Money, Money, Money (Supply)

Let's look at M2 Money Supply, October uncertainties and why we should watch out for ... BRICS.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The S&P 500 closed at a new record on Thursday. Then, it repeated the feat on Friday. Just an FYI: Friday was the S&P 500's 47th record close since the start of calendar year 2024. That's almost five times a month, on average, for 10 months, that the S&P 500 has closed at a new record high. Seems legit. I mean if money supply and high debt are indeed what causes inflation, then it all makes sense. Sometimes, the Treasury Department and the Federal Reserve, through the often more-than-borderline abuse of policy, can misdirect that inflation into risk assets and away from consumer goods and services and, sometimes, they cannot.

For those wondering, M2 Money Supply stood at a rough 21.1749 trillion in August, up from $20.7514 trillion in January. Yes, even with the central bank working feverishly at reducing its balance sheet and with it, the monetary base through the non-contact sport known as quantitative tightening. Restrictive policy? LOL. M2 Money Supply was up more than 2% over those seven months. That's lots of dough, if you ask me. Oh, did I mention that the federal debt-load is up 5.2% since the start of 2024? Just don't get me started on state, local, business and household debt, you know ... all of those things that go into the goods and services tallied up to make gross domestic product or gross domestic income what it (supposedly) is? Then, as a nation our debt-to-GDP ratio is a mere 349%, give or take. Guess we'll just go with U.S. federal debt, so we can say that the debt to GDP ratio is "a mere" 122%.

So, drink up, me hearties (coffee, we're drinking coffee), for it may be the Fed's job to support full employment and stable prices, and it may be the Department of the Treasury's job to fund the U.S. government, all of that is true. Just remember, while we all pretend that the independence of the central bank is sacred, that the Federal government could never have taken fiscal policy to the perverse levels reached over decades, but greatly accelerated in recent years, if there had not been an enabler.

That enabler was the central bank. You know it, and they know it. Hardly independent. It also would behoove all who pass this way or read these words to remember that the Federal government cannot afford to service that debt-load without making huge sacrifices elsewhere at wherever it is that borrowing costs might land if free market forces were permitted to control the bond market. Therefore, and I have told you this many times ... inflation is going to accelerate again. The federal government needs it to, at the expense of the U.S. dollar, at the expense of savers and those living on fixed incomes.

They have no choice, and if you and I are in the way, then we too will be part of that sacrifice. We all have to be more than passive. We have to defend ourselves through macro-aggression. Not micro. Understand what has to be done and front-run the policy. Even if the central bank maintains control over the short end of the yield curve, there stands a better than a puncher's chance that without renewed "quantitative easing" at some point, that long end of the curve may trade where it should. This would very likely be an unacceptable outcome to the powers that be.

The Week That Was

There was a lot to take in over the past week. I was off. Hope you noticed, but I bet you did pretty well. All of my accounts closed considerably higher than where I had left them a week earlier. S&P 500 record highs? How about record highs for the Sarge-folios? Yeah, doggies (this is how one jinxes oneself), from the accounts that I leave to others to trade for me as well as the ones that I manage myself and then left alone all week, it made no difference. As a matter of fact, I outperformed the guys I pay to run money, despite that I was doing Florida things with non-Floridian relatives and not paying nearly as much attention, even when away, as I usually do.

There was not a lot of macro-economic data released through the early part of last week. Then, on Thursday, September retail sales printed better than expected. Party! The October Philly Fed was hot, too. September industrial production was back in the tank, so we just put it out of mind. September housing starts and building permits both disappointed, as well. Forget about it. There's a party going on and we're all invited. Just ride the wind until the wind refuses to blow. Then will come the wickedness and the dark times. For we care not. Just keep the music going.

It Really Was About Earnings

Things got a little ugly on Tuesday when Dutch semiconductor equipment company ASML Holding ASML fell short of expectations for quarterly bookings, while warning of a "more gradual than previously expected" recovery in semiconductor-related business not involved in or adjacent to artificial intelligence. Two days later, Taiwan Semiconductor TSM came to the rescue. Taiwan Semi reported a blow-out quarter, gave hope to the masses. The children all sang out joyously as the AI trade was back on. Rock 'n' roll.

Away from the semis, the financials remained hot after Morgan Stanley MS reported a rebound in its investment banking business. Apple AAPL popped in response to data released by Counterpoint Research showing that iPhone 16 sales in China are up 20% since the new smartphone's release. Few stocks were able to top what Netflix NFLX did on Friday, though, gaining 11% after reporting quarterly earnings and subscriber growth that beat Wall Street.

Not everyone came home a winner, though. CVS Health CVS took a 5% beating after issuing preliminary third-quarter results that missed by a mile and canceling full-year guidance. CVS also ousted now former CEO Karen Lynch and replaced her with David Joyner who had been running the Caremark division. American Express AXP also surrendered 3% on Friday after shaving that firm's guidance for full-year revenue growth.

