Market Tilt-A-Whirl, Turning Point? Fiscal Armageddon, Week Ahead

Think we spend too much on defense? During the Cold War, the U.S. typically spent roughly 5% of GDP on defense. Today, it amounts to just 2.9%.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Going into the second half of what was a four-day workweek, split by a federal holiday, with a "triple-witching" expiration event and a re-balancing of several index-tracking ETFs looming, trading volumes began to pick up. It appears, at least on the surface, however, that volatility did not. This of course means that there must have been considerable churn, considerable rolling over of weekly and monthly options exposure, and of course some rotation. That's right, some rotation out of the exceedingly narrow AI-focused tech trade and into a broader equity market.

Equities, away from the major large-cap indexes (I don't consider the DJIA a major), more or less worked their way higher, while Treasuries rallied, sold off and then rallied again in response to a bevy of macroeconomic data that was weaker than it was strong.

I wrote to you last week, going into high-volume trading events such as what we just experienced to try to not take too much away from the price discovery that markets go through when that action is forced. Especially, now that there are very nearly no thinking, sentient beings behind the creation of said prices.

Marketplace

Equities started out rather strong on Thursday morning after rallying on Monday and doing better than holding their own on Tuesday. The simple-minded were heard shrieking with delight as the S&P 500 crossed over 5500 around 15 minutes after the opening bell that day. Close to 25 minutes later the S&P 500 re-crossed that line for the final time last week.

Blame the macro? Blame the rebalancing? You've got a bigger, badder one of those coming up this Friday. Blame the witches? Sure, balance the witches. Whatever floats your boat. The S&P 500 gave up a mere 0.16% on Friday to close the week up 0.61%.

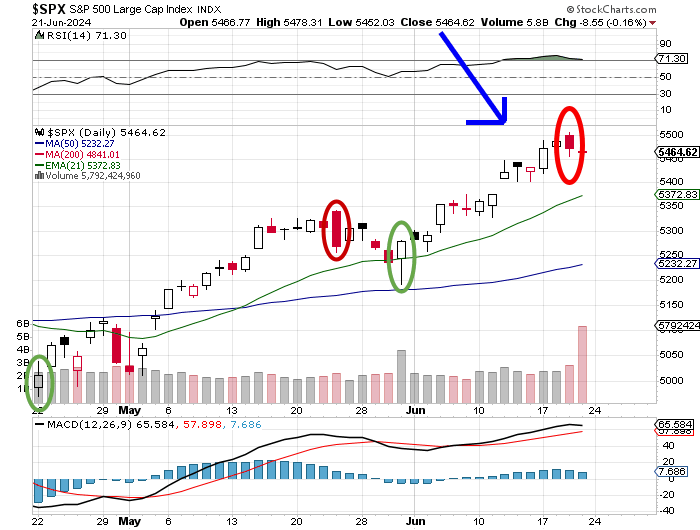

Take a look at this:

The media asked repeatedly: Has the market turned? I honestly don't know. Sure, Thursday may have been a Day One bearish reversal, but that doesn't look much like a "shooting star" to me. Friday was a "down" day on elevated trading volume, which doesn't really mean much in broad terms. I've already told you that. It's easy to see that for the S&P 500, Relative Strength and the Moving Average Convergence Divergence (MACD) are both still very strong on the daily chart.

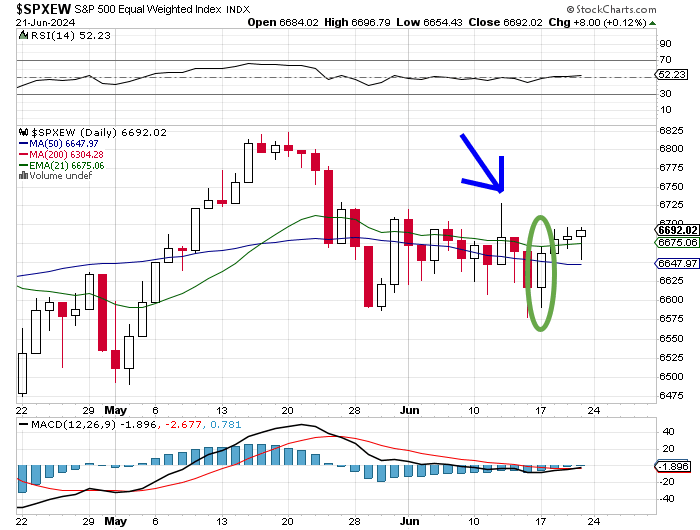

Level the playing field, and guess what? Nobody is asking that question. It's not just traders getting out of large-caps and into smaller-caps, though we have seen some of that, it's portfolio managers re-allocating away from those few mega-caps considered to be magnificent and into the nearly 500 other stocks that comprise the S&P 500.

