Outage Uh Oh, Trading Microsoft, CrowdStrike, Market Beat-Down, Netflix

Has the worm turned? After Thursday's 'ugly stock' the S&P 500 and Nasdaq Composite have moved into a much more precarious position, while I'm watching cybersecurity.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Uh oh.

Major airlines around the planet have grounded flights early on Friday morning, while banks in Australia, Sky News in the U.K. and the London Stock Exchange have all had issues. Additionally, large numbers of people have been having problems with Microsoft's MSFT 365 suite of apps and its Azure cloud computing platform.

Cybersecurity leader CrowdStrike CRWD has told the media that at least some of these issues and crashes are related to issues with its Falcon Sensor. Even some of the platforms and services that I rely upon to do my job are not working correctly.

For its part, Microsoft has announced that Azure service has been at least partially restored, while it appears that CrowdStrike is still having significant problems as I work my way through the zero-dark hours Friday morning. Though the opening bell in New York is still several hours away, I would expect the problem or these problems to impact equity performance at least in the early going. At this overnight hour, I see CrowdStrike shares trading 14% lower than where they closed Thursday afternoon, and I see Microsoft shares down 2.5%.

Yes, these are both Sarge names. MSFT is my book's most heavily weighted long position. As readers know, CRWD had become my most heavily weighted long position after its first-quarter earnings pop, and I had been working to right-size that position ever since. I had gotten myself about halfway there, selling a tranche at $370 last week and another at $354 and change earlier this week. It looks as if the share price will finish that job for me as I currently see CRWD trading with a $287 handle.

At overnight prices, CRWD is my sixth heaviest weighted long position and stands an eyelash away from falling into eighth place. Notably, other cybersecurity stocks are trading higher at this hour. I don't know just how damaging this news is, and how badly CrowdStrike's reputation is damaged. Therefore, I cannot tell you if I plan to buy this dip as of yet. I can tell you that I plan to make no changes this morning to the size of my MSFT long. I am watching Zscaler ZS, Palo Alto networks PANW and SentinelOne S this morning as this news develops.

The Ugly Stick

The "stick" was out hunting again on Thursday as both the S&P 500 (-0.78%) and the Nasdaq Composite (-0.7%) helped paint the tape red for a second consecutive trading day. It was the first time in a month that the two major U.S. equity indexes posted back-to-back losing sessions. No, this time, the selloff was not part of a rotation, but more of a broad market beat-down.

The mid-majors were all slapped around to a greater degree than were those two indexes. The Russell 2000 and S&P 600 were pasted for losses of 1.85% and 1.49% as there was to be no salvation found in the small-caps. The Dow Transports were beaten for 1.77%, while the KBW Banks were drilled for 1.87%.

Oddly, while tech sold off to some degree, not all of tech sold off. The S&P Technology SPDR ETF XLK closed very close to unchanged, but "up" just a smidge. While within tech, the Dow Jones U.S. Software Index did close down 1.04%, the Dow Jones U.S. Semiconductor Index closed up 1.64% and the Philadelphia Semiconductor Index closed up 0.51%. The group bounced back just a bit, led higher by Broadcom AVGO, and Nvidia NVDA as those two names posted Thursday gains of 2.91% and 2.63%, respectively.

Has the Worm Turned?

