Doug Kass: Be Careful of the Unexpected and Leveraged Corners of Speculation

The four-week market advance should give everyone pause. Let me list the reasons why.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Over history, market inflection points and economic dislocations often come from places not anticipated. Indeed, the most important turning points in markets (and in life) often come at the most unexpected times and in the most unexpected ways.

In particular, leverage, as proven by history, is often uncovered in unexpected places. Think about the collapse of a generally unknown currency, the Thai Bhat, that gripped Asia in 1997 and then spread to other countries (with a ripple effect), raising fears of a financial contagion and a worldwide economic meltdown.

Or the failure of the highly leveraged (and formerly successful) Long Term Capital hedge fund (managed by several Nobel Prize winners in economics) in the following year — which was, in part precipitated by the Russian Debt crisis in 1998 and required a multi billion dollar bailout by 14 banks (orchestrated by The New York Federal Reserve).

But the best example of hidden leverage (where no one was looking) was seen in The Great Financial Crisis of 2007-09 when one overleveraged segment, real estate, proved to be the Achilles Heel for the global economy.

Indeed, what started out as what many believed to be only a few California mortgages under water, multiplied geometrically and almost bankrupted our worldwide financial system — as the layers of leverage were swiftly uncovered and spread rapidly. This market commentary will highlight several significant market (and economic) risks that are not regularly discussed.

The "failure" or combustion of any of these factors could have a most adverse impact on equities and on the domestic economy.

* The U.S. economy has never been more levered to the U.S. stock market. Indeed, one can argue that — with household ownership of equities at an all-time high, with a chorus of "its different this time" and with dreams of a new investing paradigm (of higher valuations) dominating the narrative. As discussed below, it is almost as if the domestic economy is being collateralized by a foundation asset, equities.

From Tom Dyson:

The US stock market is such a foundational asset. You could say, the US stock market has become the collateral that backs the world economy, and all its debt. As long as the stock market keeps rising, everything’ll be okay. But as soon as it turns down, things will start breaking. Employment, real estate values, consumption, trade… and even the government’s finances. It’s the wealth effect, when the stock market is such an important store of wealth. They all rely on a strong stock market to function. The fact that the world’s prosperity has one single point of failure – even as it rises day after day – should terrify you. The market’s function should be to allocate scarce capital efficiently… not collateralise the entire system. In effect, it’s become too big to fail, which is an acute fragility for our capitalist system. As allocators of capital ourselves, how should we approach our investment discipline in a market where expectations (and stock market values) are literally “off the charts”? The bears say "every other time this has happened, there's been a big wreck." The bulls say "this time is different, and besides, the trend is your friend and getting the timing wrong is the same as being wrong."What do you do? Neither position is falsifiable. Which means there is no way to figure out the correct answer with logic… or research… or data. So it comes down to philosophy. Are you a contrarian? Or are you a trend-follower?... The global debt stock surged by over $12 trillion in the first three quarters of 2024 to a record high of nearly $323 trillion. It’s a huge wealth bubble and when it pops, $400 trillion or $500 trillion of (mostly) paper claims ($323 trillion in debt plus whatever owners’ equity the system has) will rush for the exits and seek safety. And policy makers won’t be able to stop it.

* Elon Musk's health and business/innovative successes are critical to a continuation of economic growth and stock market gains. Musk's broad reach — on the road, underground, in space, over the internet, in defense, in artificial intelligence — has now advanced into Washington, and in the formulation and implementation of policy. To have one person so immersed and involved in all these critical areas could pose broad risks — in many ways.

* An extremely leveraged cryptocurrency market represents potential systemic risks. It is my view that cryptocurrency is "the mother of all bubbles" perpetuated by a number of factors (including the rejection of fiat money) and developing digital narratives — many of which have a weak foundation of logic. The absurd notion that the limiting of supply of bitcoin is as stupid as it is damning — as there is no limit to the supply of other cryptocurrencies. To this observer, the sheet market size of bitcoin and other cryptocurrencies is a manifestation of the risks.

