The Moment of Truth

Election Day is the big event this week — and it's looking really close. Also, let's check the mega-caps, the dismal jobs numbers, and more.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The moment of truth will arrive -- or will it? -- on Tuesday, Election Day. By all accounts, and with very little variance between them, the polls for the most part have kept expectations for this electoral outcome both at the executive and legislative levels, within their respective margins of error.

The candidates representing the two major political parties have both made policy proposals aimed at improving the current plight of the middle- and lower-income classes. Both have tried to address the badly skewed housing market and the mismatch between the asking price for the homes that are for sale and what is affordable for the young family, even when there are two adult earners leading the household.

Obviously, affordability is the very issue in the cross hairs for those voters who might truly be undecided. It's not the 2% to 3% inflation that, on paper, seems like a return to normalcy that has so many households rattled, it's the 20% to 25% cumulative inflation over the past three years. The fact is that for those who work full-time and have not been forced into part-time employment due to a lack of available hours, wage growth has only gained some 17% to 18% over that time. That's negative real wage growth.

Of course, there are other reasons beyond tax policy or affordability, to vote that could make for a higher priority across any number of demographics. The thing to remember for those of us who like parasites, regardless of political affiliation or preference, and make our living off of our financial marketplace, is simple: There will be knee-jerk reactions made by keyword reading algorithms. Then there will be a reaction to that knee-jerk.

There may be moves on Tuesday night in currency, treasury and foreign equity markets that will extend into U.S. markets on Wednesday morning. Actually, potentially well beyond Wednesday morning. Sure, there may be a definitive outcome. While that might seem nice, odds are that something cut and dry just won't be there.

The Federal Open Market Committee will hold its next policy meeting this Thursday. The idea was to put some separation between the election and the decision. There's a somewhat good chance that on Thursday afternoon, the Fed will be making its decisions in the dark about who will be leading the U.S. government by late January.

The Week That Was

I found it very interesting that after the Bureau of Labor Statistics posted what turned out to be the single worst month for non-farm payroll growth since the pandemic that equities spent the Friday session in the green, largely due to expectations that the report would permit the Fed to get as dovish as it would like to, going forward without reservation. I found it interesting, because U.S. Treasury debt securities fell out of bed on Friday. How odd was it that the equity market and debt security markets could come to such opposite conclusions?

Yes, odd, unless, equities investors are thinking easier money leads to increased liquidity, while debt security investors are thinking that easier money leads to a renewed acceleration of both producer- and consumer-level inflation and ultimately, a debt crisis that forces some kind of broad reset, or revaluation of the national fiat.

Now that I have cheered you up, the week just ended, even with the FOMC in a media blackout period, was one chock full of high-profile earnings releases and equally high-profile releases of macroeconomic data. The U.S. Ten Year Note paid as little as 4.22% mid-week and went out paying 4.38% late Friday. That same Ten-Year Note rallied sharply during the zero-dark hours on Monday morning.

As for those high-profile earnings, there were too many to count. Notably, however, five of the "Magnificent Seven" mega-cap names reported with mixed results. Both Alphabet GOOGL and Amazon AMZN found bids following Google's strong showings in subscriptions, devices and cloud services, and after Amazon posted strong revenue guidance for the holiday season.

Then there was the less-than-spectacular market reaction to the results and guidance posted by Microsoft MSFT, Meta Platforms META and Apple AAPL. I even reduced my long-side exposure to Microsoft, which is something I had not done in quite some time. Microsoft had been either the heaviest weighted or second heaviest weighted stock on my book for literally years. By Friday night, MSFT was still my number five, but just barely ahead of number six, which is the SPDR Gold shares ETF GLD. In fact, if I were to aggregate my gold-focused ETFs, gold would be a larger long position than MSFT, and that's not counting the real stuff (physical gold).

What a Week for the Macro...

