Selective Buying Is in Order, But It Also Would Be Wise to Honor Sell Signals

Market conditions are better, but not super bullish.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Our near-term outlook for equities remains unchanged despite the elevated forward 12-month valuation for the S&P 500. We continue to believe the recent market correction has seen enough improvement that selective buying of equities with good fundamentals on weakness when they approach high-volume support levels is appropriate while issues that violate support should have their sell signals honored.

All the major equity indexes closed higher last Friday with positive New York Stock Exchange and Nasdaq internals as trading volumes dipped on both from the prior session.

All closed at or near their intraday highs that resulted in several of the charts closing above resistance, leaving their trends evenly split between bullish and neutral projections.

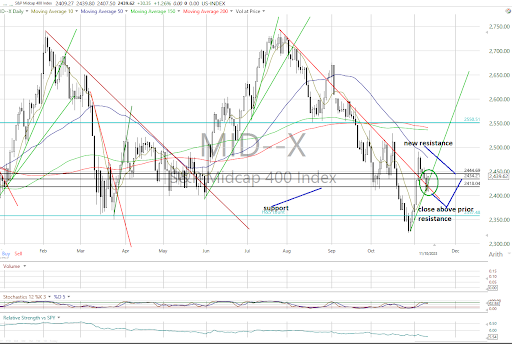

A Handful of Indexes Push Above Resistance

Notable technical events occurred on the S&P 500, Dow Jones Industrials, Nasdaq Composite, Nasdaq 100 and S&P 400 Midcap Index (chart below) as they closed above their respective resistance levels, leaving the near-term trends bullish for the first four indexes as the rest remain neutral.

Cumulative market breadth also remained neutral for the All Exchange, NYSE and Nasdaq.

Stochastic levels are still overbought for the S&P 500, Dow Industrials, Nasdaq Composite and Nasdaq 100 but have not yet seen bearish crossover signals. They can remain overbought for extended periods.

Still Plenty of Neutrality

The data remains largely neutral in its forecast.

The McClellan 1-Day Overbought/Oversold Oscillator is still neutral for the All Exchange and Nasdaq, with the NYSE's mildly overbought (All Exchange: +38.81 NYSE: +51.12 and Nasdaq: +32.96).

The percentage of S&P 500 issues trading above their 50-day moving averages (contrarian indicator) rose to 48%, staying neutral.

The Open Insider Buy/Sell Ratio was unchanged at 60.8, also staying neutral.

The detrended Rydex Ratio data (contrarian indicator) rose to 0.97 and is neutral. However, we would note it is nearing bearish signal levels.

The leveraged ETF sentiment (contrarian indicator) rose to 20.03, staying neutral as well.

Last week's AAII Bear/Bull Ratio (contrarian indicator) was essentially unchanged at 1.11, remaining neutral. The same was true for the Investors Intelligence Bear/Bull Ratio (contrary indicator) at a neutral 24.3/50.0.

S&P 500 P/E Multiple Remains a Concern

The forward 12-month consensus earnings estimate for the S&P 500 from Bloomberg has slipped to $235.76. Its forward price-to-earnings multiple of 18.7 is still well above the "rule of 20" ballpark fair value at 15.4 and is still a cause for some concern.

Its earnings yield is 5.34%.

The 10-year Treasury yield was unchanged at 4.63% and is in a neutral trend. Support is 4.49% with resistance at 4.7%.

The U.S. dollar also dipped to $29.84 and is also in a neutral trend. Support is $29.53 with resistance at $29.86.

In conclusion, we see an overall improvement in general market conditions after the recent correction. However, participation in current market strength appears selective. Thus, we are buyers on weakness of issues with good fundamentals and reasonable valuation as they near high-volume support levels. At the same time, names violating support should have their sell signals respected.

At the time of publication, Guy Ortmann had no position in the securities mentioned.