Doug Kass: A Feel-Good Market as Bad Times May Be Near

On many metrics the S&P 500 Index is more overvalued than at any time in nearly two decades. And though ignored by equity market participants, there are multiple and emerging warnings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The painting below is part of my sister's (Deborah Kass's) "No Kidding" series (2015-present). Debbie's "No Kidding" deploys the aesthetic formalism of post-war abstraction, as did her feel good paintings for feel bad times. But now, like my ursine market forecast, the mood has changed.

The palette has shifted to dark colors and the surfaces of the paintings are worn and washed out. Seemingly positive lyrical phrases such as how "Happy Days Are Here Again" and "We'll Be Young Forever" contrast with a sense that everything is not alright.

And here's a relevant pair of quotes from Berkshire Hathway's BRK.A BRK.B annual meeting:

Warren Buffett: "I would rather be 100x too cautious than 1% too incautious — and that will continue as long as I'm around."

Charlie Munger: "If we had used the leverage that a lot of successful operators did, Berkshire would be a lot bigger — but we would have been sweating at night."

I continue to be cautious regarding our stock market outlook. The advance in stocks has continued and the "animal spirits" have taken valuations ever higher — despite a continued reduction in corporate profit expectations. Specifically, over the last four months, the consensus expectations for third-quarter 2024 profit growth have dropped from a forecast year-over-year gain of 8% to less than 4%. To reach consensus 2025 S&P earnings per share forecasts, a questionable "hockey stick" recovery in profits will be necessary. Even more surprising is that the stock market has climbed, despite a rise of 65-basis points (up another four or five basis points this morning to a three-month high) in 10-year Treasury bond yields since the Federal Reserve's half percentage-point rate cut:

This recent backup in interest rates has followed an almost equal rise in inflation expectations:

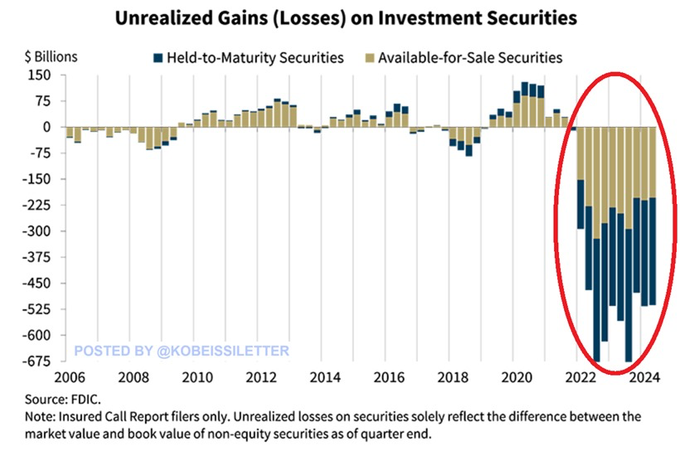

As a direct result — and ignored by market participants (much like in mid-2007) — is that unrealized bank industry securities losses are multiplying, reaching over $512 billion in the second quarter of 2024. This is seven times higher than at the peak of the Great Financial Crisis in 2008. (Bank of America BAC, alone, has 20% of the total of unrealized held-to-maturity securities losses):

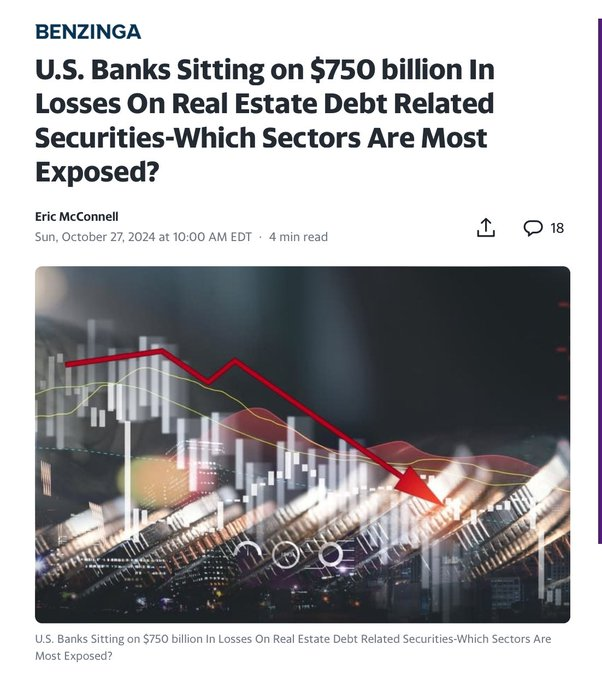

Also ignored by market participants (much like mid-2007), is that unrealized bank industry real estate losses are staggering:

Moreover:

* As I have observed previously, the dividend yield on the S&P index now stands at a meager 1.30% (versus 1.6% a year ago). That's compared to the 4.35% yield on the risk-free one-year Treasury bill. In other words, U.S. Treasuries now provide a near unprecedented (and greater than) 3-times the return that the dividends on the S&P index deliver in yield.