It was a wild week for economics nerds like myself. I really am at my most comfortable when I am surrounded by numbers. Did I ever tell you about Sister Mary Anne? She was my trigonometry teacher in junior year of high school. She used to make me take my trig tests in the hallway because she couldn't figure out how I was cheating. I used to hand in the tests with just answers. No work visible on the paper and her head used to explode. That was fun.

She called my mother, and my mother said all he does in his free time is play a dice baseball game (Strat-o-Matic) with numbers. My mother vouched for my honesty. I wasn't really a good student, so the teachers didn't trust me when it came to mathematics where magically I could do everything correctly in my head. It wasn't the teachers' fault.

They just weren't used to a kid that had a before-school job and an after-school job. Those math skills came in very handy, just after high school when figuring windage and elevation for crew-served weapons (back when that was done by humans) and land navigation (back when that was done by humans) long before they ever came in handy on Wall Street (back when that work was done by humans).

Anyway... where were we? Oh, the macro. On Tuesday, Case-Shiller and the FHFA both told us that home prices were hotter than expected in August. We also found out from the job openings report that there were a lot less job openings across the nation in September than we thought.

On Wednesday, It Was Q3 GDP

The initial estimate of 2.8% quarter-over-quarter (seasonally adjusted annual rate) growth for third-quarter gross domestic product fell short of the consensus view that had been for 3%. Personal consumption expenditures made its largest contribution since the first quarter of 2023, which was positive, while gross private investment made its smallest contribution since that same quarter. Interestingly, federal spending was at its peak since Q1 2021. Note that spending on defense was at its highest level for the third quarter for several years. I was unable to go back further than 2020. Remember also that gross domestic income does not print with the first estimate so there were no checks and balances on this estimate.

On Thursday, It Was PCE Inflation

The September headline PCE Price Index printed at year over year growth of 2.1%, which was expected, down from 2.3% growth in August. At the core, the index accelerated from year over year growth of 2.6% in August to growth of 2.7% (also as expected). On a month over month basis, headline PCE printed at +0.2%, up from +0.1% and core PCE printed at +0.3%, up from 0.2%. This did nothing to upset the Fed's plan to ease monetary policy going forward. It also kept alive my thesis that headline inflation probably has bottomed in September and will now gradually build.

On Friday, October Jobs

The numbers were awful. Yes, there was likely some impact from the storms, but they were supposedly adjusted for. From the BLS Establishment Survey, Non-Farm Payrolls, once salted and peppered, increased by 12,000. That number was derived through government net hires adding up to a net +40,000, less a print of -28,000 for private sector net hires. (That's terrible, really terrible) The BLS also reported downward revisions in total of 112,000 to the August and September data. That put net "job creation" for the report at -100,000. Where I come from, that's called "job destruction."

Moving on to the Household Survey, the number of people that left the civilian labor force in October was 220,000, and the number of those outside of the labor force increased by 428,000. The number of unemployed persons increased by 150,000, while the number of employed persons decreased by 368,000. So, according to that survey, October job creation / job destruction was -368,000. The Participation Rate slowed from 62.7% to 62.6% as the Employment to Population Ratio dropped from 60.2% to an even 60%. Not pretty.

The GDP Game

Last week, the Atlanta Fed released their initial GDPNow model for the fourth quarter. Atlanta sees Q4 growing at a 2.3% pace (q/q SAAR). Among other central banks running close to real-time GDP models for the current quarter, the New York Fed released its initial Q4 for growth of 2.01%, while the Cleveland Fed sees Q4 growth of 2.66%. The St. Louis Fed is yet to post a Q4 estimate for GDP growth. These estimates are in their infancy. I say we give them a couple of weeks before we really start scrutinizing them.

