The Fed Must Cut 50 BPS, Even if it Signals Panic

The market is anticipating a 25 BPS interest rate cut next week, but that won't be enough to get ahead of the economy.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

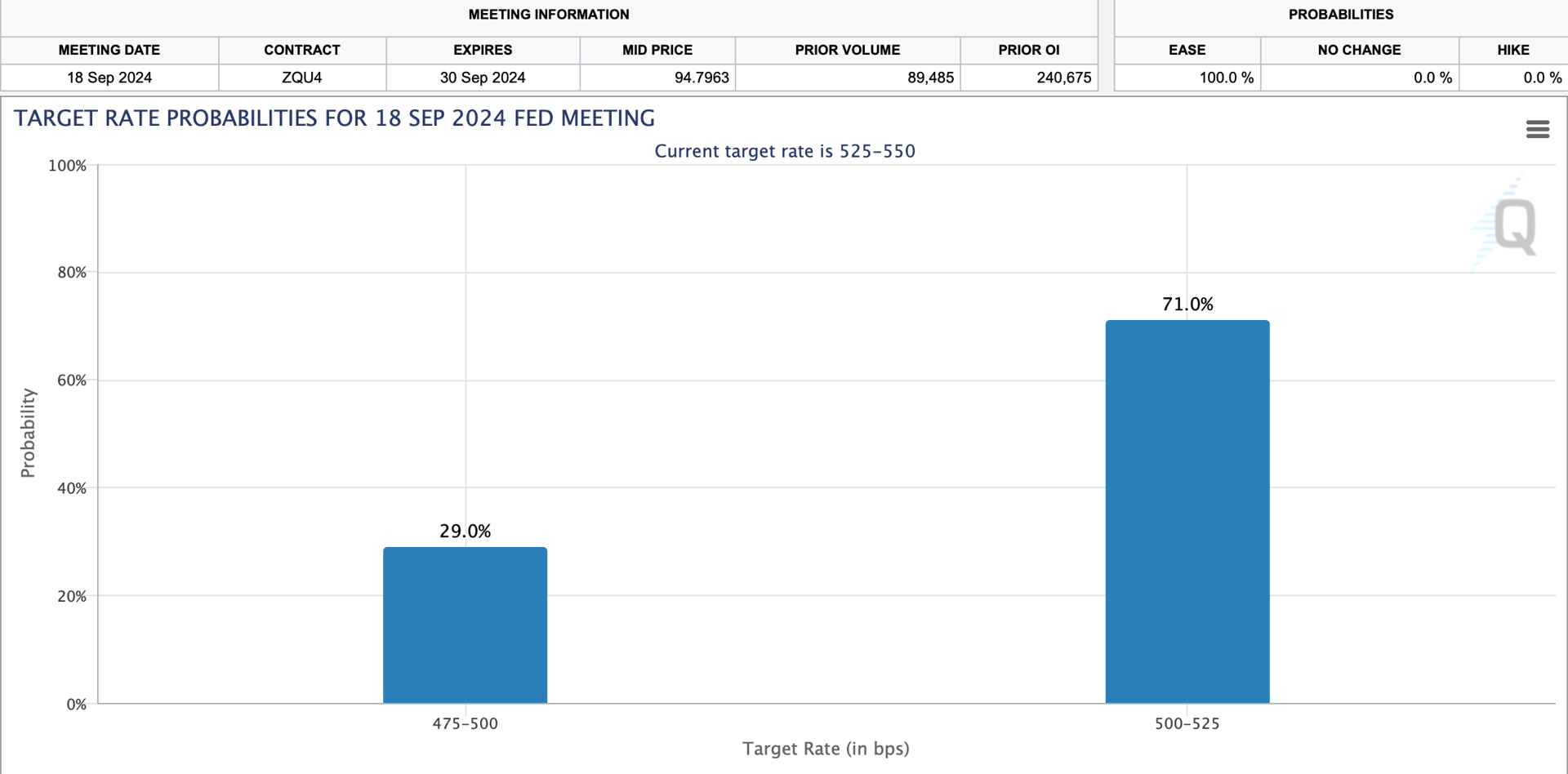

It’s a given that the U.S. Federal Reserve will cut interest rates next week. The only uncertainty is by how much.

According to the CME’s FedWatch Tool, the odds of a 25 basis point rate cut are 71%, while the chance of a more aggressive 50 basis point decrease stand at 29%.

Message to the Market

The Fed must consider how markets will react to the central bank’s next move. A reduction of 25 basis points sends the message that everything is unfolding according to plan. A cycle of rate hikes has slowed the economy and moderated inflation to the point where a soft landing is now achievable. Therefore, a modest rate cut is appropriate.

A 50 basis point cut would signal something else entirely. It would serve as an admission by the Fed that it waited too long to cut rates, and now it’s playing catch-up. An outsized rate cut can cause unease among investors, because it creates the impression that, despite reams of rhetoric, the Fed has once again mishandled the economy.

