Marching Up Wall Street

On this Veterans Day, let's review the oath with no expiration date, the Trump bump, and the chart of the S&P.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I (name) do solemnly swear that I will support and defend the Constitution of the United States against all enemies, foreign and domestic, that I will bear true faith and allegiance to the same; and that I will obey the orders of the President of the United States and the orders of the officers appointed over me, according to regulations and the Uniform Code of Military Justice. So help me God.

Those successfully accepted into service in the armed forces of the United States must take this oath, which is an accomplishment in itself as 75% of recent high school graduates for one reason or another, do not qualify. Primarily, today's young potential recruits are disqualified for a lack of physical fitness. That's right, roughly three-quarters of today's young people are unable to enlist even if they wanted to. That's what technology and a highly processed diet has wrought.

That said, when one has left the services and then re-enters, though there is never an expiration date placed on the words above, one recites the oath again. Trust me when I say that you utter these words slowly, and as seriously as possible. I like to think that no one utters these words without concentrating on them. It is an oath with no expiration date.

I took that oath at the age of 17, then again at 45 and then again at 48. As an old man, I had to relearn most of the equipment as cool things like night vision and GPS had not yet been invented while I was off being a Wall Street guy. That gave me an advantage, though. As the young kids could teach me about the new equipment, I could teach them so many things about being a Marine or a Soldier that had been partially forgotten over time. You see, I enlisted for the first time in the post-Vietnam era. My sergeants were Vietnam War veterans, and my friends, those guys were perhaps the greatest warriors of all-time.

The U.S. Code of Military Conduct

Article I - I am an American, fighting in the forces which guard my country and our way of life. I am prepared to give my life in their defense.

Article II - I will never surrender of my own free will. If in command, I will never surrender the members of my command while they still have the means to resist.

Happy Veterans Day, gang. Yes, this is the one where you can say the word "Happy" in connection to the holiday, though you and I are both at work. Veterans Day celebrates all honorably discharged veterans and all those still serving. Memorial Day is a day of solemnity where we honor those fallen in service to our nation. We never, ever say "happy" Memorial Day. Just an FYI, for those who may not have known the difference. U.S. equity markets will trade normally today, kids. Bond markets are, however, closed, as this is a federal / bank holiday.

The Week That Was

Where do I even begin? We knew the week past would be a wild one. We feared the possibility of a long, dragged-out post-election period where there would be legal battles and possibly no clear winner. Wow, were we ever wrong. The nation clearly chose a new direction, and the election never really was all that close. From early on Tuesday afternoon, the odds of former President Trump's victory kept improving on websites that track those things.

Even while the cable news channels were still anticipating a close finish, these websites had now President-Elect Trump's chances at over 90%+ fairly early on. Financial markets started pricing in a Trump victory, a Republican-led Senate and the likelihood of a Republican-led House during the regular trading session that day. They came out in droves. Trump made huge gains across demographics that Republicans had never done well with before. That success showed down-ballot as well.

I am not here to talk politics unless politics is the story behind market performance, and last week, there was a near euphoric reaction across U.S. equity markets at least, at the thought of Republican leadership for at least the next two years. or at the thought of a unified government, which is not usually seen as a market positive. Debt security markets were less excited at the prospect of this near-term future, but seemed to take it all in stride.

Of course, the Federal Reserve's FOMC statement may have had something to do with that. By Thursday, focus had at least partially if not mostly turned to monetary policy and the Fed's unanimous decision to reduce its target range for the Fed Funds Rate by a quarter-percentage point, while continuing on with its quantitative tightening program. Treasuries had taken a beating mid-week only to rally into week's end, going out on Friday, approximately where they had been prior to the election having been called in the former president's favor.

The Republican-led government is seen as mostly pro-growth, which was not really a problem of late, and possibly inflationary, but that remains to be seen. The idea of an across-the-board tariff war would be inflationary, but might also be necessary to level the playing field with nations that hold a serious advantage in trade with the U.S. These tariffs, in many cases, may merely be negotiation tactics, and if not, while admittedly inflationary, would certainly redomicile a higher quality of middle-class employment opportunity to the U.S.

On the other side of the coin, the president is known to be looking to slash the fudge from the federal budget where possible and has reportedly tasked Tesla TSLA CEO Elon Musk with finding up to $2 trillion in efficiency savings that might be carved from that budget. While the number might be farcical, the fact that budget cuts are coming probably is not. This will be a deflationary force that could to some degree counter increased tariffs applied in tic-for-tat fashion where there is currently an imbalance in import/export relationships.

As for the Fed, the FOMC did take the target range for the Fed Funds Rate down to 4.5% - 4.75%, but the prospects for a lower terminal rate appear to have faded. Futures markets are now pricing in a terminal rate of 3.75% to 4% by July 30. The press conference was more about whether or not Fed Chair Jerome Powell thought he could be fired by the incoming president than anything substantive.