Marketplace

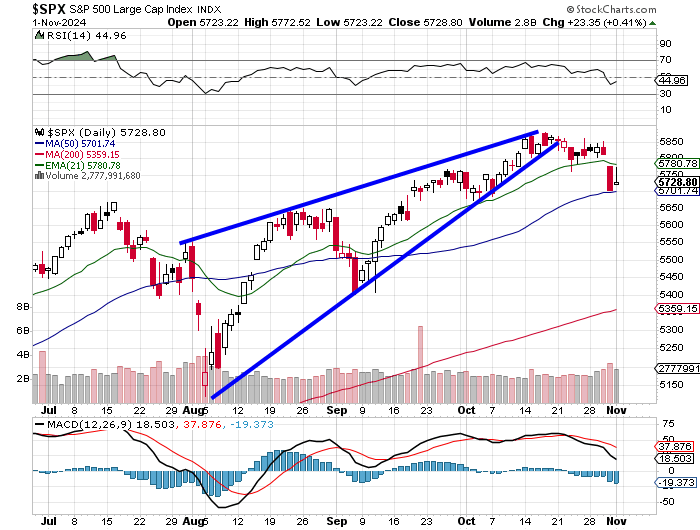

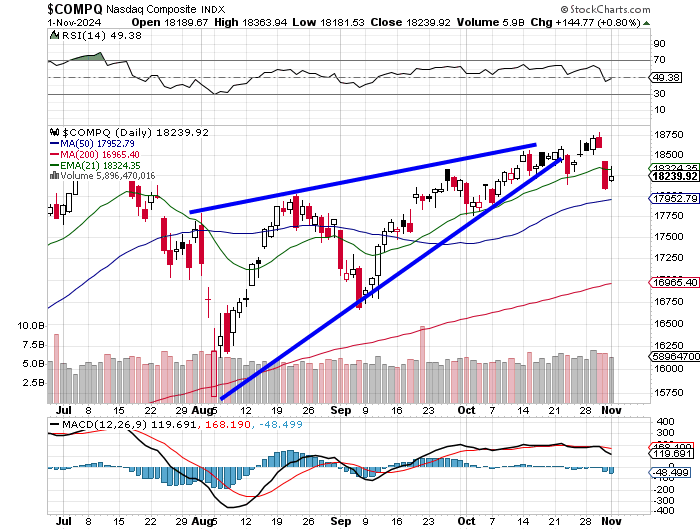

These charts look familiar to you guys? Did we nail these markets with our early recognition that these rising wedges were coming to a close ahead of the election or what? We did it together by taking a good look and trying to figure the financial marketplace out as it happened. Teamwork makes the dream work.

Readers will see that the S&P 500 has posted two successive "down" weeks as the daily Moving Average Convergence Divergence for that index rolled over. The S&P 500 closed at its 50-day simple moving average on Thursday and was able to make a stand there on Friday.

It's only one down week for the Nasdaq Composite. That ended a seven-week winning streak for this index. Here readers will see a less pronounced, but still bearish look for the daily MACD and an relative strength index that's still neutral. The fight here is around the 21-day exponential moving average, which is less significant to portfolio managers (but perhaps more important to traders), thus impacting the flow of capital to a lesser degree.

As for the major to mid-major U.S. equity indices last week....

- The S&P 500 gained 0.41% on Friday to close the week down 1.37%.

- The Nasdaq Composite gained 0.8% on Friday to still close the week down 1.5%.

- The Nasdaq 100 gained 0.72% on Friday to close the week down 1.57%.

- The Russell 2000 gained 0.61% on Friday, to close the week up 0.1%.

- The S&P Small Cap 600 gained 0.41% on Friday to close the week down 0.1%.

- The S&P Mid Cap 400 gained 0.16% on Friday, closing the week down 0.15%.

- The Dow Transports gained 0.61% on Friday to close the week up 1.53%.

- The Philly Semiconductors gained 1.11% on Friday, but still closed the week down 4.06%.

- The KBW Bank Index gave up 0.29% on Friday, closing the week up 0.63%.

On Friday, seven of the 11 S&P sector SPDR ETFs closed in the green, with the Discretionaries XLY out in front at +1.63%. The REITs XLRE and Utilities XLU both gave up more than 1% for the day. The other eight funds stayed within one percentage point of Thursday's closing prices.

