Who the Heck Is Adicet Bio?

Could this small-cap biotech company be a diamond in the rough for traders?

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Do we have a diamond in the rough?

I'm honestly not sure, but I have found a money-losing biotech that I would like to discuss. I speak of Adicet Bio ACET. Who the heck is Adicet Bio? This is a clinical stage biotech engaged in advancing its pipeline of "off-the-shelf" gamma delta T cells, engineered with chimeric antigen receptors (CARs), to facilitate durable activity in patients. The firm's leading product candidate, AD-001, is an allogeneic therapy expressing a CAR targeting CD20 and is being developed for the possible treatment of autoimmune diseases and relapsed or refractory aggressive B cell non-Hodgkin's lymphoma.

The firm's pipeline includes its leading preclinical candidate, ADI-270, which is an armored gamma delta CAR T cell product aimed at targeting renal cell carcinoma, with a potential for other CD70+ solid tumor and hematological malignancies. There has been recent news on this candidate. There are other candidates being worked on as well that are not as far along as these two.

The News

On Monday, Adicet Bio's ADI-270 cleared the FDA's new drug application (NDA) process to evaluate the candidate. The firm plans to initiate a Phase 1 clinical trial to assess the safety and anti-tumor activity of ADI-270 in renal cell carcinoma patients in the second half of calendar year 2024, with preliminary data expected by the first half of 2025. Chen Schor, the president and CEO of Adicet Bio, said “ADI-270 is the first ever gamma delta 1 CAR T cell therapy candidate to enter clinical trials for the treatment of solid tumors."

Back in May...

Adicet Bio updated progress in candidate ADI-100, which is on track to enter into a Phase 1 clinical study in the current quarter (Q2 2024) after receiving the same clearance that ADI-270 got back in December 2023. ADI-100 is being assessed for safety and efficacy in the fight against lupus nephritis. Preliminary data is expected in late 2024 or early 2025. The firm is also expected to submit an investigational new drug (IND) application for this candidate in renal cell carcinoma patients as well.

The Money

This is an issue... the firm has no sales. For the first quarter, ACET posted a Q1 GAAP EPS of $-0.35 on revenue of zero dollars and zero cents. This was better than the year ago print of $-0.72, but the firm has not reported any revenue at all since Q1 2022. Though the stock has no sales and trades at less than $2, eight sell-side analysts follow the stock, which I thought was interesting. The consensus view of these eight analysts is for a GAAP EPS of $-0.36 for the current quarter and $-1.45 for the full year. These analysts see the firm generating a small amount of revenue... $1.6 million for the full year. Interestingly, 10% of the float, even at these low prices, is held in short positions, which means that there will be a bid out there, somewhere.

As of the end of the March quarter, ACET had $247.6 million in cash on the books, with total assets of $293.1 million including the firm's property. Current liabilities amounted to just $17.5 million, while total liabilities less equity came to just $34.3 million. The firm has some lease obligations, but absolutely no debt. In other words, this is a pretty darned decent looking balance sheet, considering there is no regular sales or income.

May 15, 2024

This was the last time an analyst of any standing opined on the stock. John Newman of Canaccord Genuity (four stars at TipRanks) reiterated his "buy" rating with a $19 target price. That would be like a 1,200% rally from here. I had to look twice to make sure it was real. A couple of zero-star analysts have opined on ACET since, but I don't really look at poorly-ranked analysts very often unless I know their work.

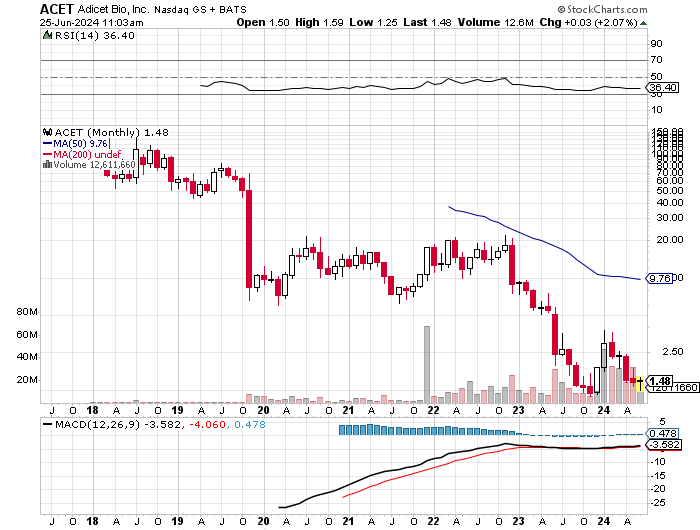

The Chart

This is a monthly chart that goes back to the beginning of ACET. This stock is not really chartable. I include the chart just to show how speculative this stock is, and make readers understand that. The stock traded with a $147 handle in 2018 shortly after going public. The risk/reward proposition ain't exactly what it once was for this name. I am not buying this name just yet. It is, however, on my radar. You may hear about it by early next year. Then again, you may not.

At the time of publication, Guilfoyle had no positions in any securities mentioned.