How the Case for Cash Adds Up (And When It Doesn’t)

As zero interest rates have become a thing of the past, has your strategy caught up?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

“Cash is king.”

But also:

“Cash is a portfolio drag.”

Which is it?

The answer is both, actually. But which one applies to you depends on something your financial plan probably isn’t tracking.

If you’re still working but within a decade of retirement, your plan was built for accumulation, and it may be leaving you in a bad position right when it matters most.

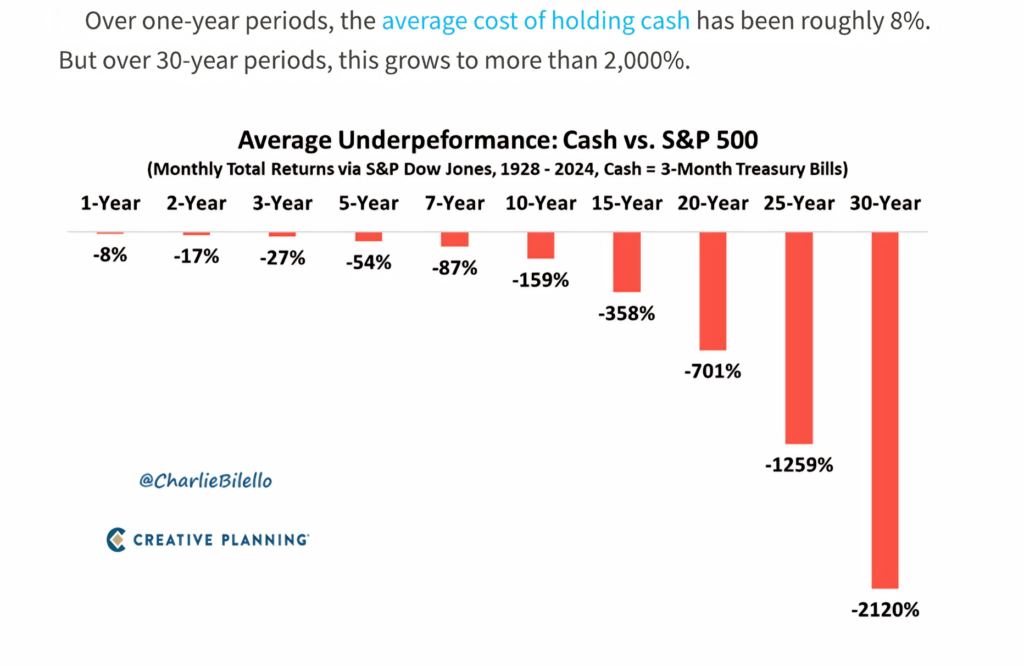

The conventional wisdom that cash kills long-term returns is correct over a 30-year horizon. That’s true, as a chart from Charlie Bilello at Creative Planning shows how over periods of one year, the average cost of holding cash is about 8%, but over periods of three decades, it can grow to more than 2,000%. Bilello shows that after five years, the cost is around 54% and by 15 years, 358%.

You can see how the math for your cash holding shifts over time, and becomes more dramatic as you approach retirement and begin drawing income.

That’s when cash stops being a drag and starts being a decision. A bad year in the market when you’re still working means the opportunity to buy more at lower prices.

A bad year in the market when you’re drawing income means you sell more at lower prices. Same event, opposite outcome. The difference is whether you have a paycheck and whether you’ve used it to build a cushion before you need one.

Why Working Investors Are Well Positioned

If you’re still working and salting away money from your paycheck, building a one-to-two year cash buffer costs you almost nothing in real terms. It’s just a redirection of a portion of your savings over a few years, or a designated chunk each year.

But doing it after you retire, when the portfolio may be your only source of income, means selling assets to create that buffer. Then think about doing that in a down market: This would defeat the purpose entirely.

The Returns: What Cash Costs You

For a 35-year-old with 30 years of runway, too much cash is a legit problem. As Bilello’s data makes that clear: Over three decades, the average opportunity cost of sitting in cash instead of equities grows to more than 2,000%. Every dollar parked on the sidelines is a dollar not compounding.