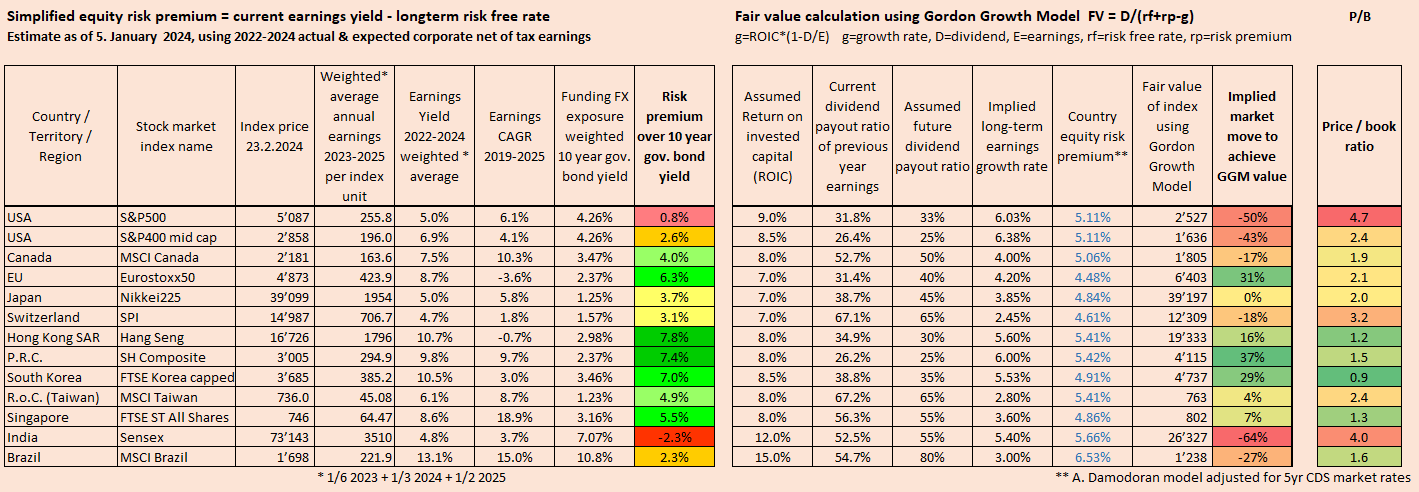

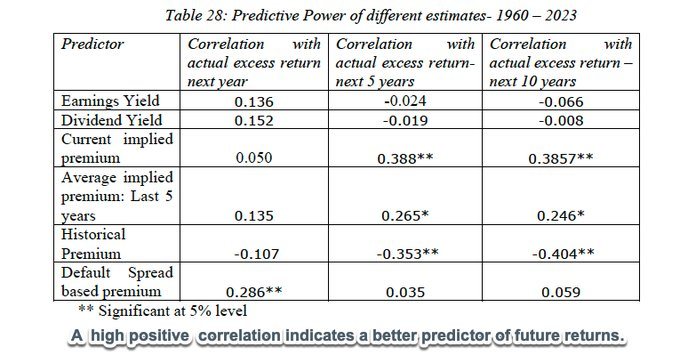

* These factors have contributed to an equity risk premium. The S&P earnings yield (inverse of the S&P's price/earnings ratio) less the risk-free rate of return available in bonds are declining to levels that are consistent with negative forward returns on equities:

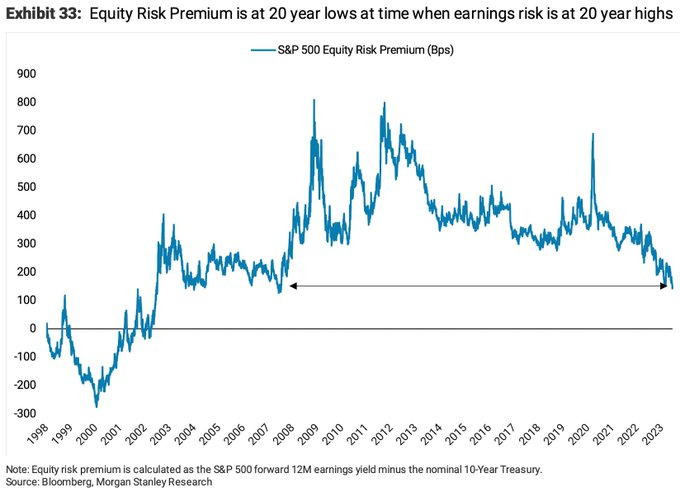

Here is a more updated view of how paper thin the equity risk premium is in the U.S. stock market:

Finally, the equity risk premium is among the best metrics in predicting future returns:

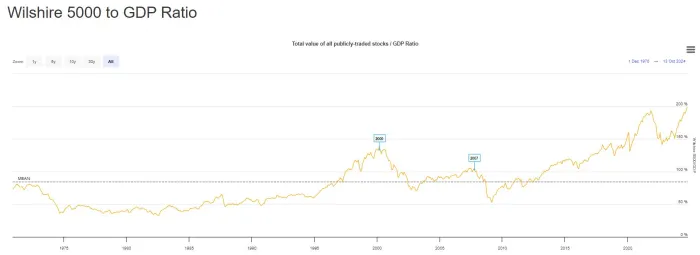

Another solid metric, The Buffett Indicator, is now at 199%, the highest level in history, surpassing the dot-com bubble and The Great Financial Crisis:

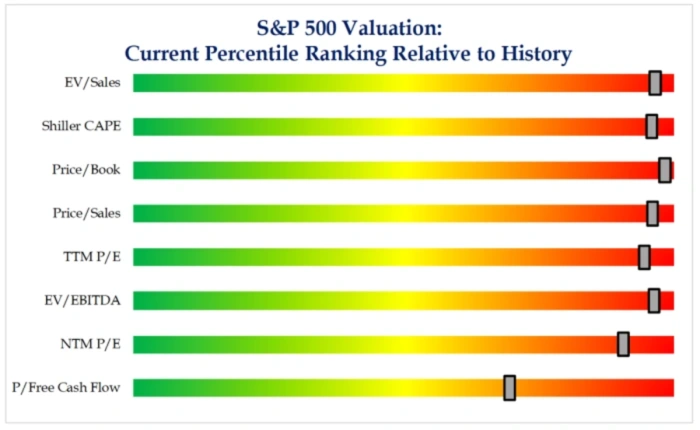

Equities, based on traditional valuation metrics, are in the 90%-95% tile of valuation:

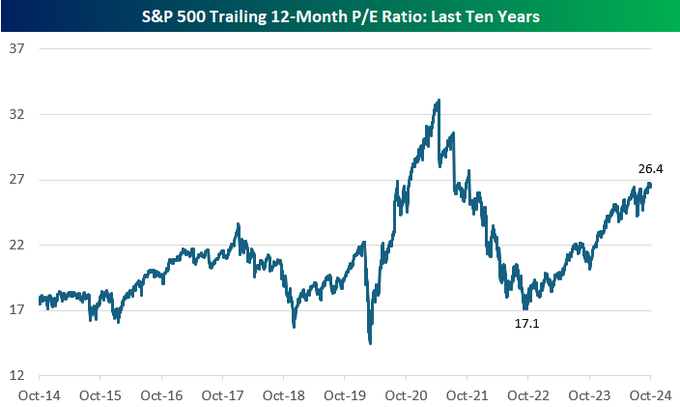

The S&P 500 Index trailing 12-month price-to-earnings ratio is above 28-times, up from 17-times at the start of the bull market in October 2022 — that's the 91%-tile of its 10-year range:

The Cash on the Sidelines Argument Is Laughable

From my Daily Diary on TheStreet Pro:

My main argument about the irrelevance of the absolute total money market assets, seen in a graph:

And from The Divine Ms M:

I recently noted that I am not alone in my ursine market outlook: We are in excellent company with Warren Buffett. In his third-quarter letter to Greenlight Capital investors, David Einhorn writes:

Warren Buffett is, of course, the most successful investor of his generation, and maybe of all time. While Mr. Buffett routinely points out that it is impossible to time the market, we can’t help but observe that he has been one of the best market timers we have ever seen. When the market got too frothy in the late 1960s, he closed his fund. Towards the market bottom in the early 1970s, he re-emerged as a stock picker and then prior to the 1987 crash, he sold everything except a couple of illiquid holdings. Later, he sidestepped the various crises in corporate credit and was well-positioned to capitalize on the 2008 global financial crisis. One could argue that sitting out bear markets has been the underappreciated reason for his outstanding long-term returns. It is therefore noteworthy to observe that Mr. Buffett is again selling large swaths of his stock portfolio and building enormous cash reserves.