Note the chart below:

We are talking about the same 500 stocks, just weighted equally and not by market-cap. Suddenly, we have a Day One bullish reversal back on Monday and this (not really an) index hasn't not looked back since. Here we see a reading for Relative Strength that remains neutral, but a daily MACD that appears to have experienced a bullish crossover of its 26-day exponential moving average (EMA) by its 12-day EMA, while the histogram of its 9-day EMA snuck into positive territory.

So, again, did we see a turning point last week? If so, in which direction? Then again, with half of the action forced late last week, can I let you know in a few days? I did not make major changes to my portfolio last week.

The Rest of the Field

The Nasdaq Composite... wait for it, gave up 0.18% on Friday, to close unchanged, yea, unchanged for the week. The Nasdaq 100 rallied last week for a whopping 0.21%. Jeekies. The Dow Transports led all major and mid-major indexes last week with a gain of 2.07%, with the KBW Banks (+1.61%) not too far behind. The mid-cap and small-cap indexes rallied. The Semiconductors? Not so much.

The Philadelphia Semiconductor Index lost a modest 1.07% last week, but that did not really tell the tale. The less closely watched Dow Jones U.S. Semiconductor Index backed up a nasty 2.81%. Folks put the blame there on Nvidia NVDA as that stock finally sold off when traders were looking for a late-week rally. NVDA surrendered 4.03% last week, but worse than that, On Semiconductor ON was beaten for a loss of 4.79%, while Broadcom AVGO was taken to the woodshed, losing 4.4%.

Even on Friday, with the market supposedly in decline, six of the 11 S&P sector SPDR ETFs closed out that day in the green. For the week, nine of those 11 funds closed higher, with Discretionaries out in front at +2.4%, and with three other funds up at least 1.5% for the four days. What closed lower? The interest-rate sensitive defensive sectors. Sounds awful. The Utilities XLU closed the week off 0.79%, while the REITs XLRE closed down just a smidge.

The Macro

As mentioned above, there was a good bit of weaker-than-expected macroeconomic data points released last week that ultimately had economists shaving (quite moderately) running Q2 GDP expectations.

Early Tuesday morning, the Census Bureau released their numbers for May Retail Sales. At the headline, May Retail Sales printed at monthly growth of 0.1%, well below expectations for 0.3%. That was worse than it looked too, because April Retail Sales were revised to -0.2% m/m from the original print flat of 0.0%. That means that the growth of 0.1% was off of a lower base than had been the expectation for 0.3%.

Retail Sales were weak at the core as well. May Core Retail Sales printed at -0.1%, which was again well below expectations for 0.2%. April Core Retail Sales were revised from the original print of +0.2% m/m down to -0.1%, again making May in reality worse than it looked. Core retail sales have now printed in a state of contraction for two consecutive months.

Then there was some good news, as about 45 minutes later, May Industrial Production hit the tape. This item outperformed expectations for 0.3% growth with a print showing monthly growth of 0.9%. May was the strongest month for industrial Production in the U.S. in two years. Within the headline print, Manufacturing Production also popped for growth of 0.9%, while Mining Production also showed growth of 0.3% after two months of contraction and Utilities Production sported growth of 1.6% in May, which was incredibly a deceleration from a 4.1% April print.

As the week moved on, weekly jobless claims remained uncomfortably elevated for a second straight week, while May Housing Starts and the June Philly Fed Manufacturing survey disappointed. On Friday though, the S&P Global Manufacturing and Services Flash PMIs for June both hit the tape at better-than-expected levels, while May June Existing Home Sales held nearly steady from the month prior.

A mixed bag? More or less, leaning weak, in my opinion. The last item of the week may have been the most important. The Conference Board's Index of Leading Indicators, that is a diffusion index of 10 key macroeconomic statistics printed at -0.5% m/m. This index has now printed in a state of contraction for 21 of the past 22 months.

GDP Revisions

After all of those numbers were released, the Atlanta Fed tweaked their GDPNow real-time model for the second quarter just a bit, down to growth of 3.0% (q/q, SAAR).

The other Fed regional districts that run such models are not nearly as optimistic as Atlanta. The New York Fed shows the second quarter at growth of 1.89%, the St. Louis Fed is now at growth of 0.8% and the Cleveland Fed is at growth of 0.67%.