Marketplace

No, I don't think anything terrible happens to U.S. financial markets prior to the national election in the U.S. on Nov. 5, the Federal Open Market Committee's policy statement on Nov. 7, nor the known outcome of that U.S. election, whenever that may be. That said, this past September was not a normal September for U,S, markets and we are not out of the October woods just yet. If you are of age, you have learned to if not fear, then at least respect what October can do.

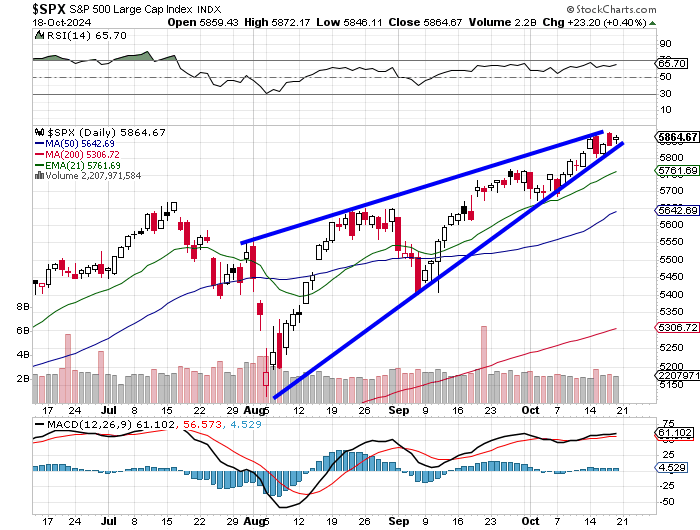

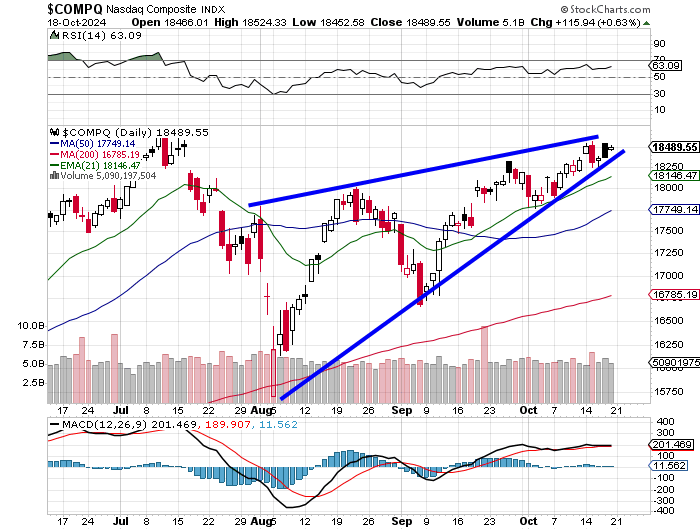

You kids have all heard of "rising wedge" patterns, correct?

By definition, rising wedges are patterns of bearish reversal that often tend to take three to six months to fully develop. Are we there yet? No. How will we know when we are there? You'll know, gang. The supporting trendline must break on an increase in trading volume after trading volume has gradually ebbed as prices ran higher. I do some of that gradual erosion in trading volume, but it's not overwhelmingly obvious just yet.

As for U.S. equities last week ...

- The S&P 500 gained 0.4% on Friday to close the week up 0.85%.

- The Nasdaq Composite gained 0.63% on Friday to close the week up 0.8%.

- The Nasdaq 100 gained 0.66% on Friday to close the week up just 0.26%.

- The Russell 2000 gave back 0.21% on Friday, but still closed the week up 1.87%.

- The S&P Small Cap 600 gave back 0.32% on Friday but closed the week up 1.64%.

- The S&P Mid Cap 400 gained just 0.01% on Friday, closing the week up 1.41%.

- The Dow Transports gained 0.31% on Friday, to close the week up 0.89%.

- The Philly Semiconductors gained 0.07% on Friday but closed the week down 2.39%.

- The KBW Bank Index gave up 0.31% on Friday, closing the week up 2.79%.

On Friday, ten of the 11 S&P sector SPDR ETFs closed in the green, with Communication Services XLC out in front at +0.74%. Only Energy XLE closed in the red. For the week, nine of the 11 S&P sector SPDR ETFs closed in the green, led by two defensive sectors... the Utilities XLU and The REITs XLRE, both of whom gained more than 3% over the five-day period. Energy was the week's loser as well, giving up 2.66%.

Earnings

According to FactSet, which is my "go-to" for all things earnings-related, third quarter results are dragging just a bit. Right now, for that third quarter, S&P 500 earnings are showing blended (results & expectations) year-over-year growth of 3.4%. That's down from 4.2% two weeks ago, and down from 4.9% four weeks ago. Revenue growth is currently running at blended 5%, down from 5.1% two weeks ago.

This slowing of expectations for the third quarter is impacting the consensus view for both the fourth quarter and the full year. Q4 earnings growth is now seen at 14%, down from 14.6%, while full year earnings growth is now seen at 9.4%, down from 10.2% three weeks ago.

