Sellers' Ambush, Inversion Reversal? Trading Microsoft, ServiceNow and Gold

The on-again, off-again rotation was back on late Thursday. Here's what I was trading. Plus, GDP vs. GDI, Friday's economic data and much more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I ever tell you my jaguar story? No? It's not like my black bear story or my lemon shark story. There was actual contact when I met up with those characters. It's not like my twin albino deer or wolfpack stories. Those were semi-mystical.

There's really not that much to it at all. I saw a jaguar, not a car, in the wild once. I was the rear guard for an ambush out in the jungle when I was a kid. It was either late or early. I no longer remember. We had set up an ambush along a slightly worn trail for some folks who never showed up. The jungle was dark, but not completely dark. It was kind of gray beneath the canopy.

The rear guard for ambush is a two-person job. The other guy was sick. I was senior. I sent him off to find our corpsman (medic). I was alone. So, I thought. Something leapt 30 or 40 feet in front of me then moved in a few feet. I had been silent and stationary for some time now. It was a cat. It was more than a cat; it was a jaguar.

I could not believe my eyes. I would have thought that it would have picked up my scent, but I guess I was pretty grungy. In the jungle one never wears deodorant or anything like that and one rubs jungle mud on their exposed skin in order to smell like jungle rot and crust the skin against insects. Guess I did a decent job.

Except, I must have moved after I saw the cat, because the cat saw me almost as soon as I saw it. Startled, it ran away from me. Thank goodness. Just as startled, I moved my post several feet back towards our main body as I was a corporal, and I did not want my sergeants to know I had let the other kid see a medic on my own authority. Nothing happened. Just one of those things that stays in the back of one's mind for a lifetime. Beautifully athletic animal.

Stocks sold off fairly hard shortly after the opening bell on Thursday morning. Then, we all went for a ride. For about two hours, it was "risk-on" in response to Wednesday's nearly day-long selloff. Just one thing. The buyers ran out of gas with about half an hour to go. The sellers were waiting in ambush... and ambush is what they did.

Marketplace

The on-again, off-again rotation was back on, during that furious ending to the regular session. Oh, the smaller-caps sold off into the bell too, just not nearly as severely. They also managed to stay green.

While the S&P 500 closed down 0.51% and in the red for a sixth day in seven, the Nasdaq 100 gave up 1.06% and did the same. The winners? The S&P SmallCap 600 rose 1.26% for the session, while the Russell 2000 and the Dow Transports each advanced 1.39%. The small-cap indexes have now gone green for three of the past four trading days.

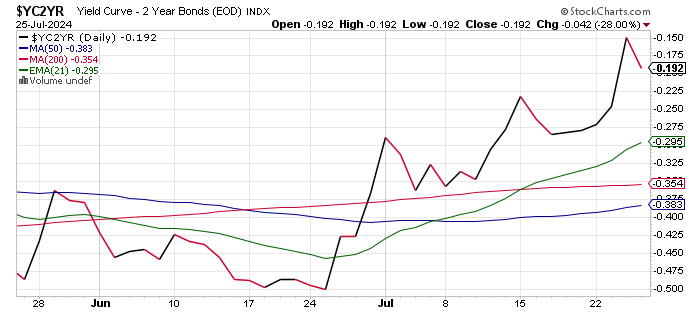

Interestingly, as equities moved in erratic fashion on Thursday, so did Treasury debt securities. The 10-Year/2-Year inverted yield spread that has been hastily speeding towards un-inverting, reversed slightly on Thursday. Alongside a strong auction for $44 billion worth of 7-Year paper, the yield for the 10-Year Note moved four basis points lower to 4.25%, while the yield for the 2-Year Note backed up two basis points to 4.43%. That spread over the past two months looks like this:

Is the surge towards reversing an inversion an economic growth story? It could be. On Thursday, June Durable Goods Order printed in deep month-over-month contraction at -6.6% for the headline print. That was versus expectations for +0.3%. The thing is, in economics, the headline print for durable goods is not as important as is the print for Core Capital Goods Orders, which omits defense and transportation orders that tend to be large and come in chunks. This line item is considered a proxy for business investment. Well, for June, Core Capital Goods Orders printed at +1% m/m versus expectations for +0.2% and makes for a nice rebound off of a revised -0.9% print for May.