See: Crypto Market Cap Charts | CoinGecko

And, as I have written, MicroStratetgy MSTR (with its "math" in expressing the case of buying $1 bills for $3 and MSTR's multiple derivative plays), is the standard bearer of the digital speculation today. See: TheStreet Pro

When the cryptocurrency markets implodes, which is my baseline expectation, the contagion effect will likely be pronounced on all of the capital markets.

* Both fiscal and monetary policy — which is needed to secure the foundation of growth — are travesties. Neither political party has been fiscally responsible — the profligate spending over the last few decades continues apace. (I do not, in any way, buy Elon Musk's objective of cutting $2 trillion from the U.S. budget, as when you go over the numbers only about $1.5 trillion can be cut (and that is if one cut all that was "available" to be cut in total). As well, the Federal Reserve has been guilty of reckless, feckless and fatuous policy in its delayed response to inflation and, then, in effecting a rapid rise in interest rates. I have little confidence in Powell's Fed steering clear of debris in his remaining time at that institution. Nor am I confident in any Fed chairman that might replace him.

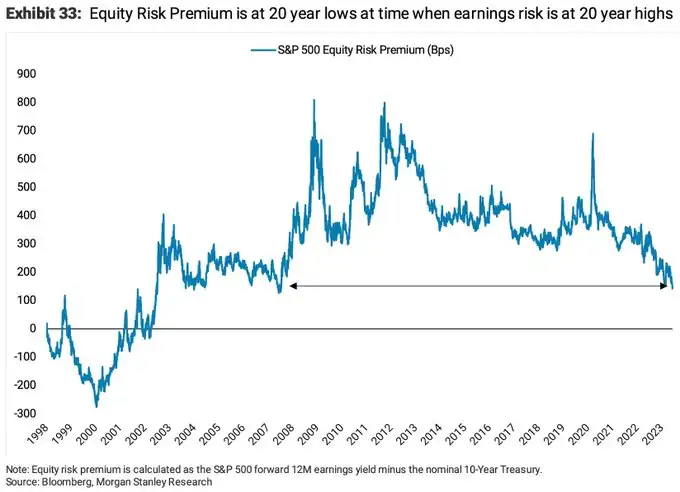

* Changing market structure poses a significant market risk. Passive investing has engulfed the stock market landscape. We are all traders now, on the same side of the boat and worshipping at the altar of price momentum. (See the first bullet point!) Massive inflows into passive strategies and products have been the straw that has stirred the market's drink:

In part, those inflows, have contributed to a near unprecedented narrowing in the equity risk premium (to 20-year lows) while the risk to earnings growth are at 20-year highs:

I can guarantee you (and history has proven) that these inflows — as well as FOMO and the animal spirits — will not be permanent conditions.

Bottom Line

* The entirety of the recent four-week market advance has been based on an expansion in price earnings multiples.

* As narratives multiply and fear/doubt disappear, guards and disciplines are dropped with many asset classes at all-time highs.

* But as asset prices rise, diligence and the assessment of reward vs. risk should take on greater irrelevance — unfortunately just the opposite is occurring.

* And so should the concept of "a margin of safety" be evermore embraced — as it is an essential and integral ingredient to investing over a "market cycle."

* As the late but great Sir Arthur Cashin would often write — in the current euphoria — one should pay strict heed to Bob Farrell's "Lessons of Investing."

* Expect the unexpected...in the corners of leverage and those that are endorsing the narrative of a "new paradigm" (of higher valuations).

The history of speculation is that it resides in areas that are rationalized (with broadening acceptance of a new paradigm).

It is also the condition of history that it is fueled by leverage and lasts longer than most expect. But excesses are never permanent. They become ever more dangerous when markets are consumed with optimism, are no longer fearful and are levered up.

Post Script:

To end today's missive, it is now time to pay heed to Bob Farrell's ten rules of investing (Sir Arthur Cashin would want it this way):

Markets tend to return to the mean over time.