For the third quarter, double-digit earnings growth is now only expected from the Technology, and Communication Services sectors. Expectations for Health Care sector earnings growth have dropped from all the way from 11.1% to just 5.7%. The Financials, Industrials and Energy sectors are all expected to post year over year earnings contraction, with close calls expected for both the Staples and Discretionaries.

The S&P 500 goes into this week trading at 21.9-times forward looking earnings, which is well above the five- and ten-year averages for the index of 19.5 and 18.1 times, respectively. The S&P 500 also trades at 27.4 times trailing twelve months' earnings, which is also well above the five- and ten-year averages of 23.9 times and 21.8 times.

The GDP Game

Last week, the Atlanta Fed revised its GDPNow model for the third quarter up to growth of 3.4% quarter-over-quarter, seasonally adjusted annual rate from 3.2%. Among other central banks running close to real-time GDP models for the current quarter, the New York Fed revised its Q3 estimate down to 3.0% from 3.1%, so apparently, they are less optimistic than is Atlanta. The Cleveland Fed left their Q3 estimate at growth of 1.45%, while the St. Louis Fed took their estimate for the third quarter up to growth of 1.78% from 1.7%. Suddenly, we have four Fed GDP models that for the third quarter are all telling us something different.

Reports for the Week Ahead

Most readers are probably concerned with whatever macroeconomic data is due this week as well as what key earnings releases are due. As there are no FANG or "Magnificent Seven" stocks reporting this week, there may be a few other items worthy of finding a spot on your "investor or trader radar" this week. There are several Fed speakers out and about, but the markets seem to care less and less about words spoken and will be satisfied as long as futures markets continue to price in consistent cuts of quarter-points per FOMC meeting going forward.

As far as the macro is concerned, there's not a lot of meat on the bones this week. September existing and new home sales will print on Wednesday and Thursday. This will be followed up by September durable goods orders on Friday, along with revisions to the University of Michigan's October survey on consumer sentiment and inflation expectations.

Concerning corporate earnings, there are some headline level names reporting over the next five days. Among them will be GE Aerospace GE, General Motors GM, Lockheed Martin LMT, AT&T T, Boeing BA, Coca Cola KO, ServiceNow NOW, Tesla TSLA, Union Pacific UNP and United Parcel Services UPS.

A Ton of BRICS

Well, there is the twice a year IMF Meetings that will last from Monday through Saturday in Washington. Leaders from the IMF and the World Bank will be there. I wouldn't get too concerned about this, though, as these groups have a long history of providing little in the way of value, while often making inaccurate projections. It's what they're good at.

What does have me concerned though, is the BRICS Summit. The group is meeting for three days this week in Kazan, Russia so that Russian Pres. Vladimir Putin can attend without having to travel across borders. Also expected to appear are Chinese President Xi Jinping, and Indian Prime Minister Narendra Modi. Representatives will attend from South Africa, and Brazil, and perhaps other several other nations as well. Brazilian President Luiz Lula da Silva will not be attending due to an injury sustained after falling at his residence. He will attend however, via videoconference.

Why does this summit concern me? At the recent business forum in Moscow, the group unveiled its BRICS Pay system, which is obviously intended as a first and perhaps major step toward ending the dominance of the U.S. dollar as the planet's leading reserve currency. Now, think with me for a moment. Go back and read the first section of this lengthy, but necessary morning note if you must.

Maybe the BRICS and financially allied nations don't take anything any further than that at this time, but maybe they do. We know that their central banks have been trying to load up on gold for years. What if one of these summits actually produces a monetary union, similar in organization to the Euro-Zone, but with a common currency backed by a hard asset such as gold? Barbarous relic? I think not. Just what do you think all of this fiat currency around the planet will be worth if there were to be a major competitor backed by something other than the promise of a sovereign that has already proven itself fiscally irresponsible?

The Treasury Department would be forced to at least consider backing its debt with something tangible, if not all of its currency. That would be the only way that anyone would even think of extending credit (buying Treasury debt securities) to the United States. Maybe the BRICS do not go there. They have been just as fiscally irresponsible.

It is, however, a threat. A threat that would have the Senate asking someone like Judy Shelton to please take on a leadership role in reinforcing the soundness of the American dollar. It may also have our legislator's embracing rather than shunning economist Stephanie Pomboy's (of Macro Mavens) proposal concerning tax free interest income on US Treasuries as a lure to help the Fed control federal borrowing costs.

Economics (All Times Eastern)

08:30 - CB Leading Indicators (Sep): Expecting -0.3% m/m, Last -0.2% m/m.

The Fed (All Times Eastern)

08:55 - Speaker: Dallas Fed Pres. Lorie Logan.

1:00 p.m. - Speaker: Minneapolis Fed Pres. Neel Kashkari.

5:05 p.m. - Speaker: Kansas City Fed Pres. Jeffrey Schmid.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: NUE (1.41), SAP (1.21)

At the time of publication, Guilfoyle was long XLU, GE, LMT.