Inflated Hopes for Retailers?

As we kick off Cyber Monday, let's look at those Black Friday shopping numbers -- but watch out for inflation distortions. Also, the 'buck' stops here with the Donald as he threatens BRICS.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Good morning. Happy Monday. If it seems like the weekend went by like a shot, that's because it sort of did. One thing most of your dinner guests probably did not "get" last Thursday, as they made plans to go shopping, or simply hunker down on their mobile devices and computers in search of holiday deals on Friday, was that financial markets were not closed on Friday. The half-day Friday trading session on Wall Street has historically been exactly the opposite of what many outside of the business might expect. It had been the one day where trading can go so awry that the higher up on the food chain one is, the more likely he or she was to be at work that day.

We've had some odd "Black Fridays" on Wall Street over the years. Due to the occasional quirkiness, but usually light trading volume, the day was the one holiday-related lighter trading session, where the decision makers often felt the need to be at the wheel and would let the junior people take the four-day holiday weekend. Strange as it was, it became almost a professional insult back in the 1980s and 1990s to be "given" the day off and almost a vote of professional confidence to be needed on that day. I am sure that the domination of algorithmic trading over professional traders over the past couple of decades has reduced that distinction, but it was one that I always found somewhat paradoxical in nature.

Regardless, there will be no such difficult staffing decisions to make this week or any of the next few weeks as this is "Cyber Monday" and this year Cyber Monday kicks off the first of three consecutive five-day, full-day workweeks. Ah, the glories of sell-side traders and sales traders avoiding anything that endangers their perceived year-end bonus will be offset by a rush of tax-loss harvesting that could possibly render December's monthly results somewhat deceptive. That is at least until we get to the traditional "Santa Claus Rally" period, which for the new kids, is just from Dec. 24 (last five trading sessions of the outgoing year) through Jan. 3 (first two trading sessions of the new year).

Black Friday

So, how did U.S. retailers do on Black Friday? The season is apparently off to a rather decent start, especially if one is more of an e-commerce retailer and less of a brick-and-mortar retailer. This is a shift in consumer behavior that has now been many years in the making and seems to only be accelerating.

According to sales data and estimates provided by Mastercard, sales at physical retail locations saw year-over-year Black Friday growth of just 0.7%, while Mastercard's SpendingPulse service showed e-commerce sales for the day up a whopping 14.6% year over year. Those headline numbers were not adjusted for inflation. Facteus, which is also a transaction data tracking service, showed online sales up 11.1% from the year ago comparison, while physical sales were actually down 5.4%. That's right, down. In real terms, meaning once adjusted for inflation, the Facteus numbers show online sales growth of 8.5% and physical retail sales that contracted a tough to look at 8%.

Those e-commerce sales in dollar terms, according to Adobe Analytics, reached $10.8 billion, which would be good for year-over-year growth of 10.2%. Three tracking services, three different numbers? Get used to it. Ever watch ADP or the Bureau of Labor Statistics try to measure monthly job creation? Or the EIA and API try to measure weekly oil inventories? Sticking with Adobe Analytics, between 10 a.m. and 2 p.m. on Friday, U.S. consumers, who executed 52.8% of their total Black Friday purchases online, averaged spending $11.3 million per minute over those four hours. Globally, according to data provided by Salesforce CRM, online Black Friday e-commerce was up 5% to $74.4 billion.

Does that mean that the rest of the world now celebrates Thanksgiving or a Thanksgiving-like holiday on the same day as the U.S.? No. That said, it does mean that the rest of the world is learning to at least hunt for online discounts in line with the American calendar.

Before I leave this topic behind. According to Facteus, neither Best Buy BBY nor Target TGT saw much year over year growth in e-commerce sales this year, while Amazon AMZN and Walmart WMT apparently did quite well online.

December Seasonality

Over the past 60 years (since 1964), the S&P 500 has closed the month of December up an average of 1.3%, which is the third best month for the index behind April and November. Those two months are up an average of 1.6% and 1.5% respectively over that same time frame. December has closed higher 72% of the time over those 60 years. This level of consistently positive monthly finishes puts December in second place to April, which has been up 73% of the time over those 60 years.

The Zero-Dark Hours

U.S. equity index futures are trading modestly lower through the very early hours on Monday morning with European markets in response to Pres. Elect Donald Trump's post on social media over the weekend regarding the possibility of a BRICS-related new currency. Readers will recall that this is a concern that I warned about in the recent past. The move away from the U.S. dollar in international trade and the reduction of the portion of global reserves held in still dominant U.S. dollars is, in my opinion, something to worry about going forward.