Our sense is that Mr. Buffett’s portfolio adjustments are not a prediction that the market will fall next week, next month, or even next quarter. Rather, these stock sales more likely express a long-term view that right now is not a great time to have a lot of equity exposure, and that the opportunity set is expected to be better at some point in the not-so-distant future. We will avoid calling this market a bubble, and simply observe that the dividend yield is low and the P/E ratio is elevated despite corporate earnings being cyclically high, if not top-of-cycle...

The market isn't just making all-time highs. It is, by many measures, the most expensive stock market that we have seen since the founding of Greenlight.

The fact that the equity risk premium is paper-thin and that Warren Buffett shares our cautious view are not the limiting factors to our negativity.

In addition to the above concerns (of interest rates, a low equity risk premium and inflated corporate profit expectations), I remain of the view that the market is ignoring political and geopolitical headwinds, the prospects for slugflation (sticky inflation and sluggish economic growth), excessive price/earnings ratios (with traditional valuation multiples in the 90% to 95%-tile), fiscal and monetary policy risks, ebullient investor sentiment and the structural risks of a momentum-driven market on the steroids of passive investing.

I am even skeptical with regard to the single most important bullish theme in place today — that corporate profit margins and profits will materially and quickly benefit from the growth in artificial intelligence (AI). One would think that with all the society-changing technological innovation since 2000, GDP growth and S&P 500 revenue growth would have been faster, not slower, than in the past.