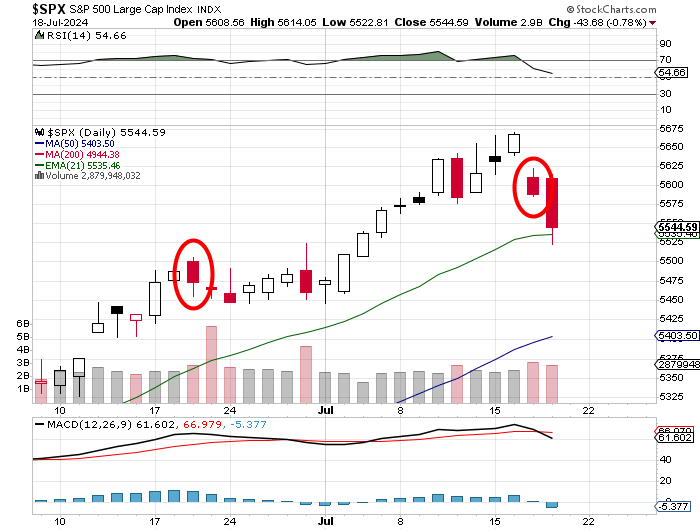

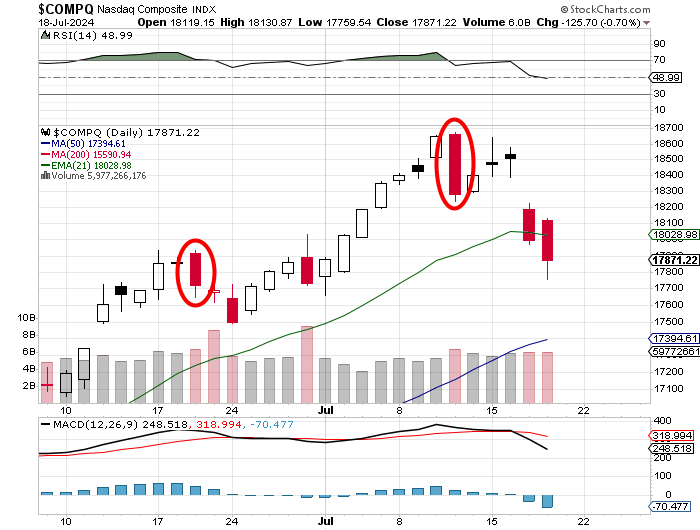

Adding a day to the two charts that I showed you on Thursday morning, readers will see that both the S&P 500 and Nasdaq Composite have moved into a much more precarious position:

On Thursday, the S&P 500 tested, but held its 21-day exponential moving average (EMA). That said, this week, the S&P's Relative Strength has moved from technically overbought territory to something far more neutral as the Moving Average Convergence Divergence (MACD) has gone sour for this index.

The 12-day EMA has crossed below the 26-day EMA as the histogram of the 9-day EMA has fallen into negative territory... all as that change in trend had not really been truly confirmed on Wednesday.

As mentioned on Thursday morning, there was such confirmation for the Nasdaq Composite on Wednesday, while Relative Strength moved from "overbought" to neutral and as the daily MACD suffered that same bearish cross-under and the 9-day EMA provided that same sub-zero reading through its histogram. This index did, however, surrender its 21-day EMA without much of a fight.

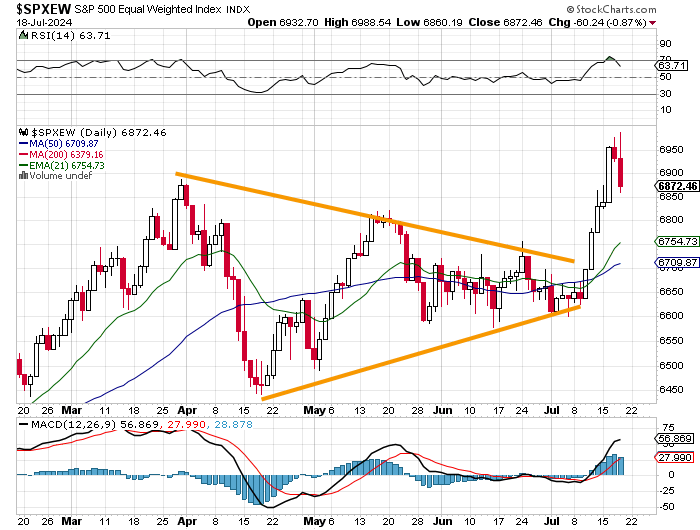

Now this... the equal-weighted S&P 500 has not only given up its "overbought" RSI reading but has also posted two straight red candle days after breaking out from a symmetrical triangle pattern. The RSI here is still better than neutral and the daily MACD is still very bullishly postured. The 12-day EMA stands well above that 26-day EMA and the histogram of the 9-day EMA is still far above zero.

What now, for the broader large-cap market? Where to, for the unwashed 493? It depends on what happens next. Does that two-day selloff start to base (consolidate, allowing its moving averages to catch up)? That could be either positive or negative. Instead of basing, this still could be the start of a bull flag. That would be more of a positive for the unblessed. We cannot arrive at a conclusive answer to that question just yet.

