So, Which One Is It, Powell?

If the Fed is cutting rates by half a percentage point, then why is Powell so strangely saying the job market is 'solid'? Also, the market, banks and Dimon's warnings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The Federal Reserve Bank's FOMC kicked off its easier monetary policy trajectory on Wednesday with an aggressive, but somewhat priced, half-percentage-point cut to its target range for the Fed Funds Rate. The benchmark rate now stands at 4.75% to 5%. At the median, in the Federal Open Market Committee's economic projections, the group signaled it would slice another half-percentage point off the rate over the final two policy meetings of 2024.

The aggressive first move, however, did not take traders completely by surprise. Futures markets had been prepared for such a rate reduction. What did take traders by surprise, was the bizarre press conference where Fed Chair Jerome Powell said that while unemployment is now the focus, "This is still a solid labor market." He referred to the economy in general as healthy, while stating that he still expected consumer-level inflation to reach the Fed's 2% target.

If Not for Economic Reasons, Then Why?

Why this is a bit on the unusual side, is that such large rate cuts, especially when coupled with such dovish signaling, is usually reserved for dire circumstances that could act as a catalyst for economic contraction. While I have been outspoken in providing my thoughts that the economy was weaker than is implied by gross domestic product data and have pointed at gross domestic income data that has been much weaker than GDP, GDI is still not in contraction.

Powell failed to answer adequately a question by Mike McKee of Bloomberg on whether the Fed was no longer data-dependent, but now proactive, or pre-emptive. Powell kept saying that the changes in policy and trajectory were not in response to failing economic conditions, but rather to "recalibrate" policy. Powell used the term "recalibrate" multiple times. He did not seem himself.

Quite understandably, after uncharacteristically being unable to provide economic reasons for taking such aggressive action, Powell and his crew faced multiple accusations overnight of acting for other than economic purposes -- even that it was for political purposes. I covered the events late Wednesday afternoon here at TheStreet Pro in close to real-time. While we search for answers, there remains the possibility that Powell sees the economy as weaker than he let on, or that it's about to weaken more quickly than he let on. That at least would better explain the actions taken. Regardless, we are amphibious. Any environment. We thrive.

Markets Gone Wild

Financial markets gyrated on Wednesday afternoon, at first appearing to celebrate the decision, then reversing quite negatively into the closing bell. Markets have now reversed yet again overnight. It seems that markets have embraced the change in direction.

Remember, as I have told you above and have inferred many times, our mission is not to decide policy. We may like it or not. I personally did see reason for a large rate cut, when a smaller one, coupled with less dovish signaling would have sufficed, but I also see the economy and labor markets as weaker than Powell admits to. I can explain why I would do, as a policy maker, what I would do. Powell in short, seemed to say, everything is better than OK, so we're going to aggressively cut rates. Powell in short, seemed to say, "Everything is better than OK, so we're going to aggressively cut rates."

Powell in short, seemed to say, 'Everything is better than OK, so we're going to aggressively cut rates.'

Always maintain focus ... our job is to adapt to any environment and seek victory. That, my friends, is what we are good at and what we are going to do. Overnight, the U.S. Dollar Index has been all over the place, trading as high as 101.38 and now trading down around 100.62. This is in response to the expectation, or realization, that the Fed is easing policy (yes, while carrying on with its quantitative tightening program), and the dollar will weaken as either a result or perhaps the intended target of such policy.

Keep in mind that the Federal government has been wasting money on debt service to a horrific degree as deficit spending exploded during and especially after the pandemic and has not let up into the present. The Fed may have no choice but to reduce borrowing costs for the overly indebted U.S. government and may have to ultimately monetize that debt. That would be highly inflationary and disastrous for savers and those living on fixed incomes. Gold futures have reclaimed their near all-time high levels reached earlier this week. Bitcoin is also up nicely overnight and is up quite sharply over the past two weeks.

U.S. equity index futures are also up sharply overnight, as yields at the short end of the Treasury curve came in on high demand and the longer end of that curve sold off, experiencing a possibly counterintuitive rise in yields. Such an expansion in Treasury yield spreads might not be very counterintuitive at all if the Fed is to artificially suppress short-term rates, and longer-term rates are permitted to be priced by the free market as free market forces will respond to over-indebtedness and a renewed acceleration of inflation.

