Estee Lauder Turns Heads (But Not in a Good Way)

The cosmetics giant looks good at first glance and then its guidance inspires fear. Should you buy the dip or run?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The shares of Estee Lauder EL have been mired in "beat-down mode" really since very early 2022. The company posted its fiscal fourth-quarter earnings on Monday morning, and as some may have expected, the shares are now trading lower. Quite interestingly, ahead of the report, CEO Fabrizio Freda said he would retire at the end of fiscal 2025, after spending the past 16 years at Estee.

Freda will lead until a successor is named and once that happens, will partner with that new leader to ensure a smooth transition. Freda expects to hang on through fiscal 2026 as an adviser. I referred to this news as being interesting because the knee-jerk to the news for the shares was to the upside. That lasted until the results crossed the tape and their warning on demand from China became news.

The Results: Looks Good at First, and Then ...

Estee Lauder posted an adjusted earnings per share of $0.64 (GAAP EPS: $-0.79) on revenue of $3.871 billion. Both the top line and adjusted bottom line numbers beat Wall Street's expectations. The sales print was good enough for year-over-year growth of 7.2%. But the quite sizable adjustment ($582 million or $1.43 per share) was made for impairments relating to the change in fair value mostly for acquisition-related intangible assets.

For the full fiscal year, Estee reported net sales that decreased 2% and a diluted EPS that declined 61%. The poor full-year performance, as stated in the press release, primarily reflected "ongoing softness in overall prestige beauty in mainland China and a decline in Asia travel retail driven by the decrease in the first half of fiscal 2024, reflecting actions taken by the Company and its retailers to reset inventory levels as well as lower conversion."

Operations: It's Kinda Complicated

As net sales increased 7.2% to $3.871 billion, the cost of those sales decreased 6% to $1.093 billion. This left a gross profit of $2.778 billion (+14%), as gross margin expanded from 67.8% to 71.8%. Normal operating expenses (selling, general, administrative) increased 1% to $2.444 billion. Restructuring charges increased from $31 million to $86 million, and then there are the impairments. After all of that, operating expenses including these "one-time" items increased 23% to $3.011 billion. This dropped operating margin from 32.1% to 22.2% and unadjusted operating loss from $5 million down to a loss of $233 million.

After accounting for interest, taxes, and other benefits/losses, net loss attributable to shareholders printed at $284 million, down from a $33 million loss. This works out to an unadjusted loss of $0.79 per diluted share, down from a loss per share of $0.09 for the year-ago comparison.

Guidance That Could Shatter a Mirror

If you are long these shares, you should probably sit down now. Here goes:

- For the current quarter, Estee Lauder is forecasting organic net sales to decrease between 5% and 3% on a year-over-year basis. Unadjusted EPS are projected to land between a loss of $0.09 and flat. Adjusted EPS is seen in between $0.02 and a dime. Wall Street had been looking for about $0.63 for the adjusted EPS number. This guidance is being seen by many as catastrophic.

- For the full year, net sales are seen printing in between a range spanning from -1% to +2% annual growth. This would actually be better than what Wall Street had been expecting, which was for something close to -20%. Unadjusted full-year EPS is seen at $2.52 to $2.76. Once adjusted, EPS is expected to print in between $2.75 and $2.95. Wall Street was looking for roughly $3.96. This guidance missed on adjusted profitability by more than $1 per share. Again, catastrophic.

- On the full year guidance, Estee warns that "Mainland China and Asia travel retail are generally expected to decline on a full-year basis, although assuming gradual improvement in the second half of fiscal 2025."

Foundation Looks OK ... in Dim Lighting

For the full fiscal year, Estee Lauder generated operating cash flow of $2.36 billion. Out of that number came capital spending of $919 million, which left free cash flow of $1.441 billion. That's actually a decent number. Out of this number came $947 million in cash dividend payments to shareholders. The rest went toward the repayment of some of the commercial paper.

Turning to the balance sheet, the company ended the quarter with a cash position of $3.395 billion, and inventories of $2.175 billion, putting current assets at $7.922 billion. Current liabilities add up to $5.702 billion, which includes no short-term debt. That leaves current and quick ratios at 1.39 and 1.01. As poor as the execution has been at this firm, these ratios do pass muster.

