5 Threats to the Current Stock Rally

There are multiple red lights flashing on the market's dashboard right now.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

With the long-awaited "Great Rotation" continuing and indexes making new highs, it's all good, right? Not so fast...

The major equity indexes all closed closed near the highs of the day Tuesday, leaving all the index charts in near-term bullish trends as is cumulative market breadth.

However, there are multiple red lights flashing on the data dashboard that suggest some digestion of recent gains is becoming more likely. Indeed, as detailed below, one is very close to an historical topping signal. Additionally, investor sentiment remains too bullish.

Is the weak action Wednesday morning the beginning of that process?

More New Closing Highs

On the charts, all the major equity indexes closed higher on Tuesday with positive NYSE and Nasdaq internals on higher trading volumes.

All closed near their session highs with the S&P 500, DJIA and MidCap 400 making ne closing highs while the Dow Jones Transports, Midcap 400 and Russell 2000 closed above resistance.

All the near-term trends remain bullish although they are now almost vertical that likely can’t be sustained.

On the other hand, cumulative market breath is also bullish on the All Exchange, NYSE and Nasdaq.

No stochastic signals of import were generated.

Several Data Points Flashing Red, Suggesting Weakness

The data has become more threatening.

The 1-Day McClellan Overbought/Oversight Oscillators are all very overbought and suggesting some pause/consolidation (All Exchange: +126.57 NYSE: +127.89 Nasdaq: +127.61).

The percentage of S&P 500 issues trading above their 50-day moving averages (contrarian indicator) rose to 76% and just shy of the 80% historical topping signal.

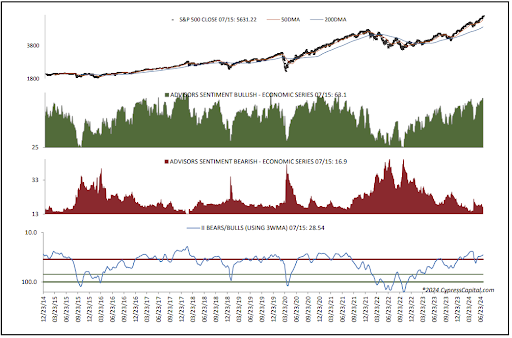

Also, the detrended Rydex Ratio (contrarian indicator) remains bearish at 1.18 with the leveraged ETF traders very leveraged long. Thus, two of the three sentiment indicators are bearish with this week’s AAII Bear/Bull Ratio (contrarian indicator) unchanged at 0.59 and neutral, while the Investors Intelligence Bear/Bull Ratio (contrary indicator) (see below) stayed bearish at 16.9/63.1 as bulls continue to outweigh bears by a wide margin.

The Open Insider Buy/Sell Ratio remains neutral at 32.4.

Leveraged ETF sentiment is 24.8, remaining neutral.

Valuation Remains a Concern

The 12-month consensus earnings estimate for the S&P 500 from Bloomberg rose slightly to $252.46 per share. However, its forward P/E multiple rose to 22.4x and well above the “rule of 20” ballpark fair value at 15.8x. This over 600-basis point premium remains significant.

The S&P's earnings yield slipped to 4.45%.

The 10-Year Treasury yield dropped to 4.17%. Support is 4.16% and resistance is at 4.29%. Its near-term trend is bearish.

The U.S. dollar, via the UUP ETF, closed flat at $28.73. Its trend is neutral with support at $28.69 and $28.94 as resistance.

Bottom Line

The nearly vertical chart trends along with the data red lights imply some near-term weakness.

We believe sell signals should be honored on individual names while any buying should be done only when names are near high-volume support and trading at discounts to their one-year forward growth rates with other considerations as well.