Doug Kass: Sell American, Warren Buffett Is

In the middle of The Great Financial Crisis, Warren Buffett wrote a New York Times column, 'Buy American, I Am.' Guess what he's doing now?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In 2008, amid The Great Financial Crisis, Warren Buffett famously wrote an editorial in the New York Times, entitled, "Buy American, I Am."

It began:

THE financial world is a mess, both in the United States and abroad. Its problems, moreover, have been leaking into the general economy, and the leaks are now turning into a gusher. In the near term, unemployment will rise, business activity will falter and headlines will continue to be scary.

So ... I’ve been buying American stocks. This is my personal account I’m talking about, in which I previously owned nothing but United States government bonds. (This description leaves aside my Berkshire Hathaway holdings, which are all committed to philanthropy.) If prices keep looking attractive, my non-Berkshire net worth will soon be 100 percent in United States equities.

Why?

A simple rule dictates my buying: Be fearful when others are greedy, and be greedy when others are fearful. And most certainly, fear is now widespread, gripping even seasoned investors. To be sure, investors are right to be wary of highly leveraged entities or businesses in weak competitive positions. But fears regarding the long-term prosperity of the nation’s many sound companies make no sense. These businesses will indeed suffer earnings hiccups, as they always have. But most major companies will be setting new profit records 5, 10 and 20 years from now.

I encourage you to read the entire column, but he essentially explains in the piece why he was being greedy in buying stocks on the cheap, while others were being fearful by aggressively selling stocks at the lows.

Buffett's column and multiple purchases of stocks in 2008 were not perfectly timed. They occurred about six months before the S&P 500 bottomed at 666 in the early days of March 2009. But, in the fullness of time, those stock purchases and his upbeat market view near the low in the S&P 500 index proved to be profitable and materially on target over the next 15 years.

Today, nearly 16 years later, Warren Buffett is making more news -- but now he is selling.

Over the last several months Berkshire Hathaway has substantially trimmed his Apple AAPL holdings by nearly half. He is already incurring a meaningful tax liability on an estimated $50 billion of capital gains.

Moreover, he is also now reducing his Bank of America BAC long (thus far by about 15%). On that, he is incurring a tax liability on between $5 billion -$6 billion of capital gains.