Thursday

Nine of the 11 S&P Sector SPDR ETFs closed in the red on Thursday, with Health Care XLV catching the most severe beating at -2.27%. The Financials XLF and Discretionaries XLY also surrendered more than a full percentage point. With Tech closing virtually unchanged, only Energy XLE gained any ground at all, and it wasn't much, just 0.18%.

Losers beat winners at the NYSE by roughly 10 to 3 and at the Nasdaq by about 7 to 2. Advancing volume took just a 23.2% share of NYSE-listed trade and a more respectable 35.1% of composite Nasdaq-listed volume. The one bright spot was that aggregate trade contracted on a day-over-day basis across the listings of both exchanges as well as across the memberships of both the S&P 500 and Nasdaq Composite.

What Are You Really Saying?

A number of Fed officials were out and about on Thursday. San Francisco Fed Pres. Mary Daly, who does vote on policy this year, said what I think we're all thinking. On potential rate cuts, she said... "We don't have price stability right now and we need to be very confident that we're on a sustainable path to achieve it." Daly added... "We're at this point of inflection, where additional slowing in the labor market could — it's not a guarantee — but could cause additional increases in the unemployment rate." That was not what struck me on Thursday.

At a conference in Dallas, both Fed Governor Michelle Bowman and Dallas Fed Pres, Laurie Logan opined on funding and liquidity. Bowman stated... "When it comes to the next steps in liquidity reform, I think it is imperative that we tackle known and identified issues that were exposed during the banking stress in the spring of 2023. Logan said... "Our last full review of the discount window function took place more than 20 years ago. By examining our approach to discount window lending in the current environment and in light of recent experience, we can ensure the window continues to provide ready access to liquidity going forward."

Problem? Not yet anyway.

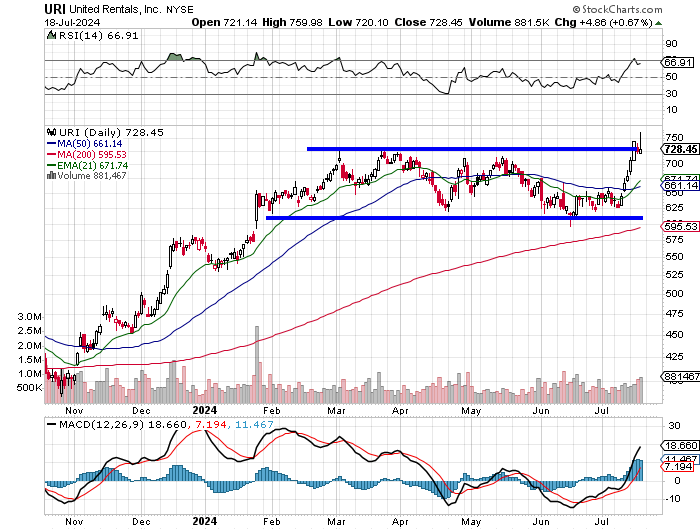

Breakout?

United Rentals URI tried anyway. The stock closed up 0.67% for the day on Thursday, but 4.2% below its high of the day. That said, the stock is still up 16.1% since July 9.

Readers will see that URI tried and failed to break out from a more than five-month-long basing period of consolidation on Thursday. The daily Moving Average Convergence Divergence (MACD) is still very muscular, while Relative Strength is strong but not too strong.

There is room for a second attempt at cracking or taking and holding the $732 pivot. Taking that level could open the door to prices as high as $840. Conversely, a fourth failure here in as many days and a seventh failure here over five months could send the shares back towards its key moving averages.

All Hail Netflix?

Great quarter for Netflix NFLX. Solid beat on paid memberships. Guidance seemed okay too. Yet the shares are trading slightly lower overnight.

At least Cobra Kai is back. That's the only show I watch on the service.

Economics (All Times Eastern)

13:00 - Baker Hughes Total Rig Count (Weekly): Last 584.

13:00 - Baker Hughes Oil Rig Count (Weekly): Last 478.

The Fed (All Times Eastern)

10:40 - Speaker: New York Fed Pres. John Williams.

13:00 - Speaker: Atlanta Fed Pres. Raphael Bostic.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: AXP (3.25), CMA (1.19), HAL (0.80), SLB (0.83), TRV (2.16)

At the time of publication, Guilfoyle was long MSFT, CRWD, S equity.