A Sigh of Relief on Wall Street

Let's look at the action after the CPI landed, chart the Nasdaq, and see why target prices slipped for military contractors like Lockheed Martin, RTX and Northrop Grumman.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Relief: That's what Wednesday's trade felt like. In the morning, the Bureau of Labor Statistics released the November consumer price index report. There was real concern that the report might print a bit hotter than what was the "official" consensus view, which is not what happened.

As the numbers were published, one could almost hear an algorithmic sigh of relief across U.S. financial markets. Traders had spent the two days ahead of the release taking profits in spots and strategically reducing any associated risk. On Thursday, after that release, at least in those spots that had been weak on Monday and Tuesday, that risk was largely put back on.

As for November consumer-level inflation, on a month-over-month basis, headline prices as well as core prices, both grew 0.3% from October. At the headline, that was an acceleration from October's 0.2% growth, as food inflation, especially food at home, printed surprisingly hot at growth of 0.5%. Gasoline prices also started to rise again in November after three months of falling prices.

Regarding the year-over-year data, which tends to be arguably more important for this series to economists, headline inflation printed at growth of 2.7%, up from October's 2.6% print, while core inflation remained on a steady pace from the past two months at growth of 3.3%. Readers may recall that I had been looking for a 2.8% headline print and considering the way markets behaved on Wednesday, I was not alone.

To be fair, if one actually does the math, November headline inflation increased 2.73% from October, so the seemingly mild uptick was partially the result of rounding. Still, according to Fed Funds futures markets trading in Chicago, the probability for a quarter percentage-point rate cut to be made by the Federal Open Market Committee next week popped from 86% just ahead of the CPI release to 98% just after, and that is why our marketplace breathed that sigh of relief.

While the Fed may get this rate cut across the tape, going forward there are certainly no guarantees that consumer-level inflation has been licked. Core inflation, throughout this entire post-pandemic period, has never printed below year -over-year growth of 3.2%, and at the headline, November's 2.73% was up from October, which was up from September's 2.4% tag. That was the bottom. As for December, the Cleveland Fed's Nowcast model currently projects headline level inflation of 2.86%, while the Hedgeye model, which I pay for and has been invaluable, is up above 2.9%.

The Hedgeye model is the reason why I have appeared to be so accurate on inflation since projecting a bottom in September well ahead of September. I trade the markets, and I write the articles, but the credit for the accurate macro goes to Keith McCullough and the team at Hedgeye.

When Doves Fly

As U.S. markets prepare for the release (also by the BLS) on Thursday morning of November producer prices, the Swiss National Bank cut its policy rate by a surprising half-percentage point. As a non-euro denominated, independent European central bank, this is one of the planet's more important central banks. The SNB took its benchmark "main rate" down from 1% to 0.5%. A quarter-percentage point rate cut had been expected.

With consumer-level inflation in Switzerland likely to print at growth of just 1.1% for all of 2024 and drop from there going into 2025, currency traders are expecting further cuts from the SNB and are even starting to talk about a return to the "zero bound." For November, consumer-level inflation in Switzerland printed at year-over-year growth of just 0.7%.

Treasury Markets

Treasuries did not exactly react to the CPI print in the way one may have expected. Sure, yields dropped just after the release. Then, everything from one year of duration out to the 30-year long bond experienced a sell-off, while everything from six-month T-Bills down to 30-day paper flat-lined.

The yield for the U.S. Ten Year Note actually moved higher by four basis points for the session to 4.27% and now pays more than 4.3%, as I work my way through the zero-dark hours. On Wednesday, though, the Treasury Department raffled off $39 billion worth of new Ten-Year Notes in a rather successful auction.

The high yield awarded at auction was 4.235%, which stopped through the "when issued" quite aggressively at the time. Bid to cover printed at 2.7, which was the highest bid to cover for this series since 2016, as demand across the internals appeared strong. Indirect Bidders (foreign accounts) took down 70% of the issuance, while Direct Bidders (domestic accounts) took down 19.5%. Dealers were "stuck" with just 10.5% of the entire pie.

Equities

Surprisingly, while the Wednesday rally was certainly strong in spots, it was not as broad as one might have thought looking at their screen or their profits and losses. The S&P 500 gained 0.82% for the session as the Nasdaq Composite gained 1.77%. Small and mid-cap stocks gained moderately on the day, but both the Dow Industrials and Dow Transports closed out Wednesday's regular session in the red.

The real strength on Wednesday was in tech, supported by the Mag 7 stocks, which is where much of the risk-off behavior early this week had taken place. Just five of the 11 S&P sector SPDR exchange-traded funds closed the day in the green, led by the Discretionaries XLY at +1.76%. That sector was led by the autos that in turn were led by Tesla TSLA. Communication Services XLC and Technology XLK posted second and third place finishes for the day, gaining 1.63% and 1.45% respectively. Within tech, the semiconductors were hot, led by Broadcom AVGO and Lam Research LRCX, FYI, Broadcom is set to report the firm's quarterly numbers this evening.

