Doug Kass: When the S&P Seems Too Good to Be True ...

The SPX is now overvalued against interest rates, earnings, cash flow and sales and most other metrics that have stood the test of time.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

When the S&P is this overvalued, it's good to remind oneself: There is no upside without downside, no reward without risk.

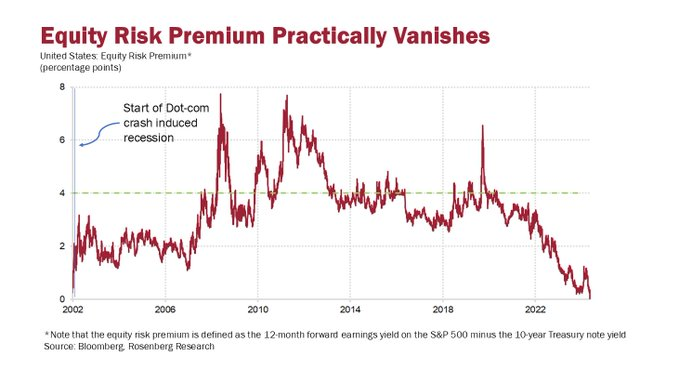

Astonishingly, with the recent rise in interest rates, the equity risk premium is only nine-basis points away from turning negative. This means that investors are now willing to pay to take on equity risk, instead of getting paid. Check out this chart:

Here is a longer-term chart of the S&P earnings yield vs. the yield on the 10-year Treasury note:

As I wrote yesterday:

Bond Market Update ... And Many More Accumulating Concerns

Nov 12, 2024 12:40 PM EST

Equities continue to ignore rising rates — that ascension is conspicuous today:

* The yield on the 1-year Treasury note is +8 bps to 4.394%.

* The yield on the 5-year Treasury note is +12 bps to 4.315%.

* The yield on the 10-year Treasury note is +12 bps to 4.428%.

* The yield on the long bond is +9 bps to 4.572%.

Bottom Line

So we have an overbought on the S&P Oscillator (near 3.5%), a Woodstock-like drug festival in Tesla (TSLA) and Nvidia (NVDA) 0DTE call options, sky-high price-earnings multiples, near universal investor bullishness, evidence that the post-election breadth thrust might be over (look at today's 2-1 negative breadth), (RSP) (equal weighted S&P) -0.86% and (IWM) (Russell Index) -1.67%)... and now bond yields starting to break out to the upside.

What, me worry?

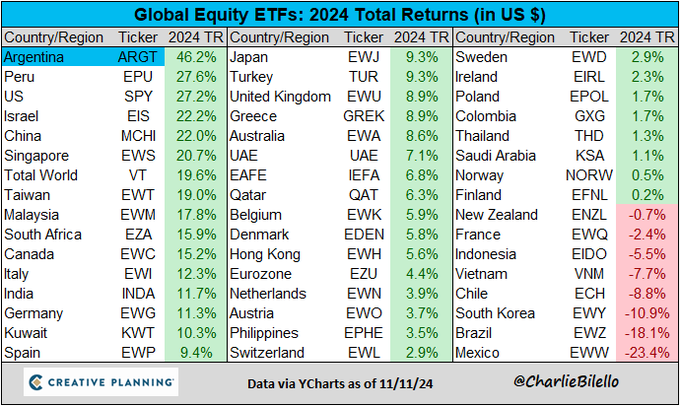

Here, I put into perspective the sharp upside movement in various asset classes since the election - only seven days ago:

As it relates to bitcoin and other crypto currencies it is always important to remember that when we see parabolic moves in asset prices, it is always a good time to remind oneself: There is no upside without downside, no reward without risk.

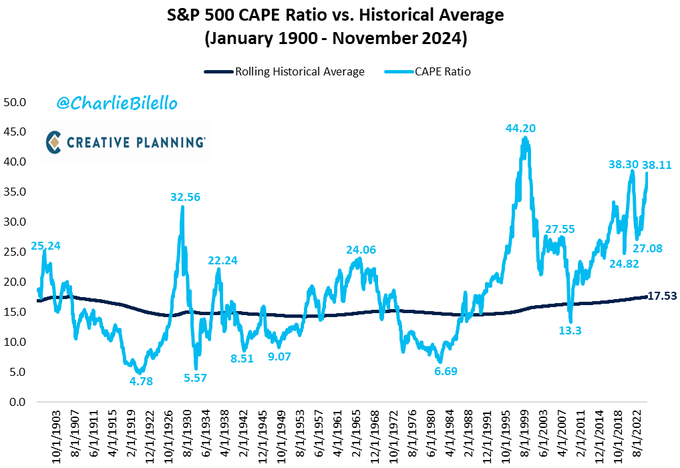

Valuations Appear Inflated

The S&P CAPE Ratio (the cyclically adjusted price-to-earnings ratio) has crossed above 38 for the third time in history and is now higher than 98% of all historical valuations:

Equities, to this observer, are overvalued.