Prime Time for Amazon, J.D. Vance, Rotation Lives, 3 Charts, Powell Drops a Hint

Let's review how Amazon stock performs after Prime Days, Trump's interesting and unusual VP pick, what's happening with the bond yields, what the market is telling us, and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

A deal for you?

Perhaps. Today is Tuesday, July 16. Today is also day one of Amazon AMZN Prime Day, which has become a two-day bargain hunting affair. Companies like Walmart WMT and Target TGT have come up with competing shopping holidays, but it is Prime Day that steals the consumers' attention, and Amazon that continues to grow overall market share in the retail space through its online dominance. Amazon has held "Prime Day" since 2015 and it has been a success.

The first day of the event in 2023, July 11, was the single largest sales day in Amazon's history. According to Angela Palumbo's piece at the Barron's website, Adobe ADBE Analytics has forecast roughly $14 billion in sales over the event's two days, which would also be a new record. As for its share price, Amazon has averaged a rise or 1.7% for the week following the event and a rise of 4.3% for the month after. I am long the stock, which is up 27% so far in 2024.

Parris Island Goes to Washington

Former President Donald J. Trump was formally nominated by the Republican party in Milwaukee last night and will seek election to his old job this November. Interestingly, Senator J.D. Vance of Ohio has been selected as the party's nominee for Vice President. Maybe five individuals had been seriously considered. Vance is young, at 39, and this is his big chance.

As long-time readers know, I try to hide my personal political preferences and I will not veer away from attempting to appear unbiased and actually be objective now. I will say that I did not know about Vance's military background until recently. Vance enlisted in the United States Marine Corps right out of high school and rose to the rank of corporal before leaving the service. He is a graduate, as am I, of recruit training (boot camp) at Parris Island, South Carolina.

A lot of you might not follow such things, but I do. Plenty of commissioned officers have held high office in this country. The Military Academy at West Point has produced two U.S. presidents, while the Naval Academy at Annapolis one. Many others were schooled in the Ivy League and served as military officers ahead of holding elected positions. Not a lot of kids, though, enlist and then go on to even consideration for such high office.

There's not a lot of information on vice presidents, but among presidents, William McKinley served as a sergeant in the 23rd Ohio Infantry during the Civil War. Harry Truman enlisted in the New York Army National Guard and ultimately deployed to France for World War I. Gerald Ford enlisted in the U.S. Navy during World War II. All three of these men enlisted but became mustangs (eventually were commissioned as officers) prior to mustering out.

In fact, of the 31 U.S. presidents who have any military service, I can only find James Buchanan (whom most historians consider to be the worst U.S. president ever, despite how badly many today want to claim that either Biden or Trump hold that title) who served only as an enlisted person. Buchanan had served as a private in the Pennsylvania militia. There is no modern example of someone like Vance seeking such high office.

Just a quick bit of history that I found interesting and thought you might as well.

Marketplace

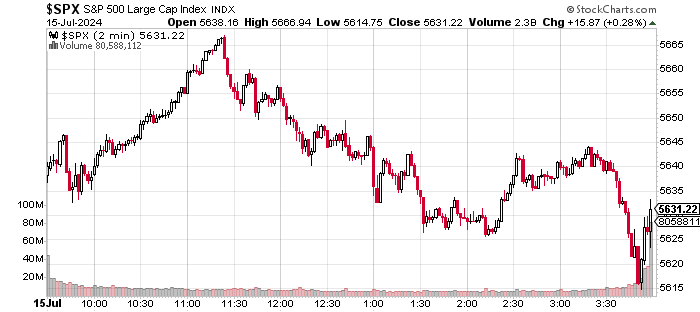

Equities rallied ferociously out of the gate Monday morning in perhaps an exaggerated response to former President Trump's survival over the weekend of the attempt made on his life. What followed over the coming hours would be a volatile session, but on trading volume that has decreased for two successive trading sessions. While the S&P 500 ended the day with a gain of 0.28% and the Nasdaq Composite with a gain of 0.4%, it was the Treasury yield curve where the real market news was made.

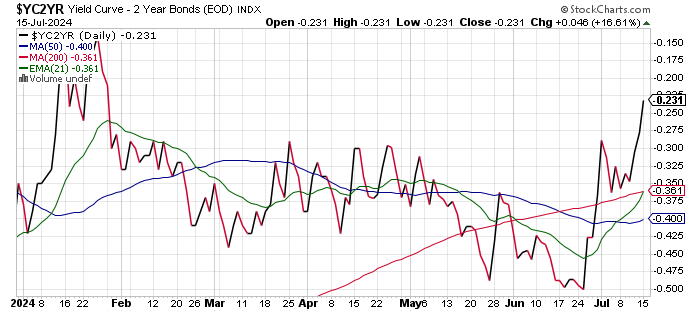

For the day on Monday, the slope of the yield curve "steepened" as the yield for the U.S. 2-Year Note dropped by one basis point to 4.44% and the yield for the U.S. 10-Year Note climbed four basis points to 4.22%. Both of these yields have dropped a bit overnight, but readers will see here that the spread between these two yields is narrowing and ended Monday at its least negatively inverted stance since late January:

As a matter of fact, the spread between the yields of that 2-Year Note and the 30-Year Long Bond did un-invert on Monday and went positive, at least briefly for the first time since January. This morning, I have seen 2-Year, 10-Year and 30-Year paper paying 4.24%, 4.18% and 4.41%, respectively.

