Month-End Markup, S&P's Summer, Why September's Are Weak, The Week Ahead

A new month beckons like some temptation of fate. Out with the old, in with the new. Out with the warmth of summer, in with the cold, wet days of autumn.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Turn the Page

A day, a week, a month-end with a flourish. If that's what you'd like to call it. I'd just as soon call it an old-fashioned "end of month" markup if you don't mind.

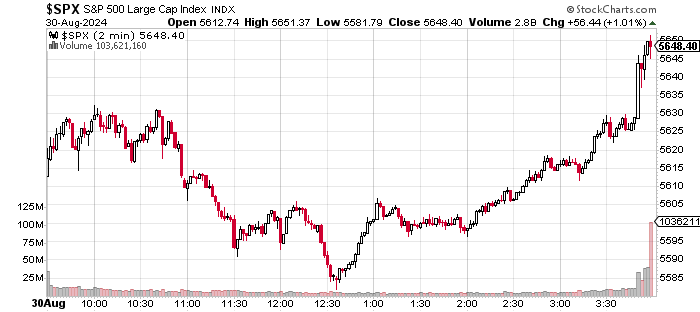

For those who cut out early on Friday for the holiday weekend and have no idea what I am writing about, U.S. equities traded straight up over the final 15 minutes or so of that most recent regular trading session. This is what a two-minute chart of the S&P 500 for this past Friday looks like:

For the session, the S&P 500 gained 1.01%, while every single major and mid-major U.S. equity index came along for the ride. Only the VIX was left in the red along with some commodity-based indexes.

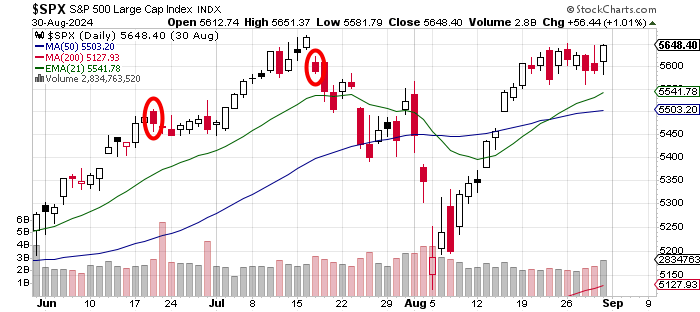

As August ended, the market universe could be seen only through an inviting green lens. That is not, however, the prism through which markets were seen as the month began. For the month that ended with the warm embrace of anticipation, or the mass yearnings of an initiation of some new era of easier money had begun only a few weeks ago with much wailing and the gnashing of teeth.

In Like a Lion

It was only a month ago. Seems far more distant. On Wednesday, July 31, the Bank of Japan surprised many with an increase to its benchmark short-term interest rate, choosing to support a disintegrating home fiat, over a struggling domestic economy.

That Friday, on August 2, in the U.S., the Bureau of Labor Statistics posted the results of its twin employment surveys for the month of July. This was one of the weakest monthly employment reports seen in the U.S. in many years. Making matters worse, we now know that nearly every month for what is now likely more than a year and a half, the BLS has significantly overstated job creation.

By Monday, August 5, global equity markets were aflame with Japan's Nikkei 225 in the lead, down 12% for the day. The yen carry trade was unwinding. It did not last long, but with the yen rising in value, and other currencies, such as the U.S. dollar losing value, a long-standing carry trade had to be unwound or mostly unwound in a matter of days.

The S&P 500 gave up 3% on August 5 after losing 1.37% and 1.84% for the two sessions prior. The rest of the month of August was spent in a state of recovery, supported by a near-promise at Jackson Hole by Fed Chair Jerome Powell who declared that "The time has come for policy to adjust."

By the end of August, the S&P 500 and Nasdaq Composite among the majority of U.S. equity indexes, had not reclaimed the highs of July, but had indeed closed out the month higher than where they had begun it.

This is what summer 2024 looked like for the S&P 500:

Marketplace

The markets had traded lightly for most of the second half of the month of August. That is until Friday when "end of month" trading activity exploded.

We enter the new month with the next FOMC policy meeting just two weeks out. This new month beckons like some temptation of fate. Out with the old, in with the new. Out with the warmth of summer, in with the cold, wet days of autumn. Starting out with a tease of kindness, ending with the beginning of what becomes a dark, raw, cold and bitter passage into winter.

-- The S&P 500 gained 1.01% on Friday to close the week up just 0.24%.

-- The Nasdaq Composite gained 1.13% on Friday to close the week down 0.92%.

-- The Nasdaq 100 gained 1.29% on Friday to close the week down 0.74%.

-- The Russell 2000 gained 0.67% on Friday to close the week down 0.05%.

-- The S&P Small Cap 600 gained 0.51% on Friday to close the week up 0.03%.

-- The S&P Mid Cap 400 gained 0.73% on Friday to close the week down 0.15%.

-- The Dow Transports gained 1.1% on Friday to close the week up 0.46%.

-- The Philly Semiconductors gained 2.58% Friday & still closed the week down 1.34%.

-- The KBW Bank Index gained 1.17% on Friday to close the week up 1.97%.

On Friday, all 11 S&P sector SPDR ETFs closed in the green with four of those funds gaining at least 1%. Happy, happy. For the week, eight of the 11 sector SPDRs went green, led by the cyclicals that in turn were led by the Financials XLF, which were up 2.95%. For joy, for joy.

However, and perhaps most interesting is that fact that for the month of August, 10 of these 11 sector SPDRs went green with the characteristically defensive funds in the lead as the Utilities XLU, Staples XLP and REITs XLRE all gaining more than 5%. Only Energy XLE closed in the red for the month, down 1.66%.