Though six of these sector SPDRs closed in the red, only one gave up more than a full percentage point. That was Health Care XLV that closed down 1.36%. The three worst performing sector SPDRs for the day were all what you would consider to be defensive in nature.

This & That on Nasdaq

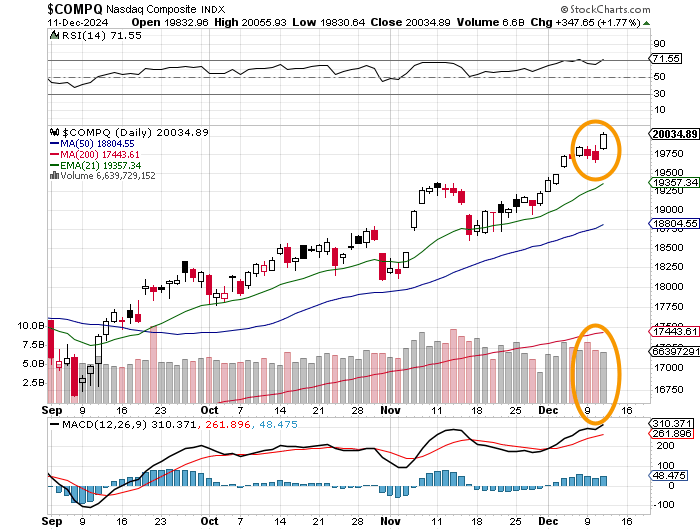

Remember when we noted that Tuesday's action did not confirm a change in trend on Monday? Yeah, good thing we wrote that. Take a look at this:

Still, while this chart otherwise appears to be taking off, one has to see that lower trading volume as perhaps representative of a low conviction rally. If last night's response to Adobe ADBE earnings is any indication, buckle your chinstraps.

As for Wednesday's breadth, it was less minty fresh than we would like. Winners beat losers by a mere 7 to 6 margin at both the NYSE and the Nasdaq. Advancing volume took just a 48% share of composite NYSE-listed trade, while aggregate trade across NYSE-listings increased slightly day over day.

At least advancing volume took a 59.2% share of composite Nasdaq-listed activity on Wednesday, but aggregate trade across those listings was down almost 3% day over day. Though a solid day, this was in my opinion, less than an enthusiastic shot in the arm.

Awful Treasury Department Release

How interesting is it that the Treasury Department released its November budget statement, and it was just awful. The budget deficit for the month of November was -$366.8 billion, which was worse than expected and combined with October's print of -$257.5 billion totals a deficit of -$624.3 billion. That by the way makes for the worst two month start to the government's fiscal year (that runs October through September) in the nation's history.

This did not stop the House of Representatives on Wednesday from passing the -$895.2 billion Defense Authorization Bill. Sure, I like defense spending as much as the next guy who served and has historically invested in the large defense contractors, but this bill adds up to $5.7 billion more than the Department of Defense had requested. Look, I know these guys. They don't ask for one penny less than they think they can get. In fact, they are more likely to try to push the envelope.

Remember a few weeks ago, when we discussed the potential impacts of the DOGE team, Elon Musk and Vivek Ramaswamy on defense spending and I told you then that with the election result in the U.S., the wars in eastern Europe and the Middle east would likely simmer down? I have shaved my defense longs, by the way.

Well, it looks like someone else is finally paying attention. On Wednesday, JP Morgan JPM cut estimates for valuation multiples across the industry and by extension, reduced target prices.

Five-star rated analyst Seth Seifman wrote, "We see a few potential headwinds for defense stocks emerging from the election, including a fiscally hawkish Office of Management and Budget, potential cuts to Ukraine support, and of course, DOGE."

Target prices were reduced for 11 big ticket defense contractors including my big four, Lockheed Martin LMT, RTX RTX, Northrop Grumman NOC and General Dynamics GD.

Economics (All Times Eastern)

08:30 - Initial Jobless Claims (Weekly): Expecting 224K, Last 221K.

08:30 - Continuing Claims (Weekly): Last 1.871M.

08:30 - PPI (Nov): Expecting 0.3% m/m, Last 0.2% m/m.

08:30 - Core PPI (Nov): Expecting 0.3% m/m, Last 0.3% m/m.

08:30 - PPI (Nov): Expecting 2.5% y/y, Last 2.4% y/y.

08:30 - Core PPI (Nov): Expecting 3.3% y/y, Last 3.1% y/y.

10:30 - Natural Gas Inventories (Weekly): Last -30B cf.

1:00 p.m. - Thirty Year Treasury Bond Auction: $22B.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: CIEN (.65)

After the Close: AVGO (1.39), COST (3.79), RH (2.66)

At the time of publication, Guilfoyle was long LMT, RTX, NOC, GD equity.