Among major to mid-major U.S. equity indexes, only the Philadelphia Semiconductors closed out Monday in the red (just barely at -0.04%), while the largest gains were made by the Russell 2000 (small-caps) and the Dow Transports (+1.8%, +1.67% respectively).

So, is last Thursday's rotation alive and well? It's certainly not dead.

Three Charts

Monday's volatility:

The percentage of S&P 500 stocks trading above their respective 50-day simple moving average (SMAs) has spiked:

While the equal-weighted S&P 500 has rapidly regained ground previously lost to the market-cap weighted S&P 500:

Powell

Fed Chair Jerome Powell spoke publicly on Monday and gave investors more reason to believe that rate cuts are on the way sooner rather than later.

Powell stated: "For a long time, since inflation arrived (as if by stagecoach), it's been appropriate to focus mainly on inflation. But now that inflation has come down and the labor market has indeed cooled off, we're going to be looking at both mandates. They're in much better balance and that means that if we were to see an unexpected weakening in the labor market, then that might also be a reason for reaction by us."

Powell added: "If you wait until inflation gets all the way down to 2%, you've probably waited too long because the tightening... is still having an effect, which will probably drive inflation below 2%."

What concerns me is this. Powell mentioned the three months in a row of improving or slowing readings for consumer-level inflation. He made no mention of the five consecutive months of reacceleration in producer prices. It stands to reason that these increases in producer prices will end up being somewhat visible in consumer prices, likely by this autumn, unless outright recession gets here first. Certainly, a time to remain vigilant for policy makers, in my opinion.

The Macro

This morning, the highly focused upon June reading for Retail Sales will cross the tape at 8:30 ET. Retail Sales have posted back-to-back tough months in April and May, so this reading will take on increased importance. The Atlanta Fed will revise their Q2 GDPNow model later this morning and will do so again tomorrow after June Housing Starts hit the tape.

As for Monday, the Empire State Manufacturing Survey continues to reflect the regional state of recession that the manufacturing sector has been mired in across the New York Fed's regional district. The headline print landed at -6.6, which made for an eighth consecutive month of contraction for the series. New Orders, Unfilled Orders, and Inventories continue to contract across the NY region, while Prices Paid and Prices received continue to expand. As for employment, the number of employees and average workweek continue to contract as well.

Monday's Internals

Winners beat losers at the NYSE by roughly 4 to 3 margin and at the Nasdaq by about 3 to 2. Advancing volume took a positive, but far more balanced share of the whole than it had on Friday. Advancing volume took a 55% share of NYSE-listed and a 61.7% share of Nasdaq-listed trade. However, as mentioned above, aggregate trading volume ebbed for listings across both exchanges for a second straight day, which may have been an expression of caution as the indexes are becoming short-term overbought ahead of this week's higher level macroeconomic events and earnings releases.

Six of the 11 S&P sector SPDR ETFs shaded into the green on Monday, led by Energy XLE and the Financials XLF, both of which were up close to 1.5% on the day. The downside was led by the Utilities XLU. That fund was brutalized for a loss of 2.43%.

Is it important that the three top-performing sectors on Monday are "cyclicals" and the three worst-performing sectors on Monday are defensive in nature? It will be if it keeps happening. It could mean that equities don't fear economic contraction in the medium-term future. It could mean that a devaluation of the U.S. dollar is on the way. How lucky are we to live in such interesting times.

Know What's Worse Than Working on Tuesday Morning?

Not working on Tuesday morning. God bless and carry on.

Economics (All Times Eastern)

08:30 - Retail Sales (June): Expecting -0.1% m/m, Last 0.1% m/m.

08:30 - Core Retail Sales (June): Expecting 0.1% m/m, Last -0.1% m/m.

08:30 - Export Prices (June): Expecting -0.3% m/m, Last -0.6% m/m.

08:30 - Import Prices (June): Expecting 0.2% m/m, Last -0.4% m/m.

08:55 - Redbook: Last 6.3% y/y.

10:00 - Business Inventories (May): Expecting 0.3% m/m, Last 0.3% m/m.

10:00 - NAHB Housing Market Index (July): Expecting 44, Last 43.

16:30 - API Oil Inventories: Last -1.9M.

The Fed (All Times Eastern)

14:45 - Speaker: Reserve Board Gov. Adriana Kugler.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BAC (0.80), MS (1.65), PNC (3.07), UNH (6.35)

After the Close: IBKR (1.74), JBHT (1.51)

At the time of publication, Guilfoyle was long AMZN and WMT equity.