Total assets amount to $21.677 billion. This includes no goodwill or any other intangible assets, which we appreciate. Total liabilities less equity comes to $16.363 billion, including $7.267 billion worth of long-term debt. This is not the strongest, most fortress-like balance sheet I have ever seen. Obviously. That said, it is clear that this balance sheet has been professionally managed and is stronger than I would have expected given the performance across the rest of the company.

My Impression: There's Potential, Maybe ...

The fact that the current CEO is leaving is going to be a reason to get long this stock. At some point. Freda hanging around long beyond his handing over the reins of corporate leadership may hang over the company and the new CEO, whomever that might be. Once there is a handoff, we hope, leadership can be passed on resolutely, and the new CEO can set about resurrecting Estee's reputation, and its stock price.

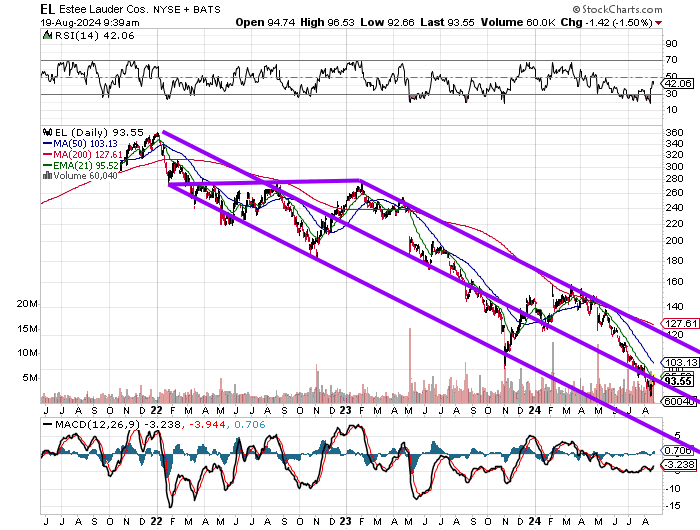

Nice three-year chart, don't you think? Down 75% over that time frame.

Readers will see that the stock is down sharply this year alone. Relative strength is no longer in "oversold" territory, but remains weak. The daily moving average convergence divergence indicator is improving. The 12-day exponential moving average has crossed above the 26-day EMA, which is a positive, but both remain deeply negative, which sort of negates the importance of this crossover. The histogram of the 9-day EMA is above the zero-bound and that should help.

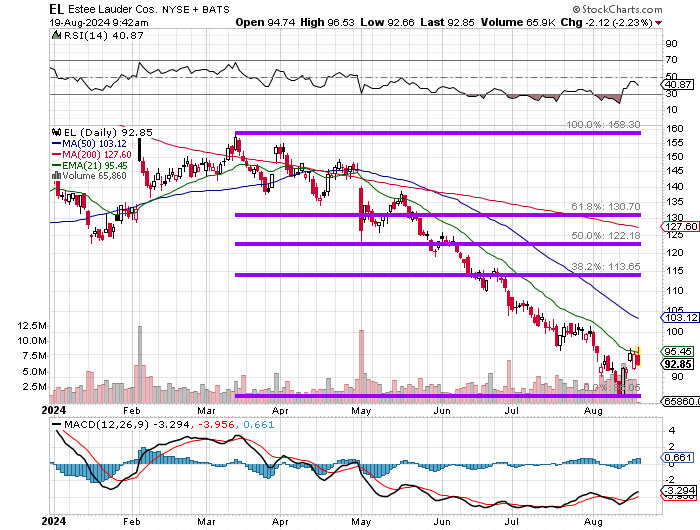

Do I buy this stock here and now? Not a chance. Estee Lauder is going to have to make believe that the company is from Missouri and show us. I think about getting interested only at new lows, or on momentum upon retaking that 50-day simple moving average. In here? The $2.64 in dividend payments over a full year, yielding 2.78% are not enough for me to risk my hard-earned capital of a firm that has done nothing but lose for three years.

At the time of publication, Guilfoyle had no position in any security mentioned.