It is because the U.S. dollar had become the currency of international trade and because the dollar had become the world's top reserve currency that the U.S. has been able to "export" much of its inflation over these past few tough years. That dominant position has been threatened, in particular by the BRICS who gather every once in a while, and discuss settling international transactions in their own currencies, in gold, or eventually in something new.

The "Donald" posted that he would need "a commitment" from the BRICS nations (China, Russia, Brazil, India, South Africa & others) that "they will neither create a new BRICS currency, nor back any other currency to replace the mighty U.S. Dollar..." The president elect suggests that these nations could face 100% tariffs. The U.S. Dollar Index is 0.6% higher this morning.

The Week That Was

Of course, the holiday-reduced (because you cannot really call it shortened) week that ended this past Friday, was not just about Thanksgiving and Black Friday. The three-and-a-half-day workweek with Thursday off produced trading volumes that scored on Monday and withered significantly on a day-by-day basis over the balance of the period.

What macroeconomic data there was to be released last week, was largely released on Tuesday and Wednesday. October Durable Goods disappointed, as October PCE and Core PCE consumer level inflation showed the same acceleration from September into October that the CPI data had shown a couple of weeks ago.

The rest of the week was all about Pres. Elect Donald Trump threatening to increase tariffs on Mexican, Canadian and Chinese imports as a means toward getting these nations to help the U.S. defend against the illegal import of both criminal elements and narcotics. On top of that, cryptocurrency traders wrestled with the $100,000 per token level for Bitcoin and the war between Russia and Ukraine appeared to increase in hostility as both sides raced to be in a stronger position to negotiate by Inauguration Day in the US.

As for the major to mid-major U.S. equity indexes last week....

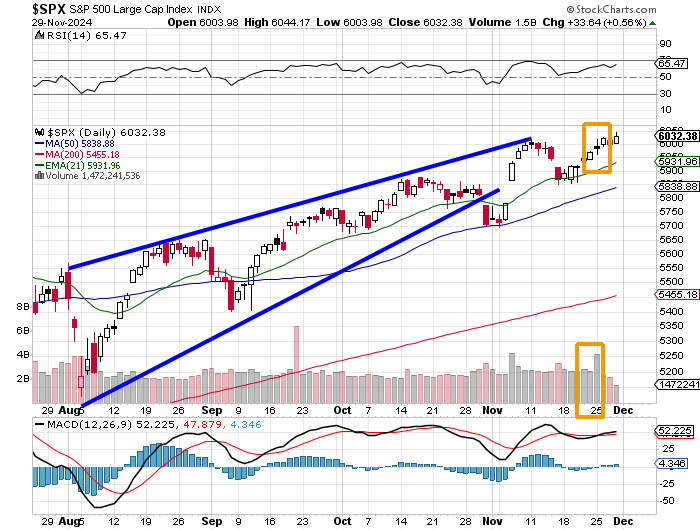

- The S&P 500 gained 0.56% on Friday to close the week up 1.06%.

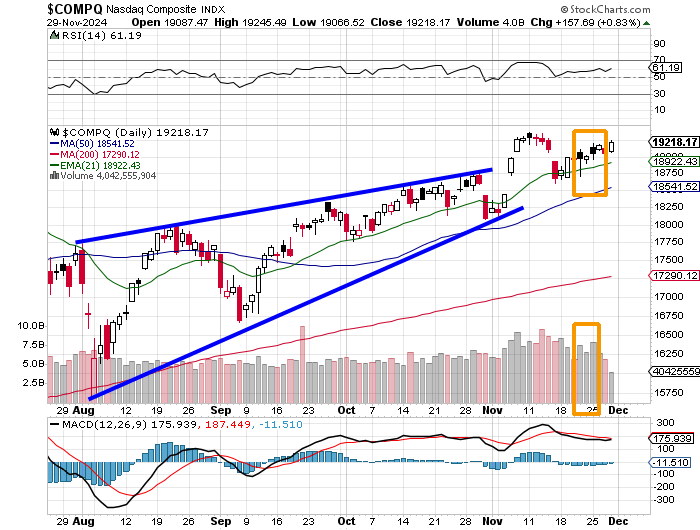

- The Nasdaq Composite gained 0.83% on Friday to close the week up 1.13%.

- The Nasdaq 100 gained 0.9% on Friday to close the week up 0.74%.

- The Russell 2000 gained 1.8% on Friday, to close the week up 1.17%.

- The S&P Small Cap 600 gained 0.16% on Friday to close the week up 1.01%.

- The S&P Mid Cap 400 gained 0.07% on Friday, closing the week up 0.73%.

- The Dow Transports gained 0.05% on Friday to close the week up just 1.45%.

- The Philly Semiconductors gained 1.52% on Friday, but still closed the week down 0.59%.