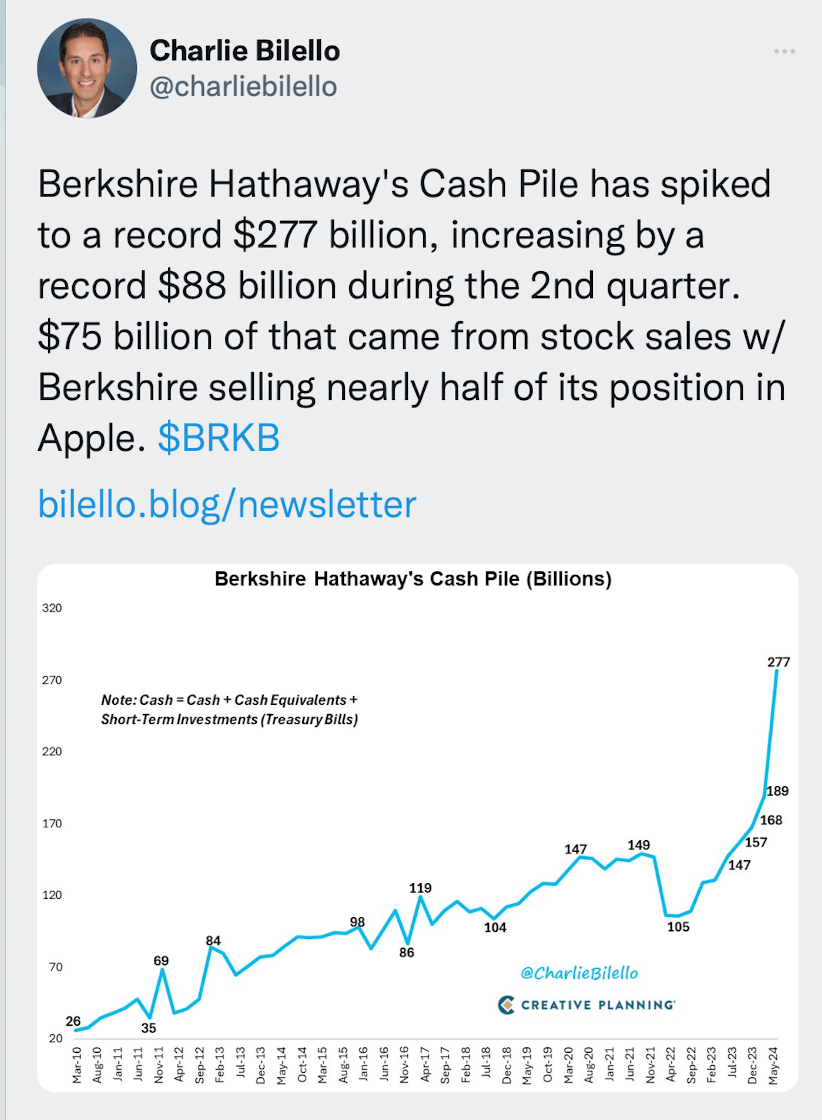

Selling "forever" holdings like Apple and BofA are not Buffett-esque. We know from previous comments that Warren Buffett hates paying taxes unnecessarily. Also, while they had grown to a disproportionately large percentage of Berkshire's investment portfolio and total equity/assets, his recent and accelerated sale of nearly half of this "forever" position in Apple during the second quarter seems to be a more important statement -- and at the polar opposite of his market view when he was buying equities 16 years ago. Moreover the continued sizeable and steady sale of shares in his long standing investment in Bank of America over the last quarter raises even more questions about The Oracle's view of the global economy and our capital markets. Furthermore, Berkshire Hathaway has now accumulated a record cash hoard that is close to $300 billion, as Buffett's favorite market indicator (Wilshire market cap to GDP) is flashing a strong sell signal.

According to the company's 2021 Annual Report (the last time individual securities cost basis were presented), Berkshire Hathaway's cost basis on his then-holdings of 907 million shares of Apple was about $34/share compared to a current share price of $225/share. Berkshire's cost basis on his position of 1.03 billion shares of BofA was about $14/share compared to the current price of $41/share.

We can fully comprehend Warren's decision to pare back an extraordinarily successful investment in Apple that, thus far, has reaped in excess of $60 billion in profits. A partial sale could have been expected and would have been a conservative and understandable decision, even though it would result in a large but manageable tax liability.

But the sale of nearly half of Berkshire's Hathaway Apple position likely represents something far more meaningful and harder to understand.

There are several possible explanations for the size of these sales:

- The sales might have been done in front of an expected Democratic election victory which would undoubtedly lead to an increase in the rate on taxes of realized capital gains (and maybe even on unrealized capital gains). This would be a reasonable explanation, but the marginal impact of a higher tax rate really shouldn't dictate the sale, as Warren has said in the past: "It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price."

- There might be some sort of technical accounting offset/benefit to Berkshire's operations which could result in a rationale for harvesting and realizing gains (e.g. an offset to large catastrophic losses). Again, this reason is probably weak and a stretch, especially given the size of the realized gains in Apple already taken.

- The partial liquidation of Berkshire's Apple and Bank of America shares might be an attempt to prepare the company for Buffett's passing on the torch by creating an even larger and more formidable fortress of cash. This seems to be a possible explanation. Or (and most likely), the stock sales might simply relate to a much more ursine economic and market view than Warren is saying out loud. After all, as I have noted recently, Warren's favorite market indicator/barometer has been signalling sell for months. (See: The Buffett Indicator: Market Cap to GDP - Updated Chart.)

Perhaps Buffett is building cash, because he wants to sit in his bathtub (see the genesis of his BAC investment during The Financial Crisis, and wait for the type of deals he was able to do in 2008- 2009) ... or he might end up owning all of Japan.

In other words, it might be time to Sell American, He Is!

At the time of publication, Kass was short BRK. B (VS).