But compress that horizon: At 58, with seven years to retirement, you’re not optimizing for 30-year compounding anymore. You’re optimizing for not being forced to sell equities at the wrong time.

Those are different problems that require different approaches.

How the Math Works

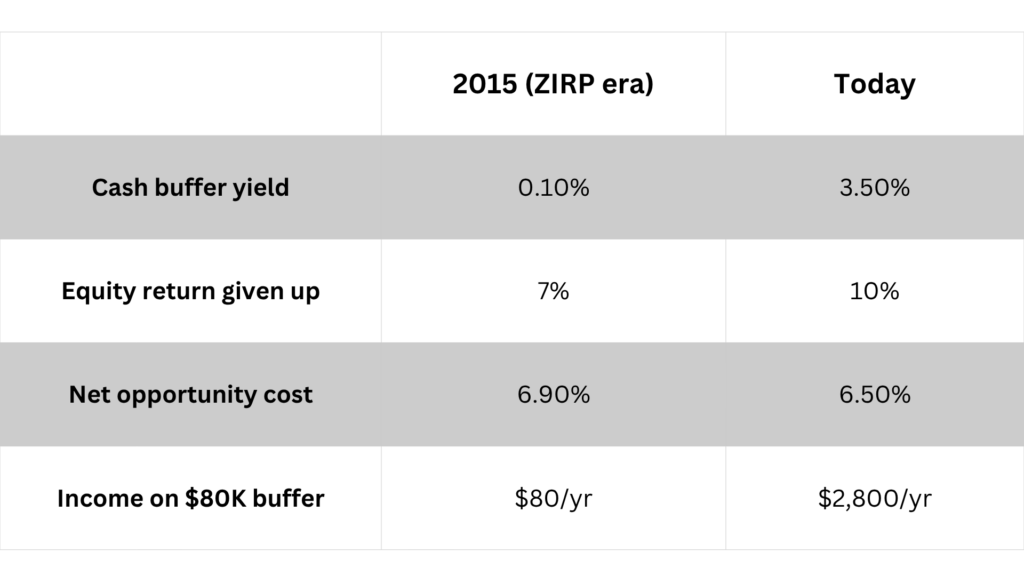

Here’s the math that sometimes gets missed: Money market funds and short-term Treasuries are no longer yielding something in the neighborhood of zero, like they were about 10 or 11 years ago. For example, the six-month Treasury yield was still at 3.69% as of mid-April 2026.

That’s not an equity-like return, but it is something, and it changes the cost of holding a cash buffer. Now the prospect of holding cash makes more sense for someone near retirement.

For example, say you hold $80,000 in a money market fund. That’s a reasonable two-year spending reserve for someone with $60,000 in annual retirement expenses after Social Security. A 3.5% money market return generates about $2,800 a year.

The drag on the broader portfolio is real but narrow. And it looked very different in 2015, when money market funds yielded near zero and the same buffer cost you 7% in equity return opportunity cost and gave you almost nothing back.

Here’s a comparison of those rates from 2015 versus today.

The equity return you’re giving up is higher today than in 2015, but the cash yield has risen so much more that the net cost of holding the buffer is actually lower.

For me, this is a useful comparison, as I find that many investors get anchored on specific conditions from the past that no longer apply.

What About the Middle Years?

If you’re in your mid-40s or early 50s, you’re not in the danger zone yet, but you’re not in pure accumulation mode either.

This is the right time to start thinking about cash not as a permanent allocation, but as a building project. A small, deliberate redirect of savings now, even $500 a month into a high-yield savings account or money market fund, will start constructing the buffer well ahead of the time when you’ll need it. If you do this, it comes at the lowest possible cost to you.

The math of compounding works against large cash positions over long horizons. But the math of preparation works strongly in favor of starting early.

At the time of publication, Stalter had no position in any security mentioned.