A Checkered History

The Fed doesn’t have the best track record when it comes to predictions. In early 2007, Fed Chairman Ben Bernanke made statements to the effect that a growing crisis in the subprime mortgage market was contained.

By the end of 2008, Bernanke and the FOMC would cut rates a total of 10 times, for a total of 525 basis points. That includes three cuts of 25 basis points each, four cuts of 50 basis points, two 75 basis point reductions and one mammoth reduction of 100 basis points on December 16, 2008.

More recently, former Fed Chairman and current Treasury Secretary Janet Yellen made a similarly egregious error, when she described inflation as “transitory” in 2021. That term was echoed by current Fed Chairman Jerome Powell and various other Fed officials.

This error helped bring about the worst bout of CPI inflation in over 40 years. Three years later, inflation has modified, but consumer prices are still rising faster than the Fed’s stated annual goal of 2%.

Jobs, Jobs, Jobs

As the FedWatch tool currently predicts, a move of 25 basis points is the most likely scenario when the Fed makes its next move on September 18.

However, a strong case can be made for a 50 basis point cut. That’s because U.S. job creation is weaker than it appears.

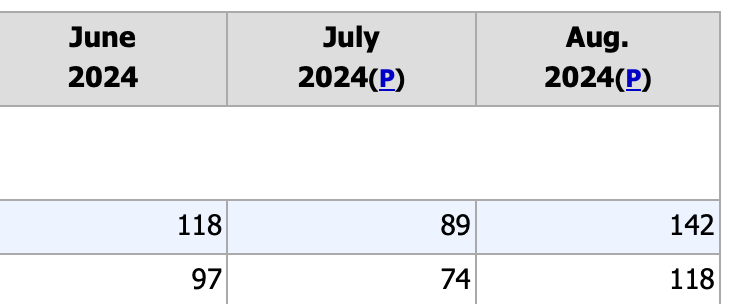

The headline figures for U.S. non-farm payrolls in June, July and August (top line) showed job creation at a three-month average of about 116,300.

This figure is misleading, because it contains government jobs. Government jobs should not be included in this calculation, because they are not created by the private sector.

If we strip out government jobs and focus on the private sector alone (bottom line), the three-month average falls to 96,300 — a reduction of 20,000 jobs per month over the past three months.

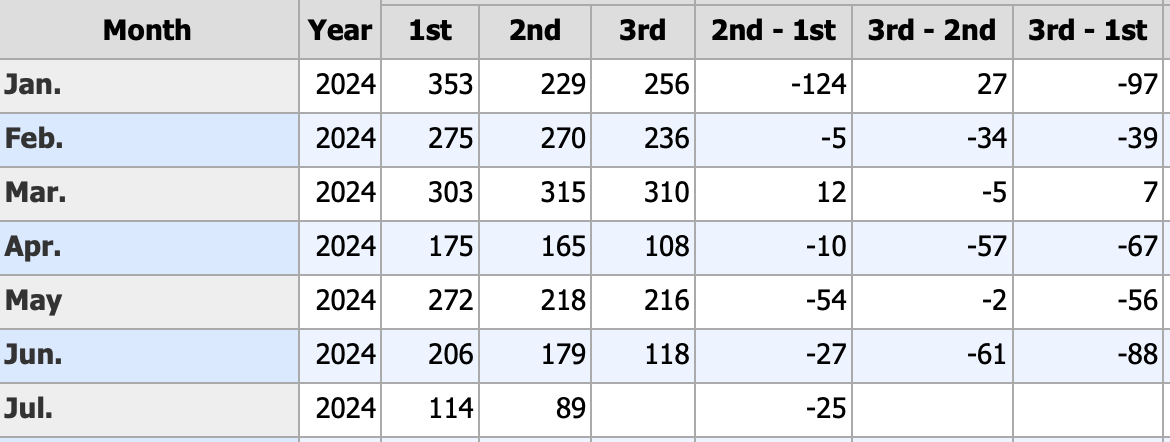

Add to this the fact that in recent months, the monthly employment figures from the Bureau of Labor Statistics have consistently overstated the strength of the U.S. job market. Over the first seven months of this year, BLS job creation figures were revised lower by a total of 365,000 jobs.

The Fed’s Next Move

The FOMC is likely to cut by 25 basis points on September 18. This creates the illusion that the Fed’s projections are playing out in an orderly fashion.

However, it won’t be enough. The Fed should make a deeper cut. A 50 basis point rate cut would be appropriate, accompanied by a statement that further cuts are on the table.

The job market in the first half of this year was never as good as BLS statistics implied. Now, the illusion of strength created by overstated non-farm payroll figures has all but disappeared.

The last thing the FOMC wants to convey is a hint of panic, and a 50 basis point move could be perceived that way. However, a larger-than-expected cut would also project the message that the Fed, which has so often been behind the curve, is for once ahead of the game.

At the time of publication, Ponsi had no positions in any securities mentioned.