On GDP

The Bureau of Economic Analysis released their first estimate (of three) for Q2 GDP on Thursday morning. The print hit the tape at growth of 2.8% (q/q, SAAR) with Wall Street expectations for 2% and most of the regional Fed districts looking for less. The Atlanta Fed, to its credit, if this number holds, went out looking for a 2.6% print. That would make Atlanta the most accurate amongst its peers for the past quarter.

Within the print, there was a rebound in both personal consumption expenditures and inventory building. Personal consumption accounted for 157 basis points of the whole (which was really +2.84%), up from 98, while inventory building accounted for 82 basis points up from -42. Government added 53 basis points up from 31, while net imports/exports subtracted 72 basis points, down from subtracting 68 basis points for the first quarter.

Readers should keep in mind that the BEA does not release its estimate for GDI with its advance estimate for GDP, so there is no check on this number at this time. As we all should know by now, GDI and GDP should in theory, come to the same pace of growth for any period of time. When they are not close, at least one of them is in error, and the Fed suggests averaging the two when discussing economic growth. We all know that this is not what the financial media did in 2023 when real GDP showed growth of 2.5% and real GDI showed growth of only 0.4%. Bottom line: Trust nobody discussing economic growth that does not understand GDI or at least mention it in the conversation.

By the way, our friends at Hedgeye were ahead of Wall Street and yours truly on this Q2 GDP acceleration. Four days ago, Hedgeye's Josh Steiner sent out a memo explaining that second-quarter GDP would likely surprise to the upside. Not bad, huh? Yes, instead of hiring a staff to meet my macroeconomic research needs, I outsource that workload, which is quite intensive.

Later On...

I would not expect as much of a market reaction this morning to the BEA's release of June Personal Income and Spending along with June PCE and Core PCE inflation. These numbers coming as late in the following month as they come are far less likely to surprise as the monthly print for CPI sometimes can.

There may, however, be a real reaction to the University of Michigan's revision to their July Consumer Sentiment survey, especially if the one-year-out print for inflation expectations moves one way or the other.

Trading

On Thursday, I made the following trades:

I added to my Microsoft MSFT long at the lower bound of an 18-month-long ascending price channel as that channel was tested.

I sold the tranche of ServiceNow NOW that I had added on Wednesday evening (making a quick $109 per share), returning that position to its intended core size.

I initiated a long position in the Goldman Sachs Physical Gold ETF AAAU to complement my existing long position in the SPDR Gold Shares GLD. I remain long actual physical gold as well. A nod to Keith McCullough, CEO of Hedgeye, for the assist on that one as well.

Economics (All Times Eastern)

08:30 - Personal Income (June): Expecting 0.4% m/m, Last 0.5% m/m.

08:30 - Consumer Spending (June): Expecting 0.3% m/m, Last 0.2% m/m.

08:30 - PCE Price Index (June): Expecting 0.1% m/m, Last 0.0% m/m.

08:30 - Core PCE Price Index (June): Expecting 0.2% m/m, Last 0.1% m/m.

08:30 - PCE Price Index (June): Expecting 2.5% y/y, Last 2.6% y/y.

08:30 - Core PCE Price Index (June): Expecting 2.5% y/y, Last 2.6% y/y.

10:00 - U of M Consumer Sentiment (July-F): Flashed 66.0.

10:00 - U of M Consumer One Year Inflation Expectations (July-F): Flashed 2.9%.

10:00 - U of M Consumer Five Year Inflation Expectations (July-F): Flashed 2.9%.

13:00 - Baker Hughes Total Rig Count (Weekly): Last 586.

13:00 - Baker Hughes Oil Rig Count (Weekly): Last 477.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: MMM (1.68), BAH (1.52), CL (.87), BMY (1.64)

At the time of publictaion, Guilfoyle was long MSFT, NOW, GLD and AAAU.