Translation: Trends that get overextended in one direction or another return to their long-term average. Even during a strong uptrend or strong downtrend, prices often move back (revert) to a long-term moving average. The chart below shows the S&P 500 over a 15-year period with a 52-week exponential moving average. The blue arrows show several reversions back to this moving average in both uptrends and downtrends. The indicator window shows the Percent Price Oscillator (1,52,1) reverting back to the zero line.

Excesses in one direction will lead to an opposite excess in the other direction.

Translation: Markets that overshoot on the upside will also overshoot on the downside, kind of like a pendulum. The further it swings to one side, the further it rebounds to the other side. The chart below shows the Nasdaq bubble in 1999 and the Percent Price Oscillator (52,1,1) moving above 40%. This means the Nasdaq was over 40% above its 52-week moving average and way overextended. This excess gave way to a similar excess when the Nasdaq plunged in 2000-2001 and the Percent Price Oscillator moved below -40%.

There are no new eras — excesses are never permanent.

Translation: There will be a hot group of stocks every few years, but speculation fads do not last forever. In fact, over the last 100 years we have seen speculative bubbles involving various stock groups. Autos, radio and electricity powered the roaring 20s. The nifty-fifty powered the bull market in the early 70s. Biotechs bubble up every 10 years or so and there was the dot-com bubble in the late 90s. "This time it is different" is perhaps the most dangerous phrase in investing. As Jesse Livermore puts is:

A lesson I learned early is that there is nothing new in Wall Street. There can't be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again.

Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways.

Translation: Even though a hot group will ultimately revert back to the mean, a strong trend can extend for a long time. Once this trend ends, however, the correction tends to be sharp. The chart below shows the Shanghai Composite ($SSEC) advancing from July 2005 until October 2007. This index was overbought in July 2006, early 2007 and mid 2007, but these levels did not mark a top as the trend extended with a parabolic move.

The public buys the most at the top and the least at the bottom.

Translation: The average individual investor is most bullish at market tops and most bearish at market bottoms. The survey from the American Association of Individual Investors is often cited as a barometer for investor sentiment. In theory, excessively bullish sentiment warns of a market top, while excessively bearish sentiment warns of a market bottom.

Fear and greed are stronger than long-term resolve.

Translation: Don't let emotions cloud your decisions or affect your long-term plan. Plan your trade and trade your plan. Prepare for different scenarios so you will not be taken by surprise with sharp adverse price movement. Sharp declines and losses can increase the fear factor and lead to panic decisions in the heat of battle. Similarly, sharp advances and outsized gains can lead to overconfidence and deviations from the long-term plan. To paraphrase Rudyard Kipling, you will be a much better trader or investor if you can keep your head about you when all about are losing theirs. When the emotions are running high, take a breather, step back and analyze the situation from a greater distance.

Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

Translation: Breadth is important. A rally on narrow breadth indicates limited participation and the chances of failure are above average. The market cannot continue to rally with just a few large-caps (generals) leading the way. Small and mid caps (troops) must also be on board to give the rally credibility. A rally that lifts all boats indicates far-reaching strength and increases the chances of further gains.

Bear markets have three stages — sharp down, reflexive rebound and a drawn-out fundamental downtrend.

Translation: Bear markets often start with a sharp and swift decline. After this decline, there is an oversold bounce that retraces a portion of that decline. The decline then continues, but at a slower and more grinding pace as the fundamentals deteriorate. Dow Theory suggests that bear markets consists of three down legs with reflexive rebounds in between.

When all the experts and forecasts agree — something else is going to happen.

Translation: This rule fits with Farrell's contrarian streak. When all analysts have a buy rating on a stock, there is only one way left to go (downgrade). Excessive bullish sentiment from newsletter writers and analysts should be viewed as a warning sign. Investors should consider buying when stocks are unloved and the news is all bad. Conversely, investors should consider selling when stocks are the talk of the town and the news is all good. Such a contrarian investment strategy usually rewards patient investors.

Bull markets are more fun than bear markets.

Translation: Wall Street and Main Street are much more in tune with bull markets than bear markets.

This commentary was originally posted Thursday, December 5, in Doug's Daily Diary on TheStreet Pro.