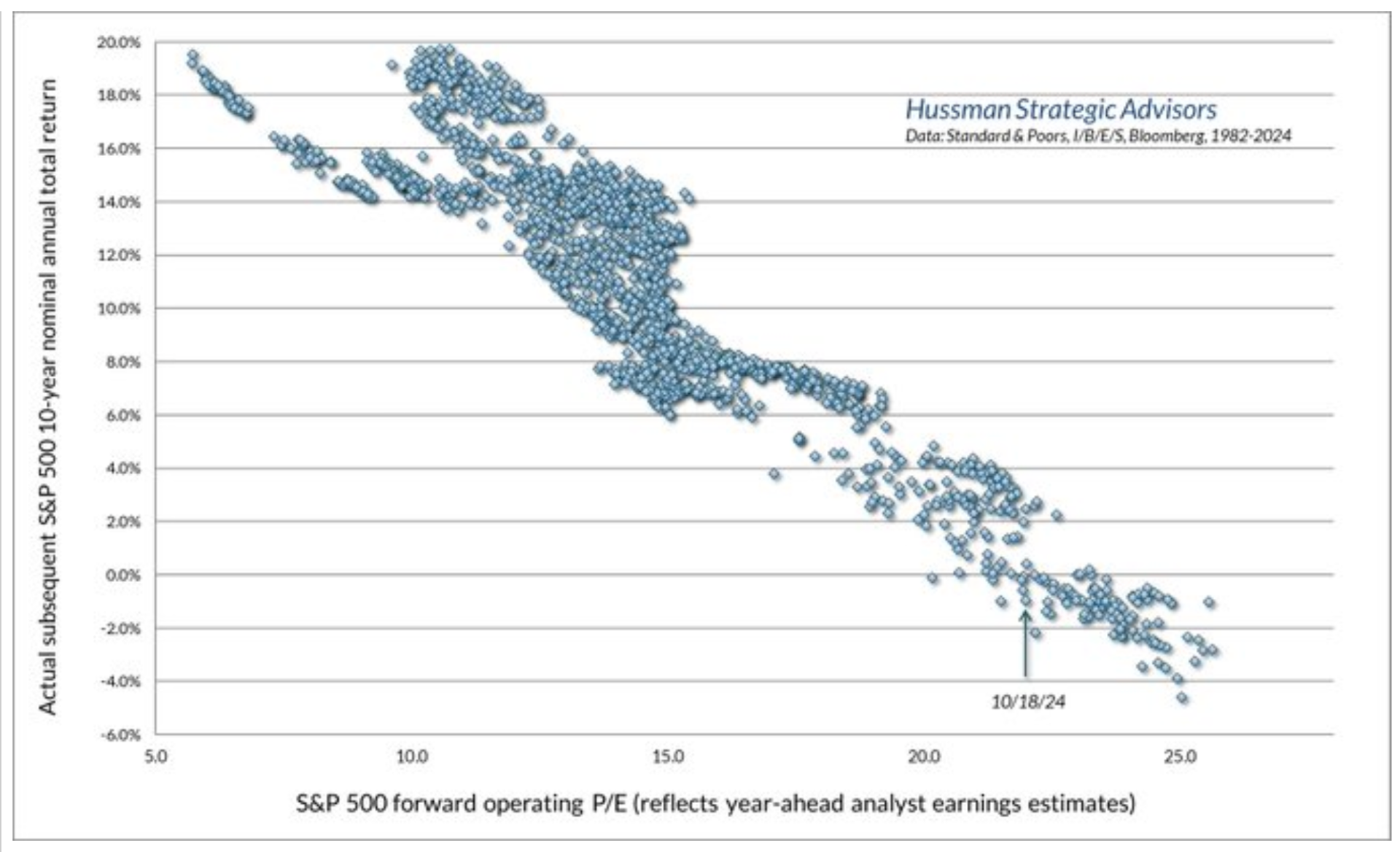

Investors make the repeated mistake of basing valuations on excitement instead of arithmetic:

Interestingly, using the S&P 500 forward operating price-to-earnings, which embeds unprecedented expectations for record profit margins, the implied S&P 500 10-year average annual nominal total return is still about zero:

In support of our view that inflation will remain sticky and higher than consensus forecasts, since the September-inflation cycle lows of less than a month ago, the CRB Index has "rallied" by nearly 10% and a series of union labor agreements (accompanied by high yearly wage increases) have been announced. (From The Fed Whisperer, Nick Timiraos' "Economists Warn of New Inflation Hazards After the Election" in Monday morning's Wall Street Journal.)