For the week, just two of the eleven S&P sector SPDR ETFs closed in the green as Communication Services XLC gained 1.71%. Six of these funds gave back more than 1% for the week, three gave back more than 2% and the REITs gave back 3.02%.

Earnings

According to FactSet, which is the service that readers know I rely on for all things earnings-related, third quarter results perked up very nicely last week. Currently, for the third quarter, S&P 500 earnings are showing blended (results & expectations) year over year growth of 5.1% up from 3.6% a week ago. Revenue growth is currently running at blended growth of 5.2%, up from 4.9% three weeks ago.

Results and expectations for the third quarter are no longer negatively impacting the consensus view for both the fourth quarter and the full year as they had been. Q4 earnings growth is now seen at 12.7%, down from 13.4% last week and down from 14.6% three week prior. Full year earnings growth is still seen at 9.3 for a couple of weeks in a row.

For the third quarter, double-digit earnings growth is now only expected from the Communication Services (+21.7%), and Health Care (+12.1%) sectors. Expectations for Tech sector earnings growth have dropped all the way from +15.6% to just +6.4%. The Materials, Industrials and Energy (-25.5%) sectors are all expected to post year over year earnings contraction.

The S&P 500 goes into this week trading at 21.3-times forward looking earnings, down from 21.7-times a week ago, which is well above the five- and 10-year averages for the index of 19.6 and 18.1 times, respectively. The S&P 500 also trades at 26.7-times trailing 12 months' earnings, down from 27.2-times a week ago, which is also well above the five- and 10-year averages of 23.9-times and 21.8-times.

The Week Ahead

The week ahead will be different for sure. The Fed is still in "quiet mode" until the FOMC releases its policy statement followed by Jerome Powell's press conference on Thursday. The Treasury Department will raffle off $42B worth of new Ten-Year paper and $25 billion worth of new 30-Year Long Bonds on Wednesday and Thursday. There will be a plethora of quarterly earnings releases from corporate America, and some might be considered higher profile, but nothing like what we went through last week.

The main event this week, all of that aside, will be the national election in the U.S. It's going to be wild that night, gang. I will be on TV Tuesday night, but not here in the U.S. I think it will mostly be in Asia and on the Pacific Rim.

Among the more well-known names reporting this week will be my beloved Palantir Technologies PLTR this evening, Super Micro Computer SMCI on Tuesday evening, and CVS Health CVS, McKesson MCK, and Qualcomm QCOM all on Wednesday. On Thursday, Datadog DDOG, Moderna MRNA, Airbnb ABNB and The Trade Desk TTD will report, followed by Baxter BAX and Paramount Global PARA on Friday.

Nvidia and Buffett

On Friday evening, news broke that Nvidia NVDA will replace Intel INTC in the Dow Jones Industrial Average, while Sherwin-Williams SHW replaces Dow Inc DOW. Does this really matter? In terms of the flow of capital... not really. While it perhaps does serve to make the Dow 30 more relevant, the fact is that almost no money tracks the Dow Jones Industrials, and I don't know anyone in the business that still uses it in their analysis.

Also, in Berkshire Hathaway's (BRK.A, BRK.B) quarterly 13-F filing, we learned that during the third quarter, Warren Buffett's operation reduced holdings of Apple and Bank of America BAC by more than 20% each.

Economics (All Times Eastern)

10:00 - Factory Orders (Sep): Expecting 0.4% m/m, Last 0.4% m/m.

The Fed (All Times Eastern)

Fed Blackout Period.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BNTX (-1.73), ZTS (1.46)

After the Close: CE (2.84), CLF (-.31), NXPI (3.43), PLTR (.09), WYNN (1.10)

At the time of publication, Guilfoyle was long PLTR, AMZN, MSFT, GLD, XLU, NVDA, INTC, BRK.B.