Geopolitical Risk Has Increased and it's Time to Add Energy Exposure

It's imperative to address the recent U.S. presidential debate and investors should adopt this portfolio strategy.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

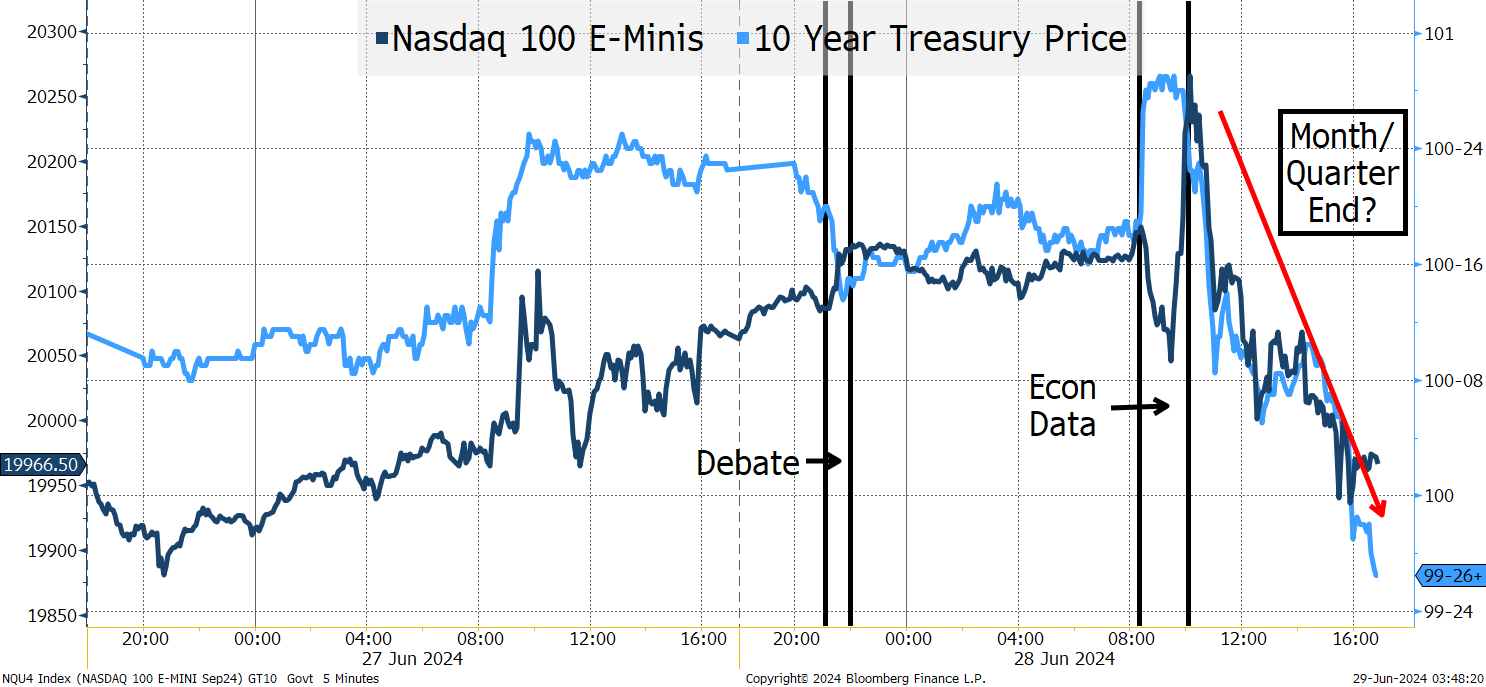

It is unclear what drove Friday’s weakness in stocks and bonds. On the surface, it wasn’t the debate, nor was it the economic data. It is unusual for both stocks and bonds to do so poorly at quarter end (if there was rebalancing, one asset class should be getting bought and the other getting sold).

Is it another warning sign, just a bump or nothing more than some strange quarter-end flows? I don’t know, though I think it remains very dangerous in the markets as the AI theme has been getting questioned more and more as time progresses and we haven’t seen any “gotcha moments” like we did when ChatGPT took the world by storm.

I do think the 10-year treasury yield should stay in the 4.3% to 4.5% range, with data helping push the yield lower, while deficit fears, auctions, etc., push it higher. We are smack in the middle of that range.

Increased Geopolitical Risk

European elections are nearing, and I’m leaning toward those causing some market hiccups in Europe. I’d avoid European risk here, and those elections could add pressure to U.S. markets.

While I am non-partisan (in fact, as a Canadian, I cannot vote in the U.S.), I feel it is imperative to address the presidential debate, because I think it has increased the risk of some sort of geopolitical event in the coming weeks.

There are two things that I think I can safely say about the debate:

- Based on betting data, we saw President Biden’s odds decline, noticeably, but former President Trump’s odds increased marginally. Basically, the betters were taking chips off the Biden table, and spreading them around, not just throwing them all to Trump.

- There is a conversation, at least at the moment, even by traditional supporters, of what the next step is for Biden.

I think it is important to think like our adversaries/competitors might think.

China (President Xi), Russia (President Putin), Iran (Supreme Leader Khomeini), and North Korea (Supreme Leader Kim) are all autocrats. They are in charge. What they say goes. They probable “know” about the nuances of the U.S. political system, but probably have difficulty grasping it. Likely, they see a leader who is being questioned, which might make it difficult for them to act.

The U.S. media was (and is) completely-domestically focused at the moment. This may be taken as an opportunity to take some action, expecting less intense scrutiny in the U.S.

To the extent any of these actors were planning on influencing U.S. elections, they probably already have some elements in place.

It seems plausible that, having watched the Ukraine funding debate and the relationship with Israel evolve since October 7, 2024, any bad actor has potentially added some new influencing tools to their tool kit.

A combination of misunderstanding how the U.S. works and overconfidence in their ability to win a misinformation campaign may give these bad actors the incentive to act sooner than later.

I want to own energy- and commodity-related assets now (the commodities, but also the stocks of companies in those industries). Since I’m worried about trade, in the event of some act, I’m leaning more toward energy than industrial commodities. I’ve been asked about gold and silver (and bitcoin), but I don’t have a strong opinion (though gold and silver would certainly seem to fit my geopolitical risk thesis).

I own XLE and will be adding as I think that is the best way to position your portfolio for a geopolitical shock and I think that risk has risen near-term.

At the time of publication, Tchir was long XLE.