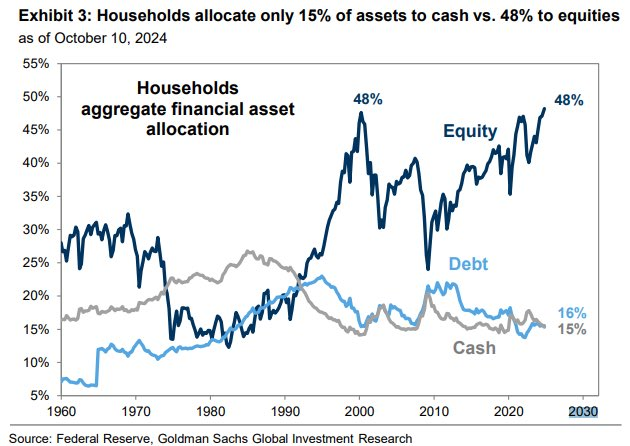

Positioning Is at a Bullish Extreme

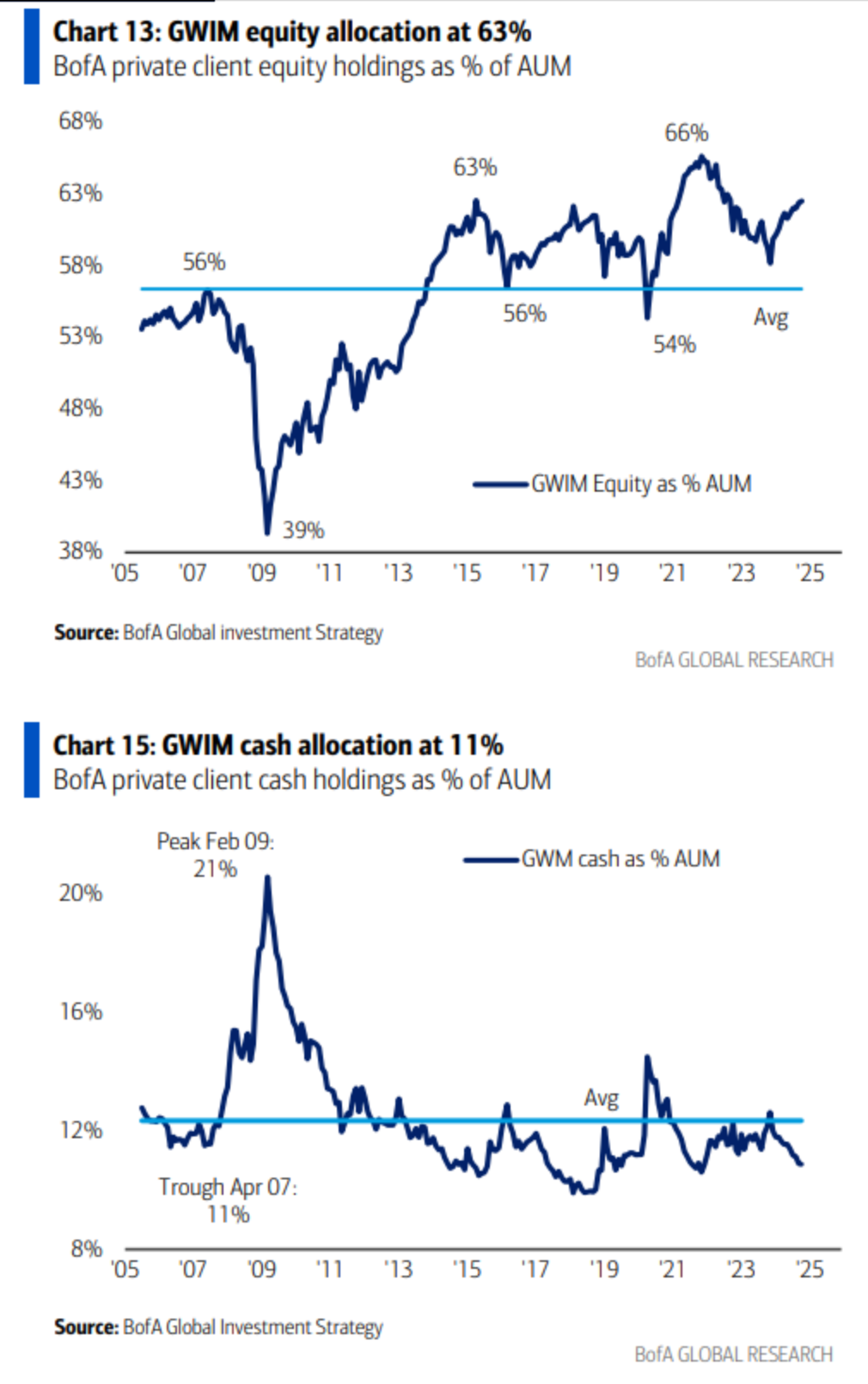

As to ebullient investor sentiment, as noted previously in my Diary, Merrill Lynch's data shows their private client accounts are well above average in their allocation to equities, while cash positions are below average:

Optimism is not confined to the retail investor.

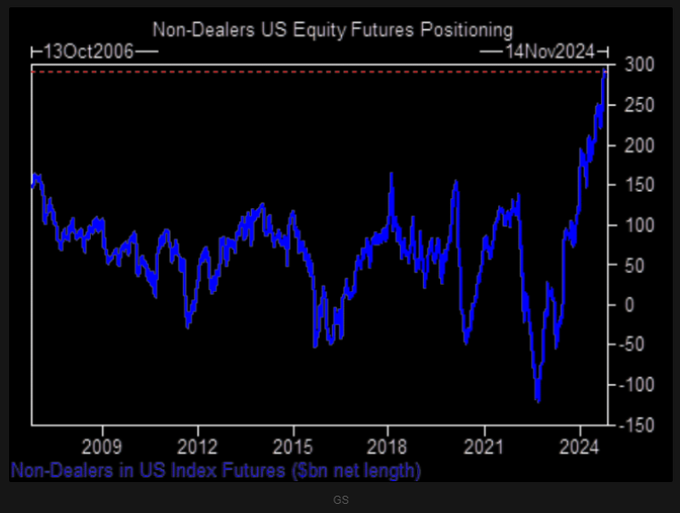

Goldman Sachs reports that traders have built up the largest long position in S&P futures in history:

To summarize, greed is increasingly conspicuous:

Fear and Greed Index - Investor Sentiment | CNN

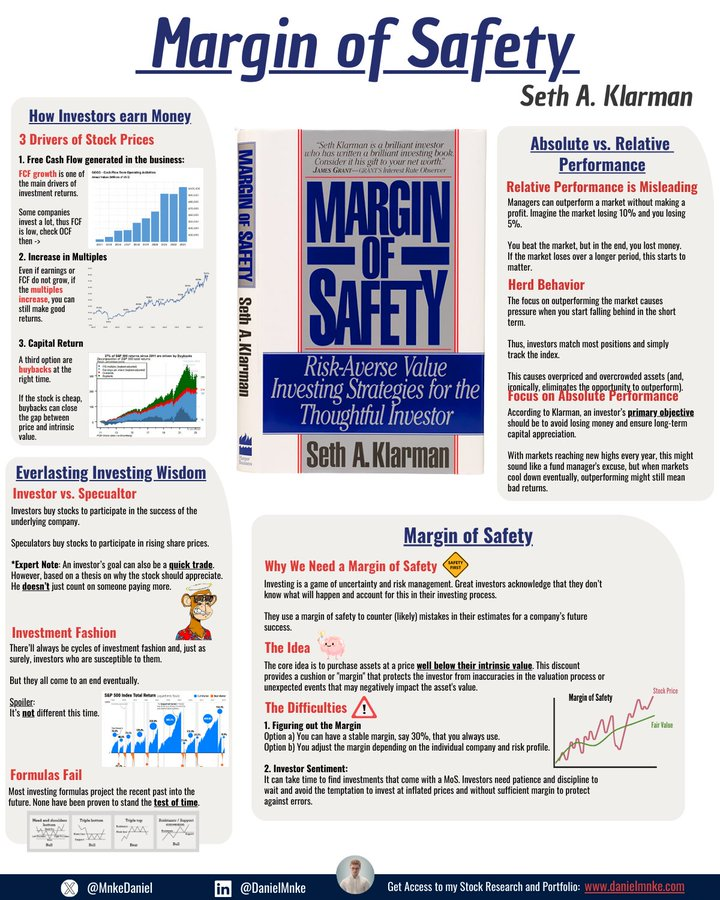

And market participants seem to have lost sight of assessing upside reward vs. downside risk and, even more importantly, are dismissing the fundamental concept of seeking a "margin of safety:"

I Vehemently Disagree With 'Oy'-the-Deficit Steve Eisman

Finally, I am of the view that fiscal profligacy (on both sides of the political aisle) represents a non-trivial risk to rising interest rates and lower equity valuations:

"The deficit is not the issue .... The "oy" the deficit people have been literally saying "the deficit" is a problem for forty years. Until it does everyone should be quiet."

- Steve "The Big Short" Eisman, Neuberger Berman (Watch Steve Eisman Talks US Election, Fed Policy and Crypto - Bloomberg)