Defensives in the lead? The cyclical of cyclicals in the red? Sounds ominous.

Seasonality

October has the rep, thanks to 1929 and 1987, but for the past 45 Septembers, as we only went back to 1980, September is the worst month of the year for the S&P 500. Not only is September the worst-performing month of the year on average, but September is the only month of the year with more down years than up years since that time.

Since 1980 (45 Septembers), the ninth month of the year has posted a negative return 25 times, while posting an average return of -1%. September easily came in twelfth place in both categories.

Why is September typically weak? There are a number of reasons.

Portfolio managers usually start to really focus on year-end performance about two-thirds of the way through the year and may take profits on less-than-trusted winners or cut losers in order to set themselves up for a year-end rally, which is also typical, especially in election years.

This is also the time of year that investors have to pay college tuition for family members and thus are more likely to liquidate holdings in order to pay the academic piper. Maybe part of the reason is simply the realization that another summer has passed, and another winter lies ahead.

The Week That Was

Last week was a rather quiet one for macroeconomic data as the investment world focused on Nvidia NVDA earnings. I think it is a potentially positive sign that markets took truly outstanding but honestly decelerating Nvidia results (and guidance) in stride.

Nvidia did give back 7.73% for the week, but still went out on Friday very close to where the stock split 10 for 1 this past June. That did pressure semiconductor stocks broadly, but the major indexes hung in there well. The Tech sector did get a boost from cybersecurity provider CrowdStrike CRWD, which after July's outages, reported a solid quarter and cut guidance less severely than many feared. CRWD was up 2.11% last week.

On the macroeconomic front, Existing and New Home Sales both disappointed for July on Tuesday and Wednesday. On Thursday, the Bureau of Economic Analysis revised its estimate for Q2 GDP from growth of 2.8% to growth of 3.0% (q/q, SAAR).

Almost completely uncovered by the media, however, was the fact that the BEA's estimate for Q2 GDI came to growth of just 1.3%. As we know, the GDP and GDI are supposed to match and when they do not growth is to be expressed as an average of the two. This is the Fed's suggestion as GDP is not superior to GDI in accurately reflecting economic growth or the lack thereof in the aggregate. Somehow, the financial media just "goes with" the higher number. Some elite level of financial journalism there, gang. Not. One would think a lesson learned. One would be wrong.

The big deal last week, though these datapoints rarely provide surprise, was Friday's numbers for July PCE consumer-level inflation, which is what the Fed watches and acts on more so than CPI. Headline and Core PCE printed at growth of 0.2% apiece month over month as projected. On a year-over-year basis though, headline PCE printed at growth of 2.5% and Core PCE printed at growth of 2.6%. In both cases, these numbers were in line with June's pace of annual growth and one tick below projections.

Additionally, within the University of Michigan's end of month revision to its Consumer Sentiment survey, expectations for one-year-out inflation dropped to 2.8% from 2.9%. This set up the end of day markup. Yeehaw.

The GDP Game

On Friday, the Atlanta Fed revised their GDPNow model for the third quarter up to growth of 2.5% (q/q, SAAR) from 2.0%, which seems to me to be a bit on the warm side. Of course, that's just an opinion, but one I am fully qualified to have and state.

Among other central banks running close to real-time GDP models for the current quarter, the New York Fed has Q3 humming along at 2.49%, so they are in agreement with Atlanta. The Cleveland Fed shows growth of 1.61%, and the St. Louis Fed shows growth of 2.05%. Just an FYI here, the St. Louis Fed was the most accurate among the four models for Q1, while Atlanta was the most accurate for Q2.

Expect Atlanta to revise their model later this morning after the ISM Services PMI for July hits the tape and again tomorrow after the BEA publishes the national trade balance for July.

The Week Ahead

The holiday shortened week ahead will be light on high profile earnings as we are unofficially in between earnings seasons at this point. This afternoon, we'll hear from cybersecurity provider Zscaler ZS. On Wednesday morning, Dick's Sporting Goods DKS and Dollar Tree DLTR will report. to be followed on Thursday evening by Broadcom AVGO, and DocuSign DOCU.

The Fed will go easy on us this week. Right now, I only see New York Fed President John Williams speaking and Fed Governor Christopher Waller speaking, both this Friday. That is after the Beige Book is released Wednesday afternoon. As for the macro, the calendar is rather crowded, headlined by the release of the BLS employment surveys this Friday.

Will traders take this monthly report seriously, now that we know beyond the shadow of a doubt that these monthly surveys are wildly inaccurate and modeled to consistently skew substantially higher than what is the American reality? Remember, the vast majority of trading across financial markets is done by algorithm. The algos don't care if the numbers are real or fantasy, The algos will react. Keep that in mind.

The guys at the point of sale with common sense? Those human traders that would refuse to make purchases or sales at "stupid" prices? They have been put out to pasture at the altar of speed and greed. Speed and greed over fair process in price discovery. You can bet your tail all day, every day. That, however, is the way it is. In 2024.

Economics (All Times Eastern)

08:55 - Redbook (Weekly): Last 5.0% y/y.

09:45 - S&P Global Manufacturing PMI (Aug-F): Flashed 48.0.

10:00 - ISM Manufacturing Index (Aug): Expecting 47.5, Last 46.8.

10:00 - Consumer Spending (July): Expecting 0.1% m/m, Last -0.3% m/m.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: GTLB (0.10), ZS (0.69)

At the time of publication, Guilfoyle was long NVD, CRWD and XLU.