Economics: The GDP Game

Last week was a light week for domestic macro. On Tuesday, the ISM Services PMI for October hit the tape and was rather strong, at least at the headline level. On Thursday, we found out that non-farm productivity for the third quarter printed well below expectations, while unit labor costs were much hotter than projected and up sharply from the quarter prior. On Friday, we learned that according to the University of Michigan, consumer sentiment had started to turn more optimistic even as current conditions continued to deteriorate.

The Atlanta Fed revised their GDPNow model estimate for the fourth quarter upward from 2.3% to growth of 2.5% quarter-over-quarter at a seasonally adjusted annual rate. Among other regional central bank branches running close to real-time GDP models for the current quarter, the New York Fed revised its fourth-quarter estimate for growth to 2.06% from 2.01%, while the Cleveland Fed reduced that estimate for Q4 growth all the way from 2.66% to just 1.84%. The St. Louis Fed still is yet to post a Q4 estimate for GDP growth.

Marketplace Marches Higher

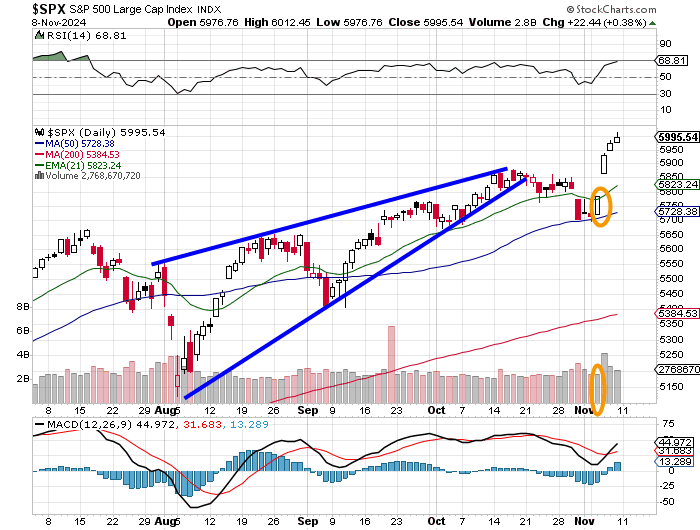

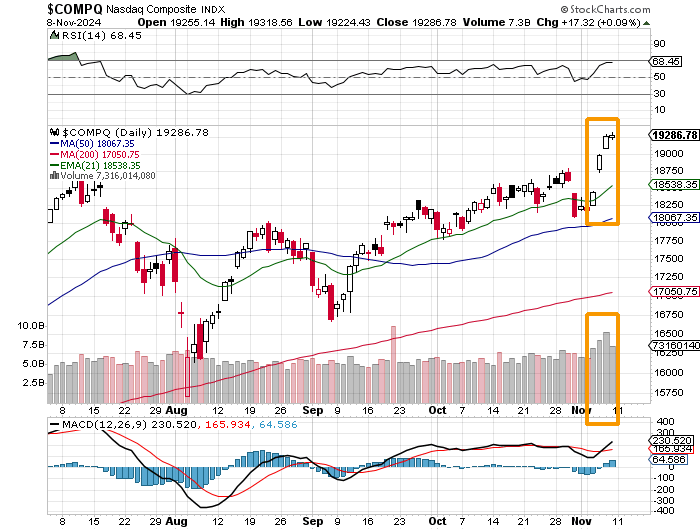

Just wow. That's all there is to say. Both the S&P 500 and Nasdaq Composite posted a "day one" reversal of trend last Tuesday, Election Day. There was, for a couple of days, a continuation of that move on increased trading volume before Friday cooled things down just a bit, even if there has still been no "let up" in the rally at the major equity index level.

Readers will see that we got the selloff that we projected coming out of the closing pennant formation and then, boom! Election Day hit with the surprisingly one-sided results. Relative Strength remains strong, but is not yet technically overbought, while the daily moving average convergence divergence indicator is now decisively bullish. To truly confirm this change in trend, I would prefer to see a couple of days of basing consolidation before the rally resumes. That, however, does not mean that the market will do what I like just to make it fit a technical narrative.

Trading volume did finally pause on Friday as several mid-major equity indexes actually slowed their upward climb. That said, U.S. equity index futures have been trading higher overnight. Here also, we find a muscular, yet not overbought reading for Relative Strength and an overtly bullish looking daily MACD.

As for the major to mid-major U.S. equity indexes last week ...

- The S&P 500 gained 0.38% on Friday to close the week up 4.66%.

- The Nasdaq Composite gained 0.09% on Friday to still close the week up 5.74%.

- The Nasdaq 100 gained 0.0.7% on Friday to close the week up 5.41%.

- The Russell 2000 gained 0.71% on Friday, to close the week up 8.57%.