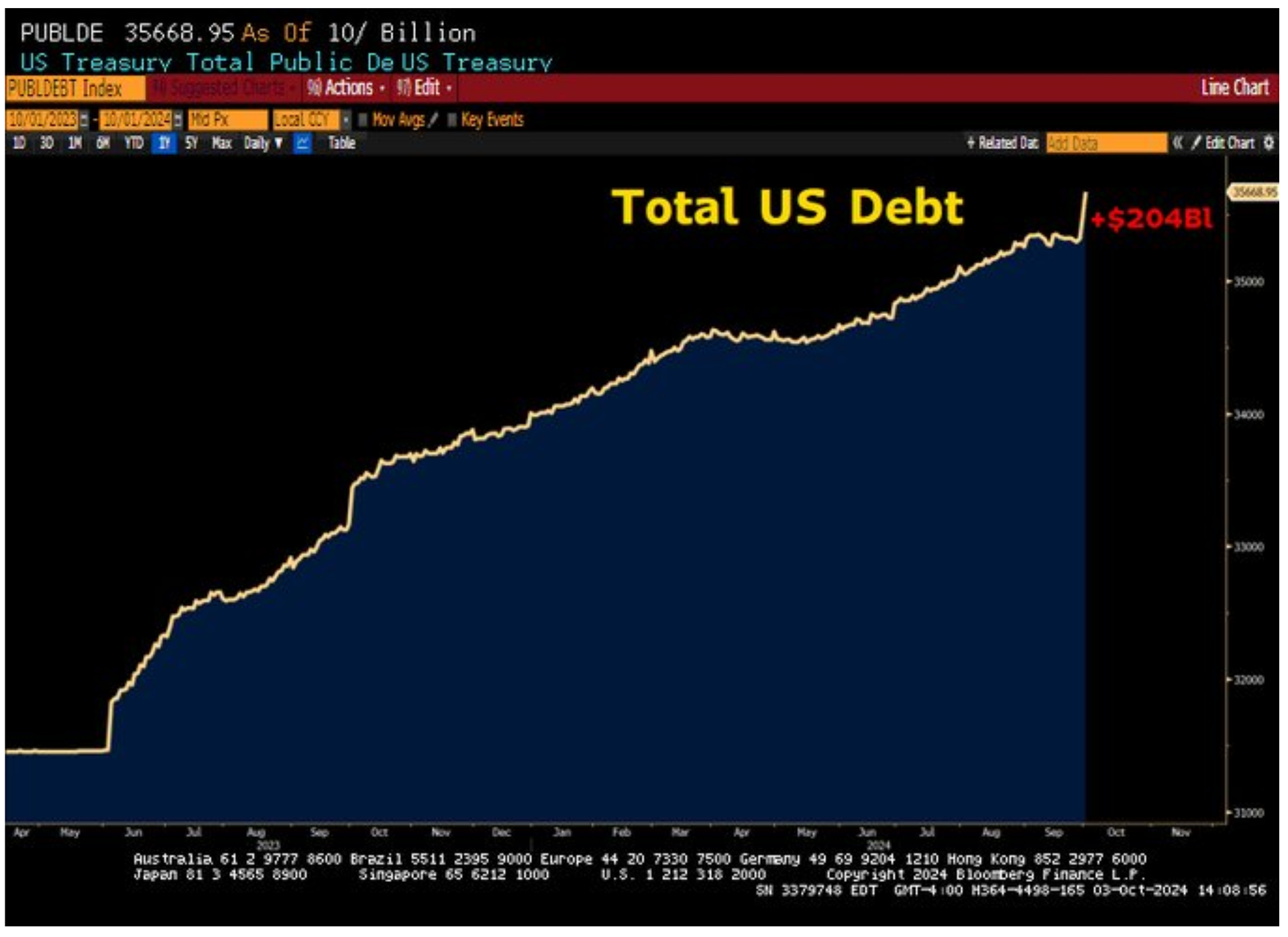

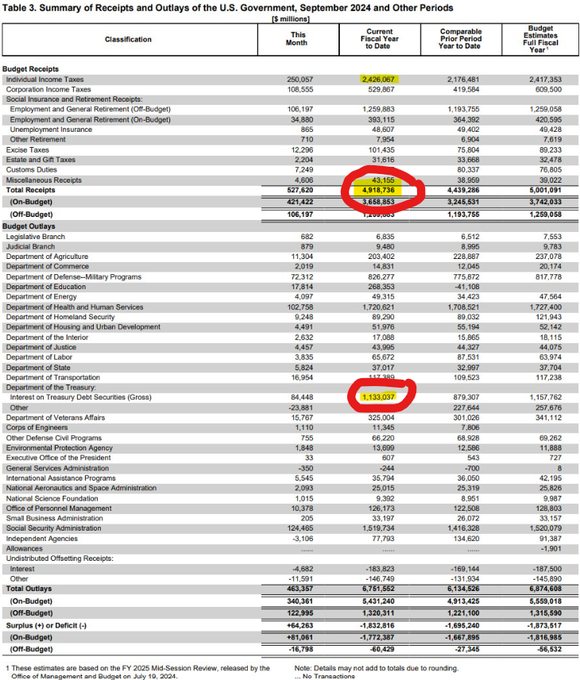

It has become popular to ignore our country's expanding deficit and expanding debt load. Consider, however, that in fiscal 2024 the total U.S. government revenue will be nearly $5 trillion. The annual interest on the national debt totals over $1.1 trillion (up from only $270 billion four years ago) — so 23% of all government revenue goes to pay the interest on our debt.

The average weighted coupon on the U.S.debt load is only 2.6% — but over $15 trillion comes due in the next two years. Given the Treasury Curve (with most maturities in excess of 4.0%), in the 2025 fiscal year (starting October 1, 2024) we are on pace for 30% of all government revenue going to interest payments:

I estimate that our country's budget deficit totaled more than 6% of GDP in the just ended 2024 fiscal year. With neither former President Donald Trump nor Vice President Kamala Harris prizing fiscal discipline, within five years our deficit could reach 8% of GDP. Writer Peggy Noonan described the situation well in a recent Wall Street Journal editorial, noting that the presidential campaign had reached its "Oprah phase," when TV star Oprah Winfrey would tell her studio audience, "You get a car and you get a car and you get a car."

Though ignored by equity market participants, there are other multiple and emerging warnings. Specifically, a rise in less benevolent stuff not usually associated with higher stock prices: increased equity volatility, higher bond yields and an all-time high of $2,700/ounce in the price of gold (and an outsized +32% year to date gain). These trends may foreshadow problems that could lie ahead for stocks.

In terms of portfolio structure, over the last few months I have been respectful of the market's strong price momentum and have maintained close a market neutral position with pairs trades comprising a large portion of my hedge fund's portfolio. However, should equities continue to advance this will not be a permanent situation! Indeed, I have moved back to net short on the leg higher in recent days to near all-time market highs.

That said, I am seeing the emergence of more long opportunities (in neglected areas) and short opportunities (in heavily owned areas) than at any time in the last several years. I am currently increasing our exposure in those unpopular stocks and sectors while increasing our short exposure in those overpriced and popular stocks and sectors.

Bottom Line

Finally, some visuals of my view as I go back to the abstract expressionism expressed by my famous artist sister, Deborah Kass:

Enough Already (another from Deb):

The S&P Index is more overvalued (in absolute terms) today than at any time in nearly two decades.

This commentary was orginally posted in Doug's Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.