- The KBW Bank Index gave up 0.09% on Friday, still closing the week up 0.54%.

On Friday, ten of the 11 S&P sector SPDR exchange-traded funds closed in the green, with the Discretionaries (XLY) out in front at +1.03%. The REITs (XLRE) were the only fund among the eleven to close lower at -0.46%.

For the week as well, ten of the eleven S&P sector SPDR ETFs closed in the green as Health Care XLV and the REITs each gained more than 2%. Only Energy XLE closed out the week in the red at -1.79%. Interestingly, for the week, four of the top five performing sector funds would be what you would call defensive in nature.

Speaking of Bitcoin...

I see the world's most famous cryptocurrency still flirting with taking that $100,000 level after trading above $98,652 last week and below $91,000. This morning, Bitcoin is trading 1.6% lower, with a $95,000 handle.

The GDP Game

Last week, the Atlanta Fed revised their GDPNow model for the fourth quarter up to growth of 2.7%, up from 2.6% (q/q, SAAR). Among other central banks running close to real-time GDP models for the current quarter, the New York Fed cut its estimate for Q4 growth to 1.81% from 1.91%, while the Cleveland Fed still sees Q4 growth of 1.84%. The St. Louis Fed has now revised their model for Q4 GDP growth down to 1.31% from growth of 1.55%. The Atlanta Fed's model currently appears to be significantly out of sync with the other three regional Fed models that are all significantly less optimistic.

Charts

I showed you the chart of the Nasdaq Composite below that reflected the upward movement on elevated volume that constituted for me a "day one" followed two days later (last Monday) by a high-volume confirmation of trend. Both the S&P 500 and Nasdaq Composite are in the same position right now, at least technically.

Readers will see that the S&P 500 closed out the week on strength after suffering a down day on Wednesday, but that after Monday, the trading volume rendered the action considerably less meaningful. Currently, both Relative Strength and the daily Moving Average Convergence Divergence indicator of the S&P 500 are postured quite bullishly.

While the moves described above are clearly more distinct for the Nasdaq Composite, both the reading for Relative Strength as well as the daily MACD are postured less bullishly than these indicators are for the S&P 500.

The Week Ahead

Investors can at least look forward to a full workweek over the five days ahead. They can also look forward to a full slate of fed speakers after that group largely took last week off. There will be Fed officials making scheduled public appearances every single day of the week, headlined by Fed Chair Jerome Powell and the release of the Beige Book, both on Wednesday.

Keep in mind that the FOMC will go into their media blackout period this weekend ahead of the Dec. 18 policy decision. Fed Funds futures trading in Chicago are currently pricing in a 65% probability for a quarter-percentage point rate cut at that meeting.

As far as coming macroeconomic data is concerned, this week's key event will be the release of the BLS November Employment Survey data on Friday morning. Before we get there, we will have to run through the ISM Manufacturing and Service sector PMIs on Monday and Wednesday respectively. We'll also hear October JOLTs data on Tuesday, the November ADP Employment Report on Wednesday and the advance release of the University of Michigan's December Consumer Sentiment survey on Friday after the jobs numbers.

Third-quarter earnings season is just about done, but we do have a few stragglers still coming in, primarily among the retailers and some tech names. Tonight, we'll hear from Zscaler ZS and then on Tuesday from Marvell Technology MRVL and Salesforce. After that, on Wednesday morning, Campbell's Soup CPB, Chewy CHWY, Dollar Tree DLTR, and Foot Locker FL all report, followed by American Eagle Outfitters AEO Five Below FIVE and SentinelOne S on Wednesday afternoon.

Thursday morning brings results from Dollar General DG and Signet Jewelers SIG. This will be followed by DocuSign DOCU, Lululemon Athletica LULU and Ulta Beauty ULTA on Thursday evening.

What Else?

- Still nothing to report on the Juan Soto front.

- Michigan surprisingly defeated heavily favored Ohio State at Ohio State on Saturday, though I'm not sure who won the post-game rumble.

- Army plays host to Tulane this Friday night in the American Athletic Conference championship game.

- The Jets still stink.

Economics (All Times Eastern)

09:45 - S&P Global Manufacturing PMI (Nov-F): Flashed 48.8.

10:00 - ISM Manufacturing Index (Nov): Expecting 47.6, Last 46.5.

10:00 - Construction Spending (Oct): Expecting 0.2% m/m, Last 0.1% m/m.

The Fed (All Times Eastern)

15:15 - Speaker: Reserve Board Gov. Christopher Waller.

16:30 - Speaker: New York Fed Pres. John Williams.

Today's Earnings Highlights (Consensus EPS Expectations)

After the Close: ZS (.63)

At the time of publication, Guilfoyle was long AMZN, WMT, S equity.