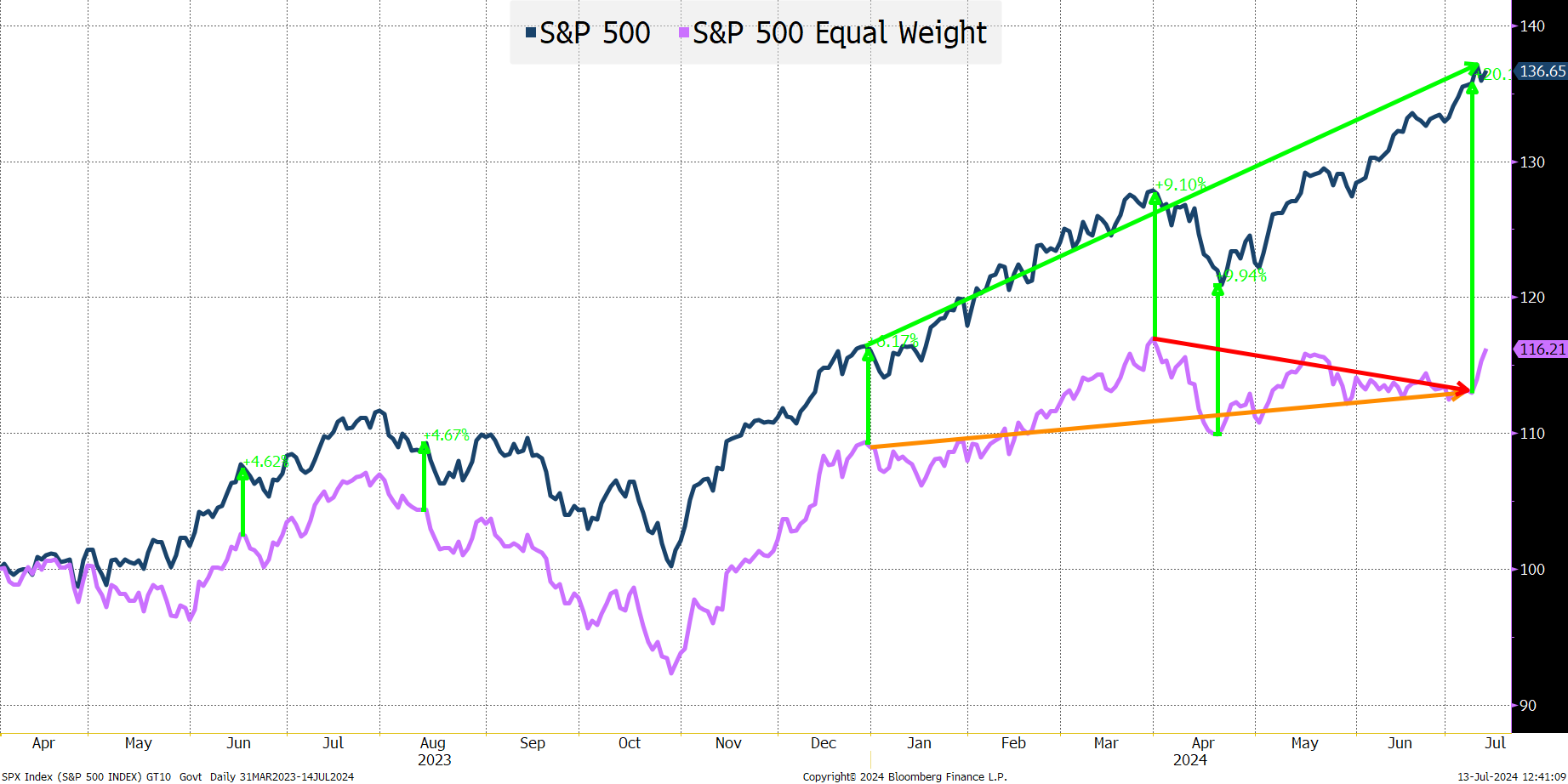

Possibly another factor is that the second-to-last rate hike occurred in May 2023, with the last cut in July 2023. The divergence, though, stayed relatively stable until this year. From the middle of 2023 until the start of this year, it was somewhat “stable” at around 6%. Yes, we had an initial deviation, but it grew gradually. That is not the case now. It went to 9% by the end of March and stood at a whopping 20% as of Wednesday. The equal weight index is actually down from March 27, 2024.

The same stocks create 17.7% year to date when using market weights, and only 6.7% when using an equal weight.

The top-12 companies (13 holdings) currently account for almost 40% of the market cap index. Those stocks are up an average of 42%. The average return of the other 490 or so companies is 5%. The average return, year to date, of the smallest 250 companies in the S&P 500 is 0%.

Bottom Line

I still like energy-related stocks and commodities (primarily as geopolitical risk hedge).

I fear that much of the trading late last week had the hallmark of “quant fund” selling. We have seen time and again in these markets the ability of quants to overrun liquidity.

Base case is outperformance of small caps, value, anyone ‘left behind” but in a down market, one fraught with the risk of a sizable one day move!

In terms of lack of breadth, beware what you ask for, as getting an expansion of breadth may come with far more costs than the “money on the sidelines” crowd bargained for.

At the time of publication, Tchir had no positions in any securities mentioned.