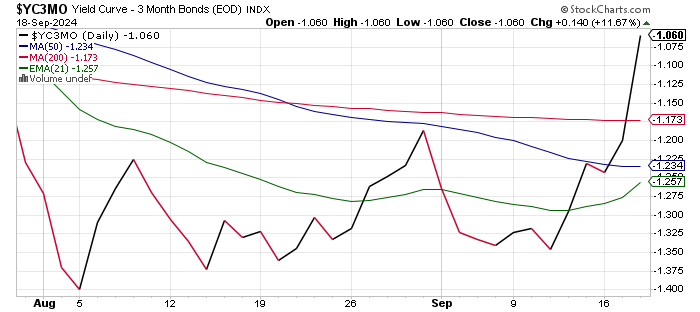

Just take a look at the spread between the yields of the U.S. Three-Month T-Bill and U.S. Ten Year Note. This spread, though still quite inverted, steepened a great deal on Wednesday and over the past week ahead of the FOMC decision. I remain long the SPDR Gold Shares GLD, the iShares Silver Trust SLV, and the Goldman Sachs Physical Gold fund AAAU, as well as physical gold itself.

Temporary Boost for Banks?

Don't be surprised if these conditions actually improve things like net interest margin for the banks for at least a little while. Several of the big banks have recently warned on net interest margin as the long end of the yield curve has come in. Now, with the central bank pressuring the short end of that curve, the environment could and should at least temporarily improve. I remain long SoFi Technologies SOFI and Wells Fargo WFC.

Interestingly...

DoubleLine CEO Jeffrey Gundlach, who I see as a smart fellow, and enjoy listening to, appeared on CNBC late Wednesday afternoon. Gundlach was not surprised by the large cut, in fact, in an appearance earlier this week, he referred to the Fed as being "behind the curve." He sees the action in Treasury markets and the fact that he believes the US economy may already be in recession as reasons for the FOMC's aggressiveness.

For those unaware, the US Two Year Note pays 3.59% this morning after having paid as much as 4.76% on July 1st and more than 5% this past Spring. During last night's interview, Gundlach said, "The level of debt on the consumer is very high. I expect to see weaker economic data in coming reports. I still think there's a good shot that the history books will say September '24 was a start of a recession."

That would be a far better explanation than what Powell provided.

Bear in Mind Dimon's Words

This past Tuesday, JP Morgan Chase JPM CEO Jamie Dimon spoke in Brooklyn. Dimon said then that the U.S. economy is not "out of the woods" adding "I would say the worst outcome is stagflation -- recession, higher inflation... and by the way, I wouldn't take it off the table."

A day later, at the 2024 Financial Markets Quality Conference in Washington, Dimon stated, "The most important thing that dwarfs all other things, that's really far more important today than it's been probably since 1945 is the war in Ukraine, what's going on in Israel, in the Middle East, America's relations with China and the attack fundamentally on the rule of law that was set up after World War II."

Dimon added, "It's ratcheting up folks and it takes really strong American leadership and Western world leadership to do something about it. That's my number one concern." Hence, I remain long Lockheed Martin LMT, Northrop Grumman NOC, General Dynamics GD and of course, Palantir Technologies PLTR.

Economics (All Times Eastern)

08:30 a.m. - Initial Jobless Claims (Weekly): Expecting 230K, Last 230K.

08:30 - Continuing Claims (Weekly): Last 1.85M.

08:30 - Philadelphia Fed Manufacturing Index (Sep): Expecting 1.2, Last -7.0.

10:00 - Existing Home Sales (Aug): Expecting 3.88M, Last 3.95M SAAR.

10:00 - CB Leading Indicators (Aug): Expecting -0.3% m/m, Last -0.6% m/m.

10:30 - Natural Gas Inventories (Weekly): Last +40B cf.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: DRI (1.84), FDS (3.62)

After the Close: FDX (4.85), LEN (3.62)

At the time of publication, Guilfoyle was long SOFI, WFC, LMT, NOC, GD, PLTR, GLD, SLV, AAAU.