One of these things is not like the others...

Fiscal Armageddon

Early last week, the nonpartisan Congressional Budget Office (CBO) took their estimate for full fiscal year 2024 federal revenue down to $4.89T from $4.935T, while taking their estimate for full fiscal year 2024 federal outlays to $6.805T from $6.442T. That takes their projected federal deficit for the year to $1.915T from $1.507T.

Imagine being off by $400B in anything at your job? Now consider a world that seems to just get more dangerous daily. Consider that the nation is fiscally strapped with a defense budget that amounts to just 2.9% of GDP. Think we spend too much on defense? Think again. Asia is a fuse looking for a light, while Eastern Europe is a quagmire, where NATO and the U.S. are already in far too deep, and the Middle East is more than just a "mess."

During the Cold War, the U.S. typically spent roughly 5% of GDP on defense. We had a superpower for an adversary back then. Is today much different? We have at least one superpower that acts as an adversary and then we have near peer adversaries that force a U.S. military that has been left to rot in disrepair for several years now with too many holes to plug. NATO allies are increasing defense spending across Europe and Canada by about 18% this year. We are going to have to work that 2.9% back up to 5% or relinquish our ability to project influence as a nation.

What then? Where will discretionary spending be cut? A lot and I mean a lot of discretionary spending has to be cut from the federal budget, and that's without going into austerity. That's just to be able to defend our nation and our people from those intent on doing us harm. Not just food for thought.

We have fiscal problems to solve thanks to the recklessness of our legislature coming out of the pandemic era. Interest expense will reach 3.1% of GDP this year, outstripping defense spending. That same CBO projects that the federal government will spend roughly twice as much on interest as on defense within 15 years or so.

At what point will there be no room whatsoever, for any discretionary spending? Without monetizing the debt. What if the BRICS really do create their own monetary union based on a currency backed by gold? Let that thought sink in.

Who's Number One?

Early last week, Nvidia snatched the crown of most highly valued company in the world with a market cap of $3.3 trillion. Nvidia's time as "king of the hill" was short, though.

By week's end, Microsoft MSFT reclaimed the top spot with a market cap of $3.34 trillion, while Apple AAPL reclaimed second place with a market cap of $3.18 trillion. Don't feel too bad for Nvidia. Jensen "The Fonz" Huang and company are still in third place at $3.11 trillion.

The Week Ahead

The earnings calendar remains thin this week, as we make our way between earnings seasons. We won't start hearing Q2 numbers from the big banks until the second week of July. That said, we will almost certainly hear news from and about the big banks this week.

Corporate... There is just one corporate event outside of earnings that caught my eye for the week ahead. Datadog DDOG will hold that firm's annual DASH event in New York City this Tuesday and Wednesday. As for the few earnings we do have, FedEx FDX will report this Tuesday afternoon. We'll hear from General Mills GIS ahead of the opening bell on Wednesday and from Levi Strauss LEVI after the close that same day. On Thursday, the action gets a little busier with McCormick MKC, Walgreens Boots Alliance WBA and Nike NKE all going to the tape with their numbers.

The Fed... There are several Fed speakers this week. I am more than a little interested in what message is being prepared as this Friday, the PCE data for May will hit the tape and the Fed is sending out Gov. Michelle Bowman and Richmond Fed Pres. Tom Barkin (both hawks) the very same day. In addition, this Wednesday, after the closing bell, the Fed will release its stress test results for 2024 for the 32 largest banks in the nation.

Macro... The headline event for the week will be this Friday's May data for PCE, Core PCE, Personal Income and Personal Spending. Before we get that far, we'll have to run through April home prices, June Consumer Confidence, May New Home Sales, May Durable Goods Orders, and the BEA's final revision to Q1 GDP.

Lastly... This Friday brings the annual Russell Rebalance, also known as the Reconstitution of Russell Indexes. This day is typically the busiest day trading day of the year at the NYSE.

Economics (All Times Eastern)

10:30 - Dallas Fed Manufacturing Index (Jun): Expecting -13, Last -19.4.

The Fed (All Times Eastern)

03:00 - Speaker: Reserve Board Gov. Christopher Waller.

14:00 - Speaker: San Francisco Fed Pres. Mary Daly.

Today's Earnings Highlights (Consensus EPS Expectations)

No significant quarterly earnings scheduled.

At the time of publication, Guilfoyle was long NVDA, MSFT and AAPL equity.