- The S&P Small Cap 600 gained 0.55% on Friday to close the week up 8.57%. Not a misprint.

- The S&P Mid Cap 400 gained 0.49% on Friday, closing the week up 6.27%.

- The Dow Transports gained 0.83% on Friday to close the week up 6.13%.

- The Philly Semiconductors gave up 0.81% on Friday, but still closed the week up 5.78%.

- The KBW Bank Index gained 0.31% on Friday, closing the week up 8.43%.

On Friday, eight of the 11 S&P sector SPDR exchange-traded funds closed in the green, with the Utilities XLU out in front at +1.92%. followed by the REITs XLRE at +1.71%. The Materials XLB led the day's losers at -0.91%.

For the week, all 11 S&P sector SPDR ETFs closed in the green with Consumer Discretionaries XLY, Energy XLE and the Industrials XLI up a stunning 7.51%, 6.5% and 6.03% respectively. In fact, 10 of the 11 sector SPDRs gained at least 1% for the week, with only the Staples XLP failing to do so. Defensive sectors took four of the five bottom rungs on the weekly performance tables, with cyclicals taking four of the top five.

Earnings

According to FactSet, which is the service that readers know I rely on for all things earnings-related, third quarter results have continued to improve from where they were. Currently, for the third quarter, with 91% of the S&P 500 having reported, earnings are showing blended (results & expectations) year over year growth rate of 5.3% up from 5.1% a week ago and 3.6% the week prior. Revenue growth is currently running at a blended growth rate of 5.5%, up from 5.2% last week.

Results and expectations for the third quarter are no longer negatively impacting the consensus view for both the fourth quarter and for the full year as they had been a few weeks ago. Q4 earnings growth is now seen at 12.2%, down from 12.7% last week while full year earnings growth is now seen at 9.4%, up from 9.3%, where it had been for a couple of weeks in a row.

For the third quarter, double-digit earnings growth is now only expected from the Communication Services (+23%), and Health Care (+13.9%) sectors. Expectations for Tech sector earnings growth have dropped all the way from +15.6% to just +6.9%. The Materials, Industrials and Energy (-25.5%) sectors are all still expected to post year over year earnings contraction.

The S&P 500 goes into this week trading at an almost stunning 22.2 times forward looking earnings, up from 21.3 just a week ago...which is well above the five- and ten-year averages for the index of 19.6 and 18.1 times, respectively. This is now the highest forward-looking valuation placed upon the S&P 500 in more than three years. According to FactSet, the 25-year high for S&P 500 forward looking valuation by PE was 24.4 times in May 2000, so we're not quite there yet. The S&P 500 also trades at 27.9 times trailing twelve months' earnings, down from 26.7 times a week ago...which is also well above the five- and ten-year averages of 23.9 times and 21.8 times.

The Week Ahead

The week ahead will be busier in terms of macroeconomic releases and high-profile corporate earnings than was last week. Then, there will be the plethora of fed speakers that will crawl out of their holes publicly now that we are past the election and last week's policy meeting.

On the macro side, October CPI is due this Wednesday. Coming off of the 2.4% year-over-year growth print for September, most of the street is up around 2.6% for this release. October Producer Prices will hit the tape on Thursday, where we are expecting to see a more pronounced increase from September than we'll get for consumer pricing. On Friday, October retail sales and industrial production will be released. The Atlanta Fed will revise its GDPNow model for the fourth quarter that day.

Between Tuesday and Thursday, I am tracking at least 12 public appearances by high-ranking Fed officials. The headliner will be the Fed Chair himself who speaks from Dallas on Thursday Afternoon.

As for corporate earnings results, we do not have the sheer numbers that we have seen in recent weeks, but we will hear from a number of headline level firms. The notables include Home Depot HD on Tuesday morning, followed by RocketLab USA RKLB and Spotify SPOT on Tuesday evening. Wednesday will open with Shopify SHOP and close with Cisco Systems CSCO, while the Walt Disney Company DIS reports on Thursday morning and Alibaba BABA reports on Friday morning.

What Else? The Fed

- Minneapolis Fed Pres. Neel Kashkari spoke on Saturday. Kashkari talked about the longer end of the yield curve. He said, "As we've been cutting rates over the past couple of months, a lot of people have focused on the fact that long-term Treasury yields have gone up. Some people have speculated it is expectations about what a new administration might do, we'll see what the new administration does or what Congress does. Another possible explanation is that we're just in a higher productivity, higher growth environment. And in a higher productivity, higher growth environment, all else equal, I would expect higher interest rates to go along with that." Minneapolis does not vote on policy until 2026.

Economics (All Times Eastern)

No releases of significant domestic macroeconomic data scheduled.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: ARMK (.53), MNDY (.63)

At the time of publication, Guilfoyle was long XLU, RKLB.