Relentless Rally, Palantir Power, The Economy, Stupid, Trading SoFi, ServiceNow

The beat goes on for this market, which surprised even me Monday with a 'kitchen sink' kind of day.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

To say that financial markets surprised me a bit on Monday would be accurate. The charts for the S&P 500 and the Nasdaq Composite, had, towards the end of last week, sent bearish signals, or to be honest, what I perceived as bearish signals. The breadth had been narrowing. On that count, there is no argument. The indexes had been led in a northerly direction by mega-cap tech stocks and the further north the headline indexes climbed, the more select the companionship seemed to be. That is, until Monday.

Monday was a kitchen sink kind of day. Equities rallied. All kinds of equities rallied.

Am I upset that I saw a bearish setup that proved to be fool's gold? Of course not. I'm still running several decisively net long portfolios. This is why I teach about confirming changes of trend. I can take individual profits here and there as target prices are reached, but changed my posture? Only when the markets tell me to do so. We win through the ability to adapt to our environment, not through trying to adapt our environment to what we think will or might happen.

We had a feeling that something was different when Friday's bout of equity market profit-taking turned out to be as shallow as it was.

Markets

The S&P 500 opened sort of flat on Monday as did the Nasdaq Composite. But the markets really turned on the juice over the final three hours of the regular trading session. After all, strategists at Citigroup C, Goldman Sachs GS, UBS UBS and Evercore ISI had all recently increased their year-end targets for the S&P 500. That last one, Evercore's Julian Emanuel, had been bearish. He now has an S&P 500 target of 6000, which would add almost another 10% to an index that is already up 14.75% year to date.

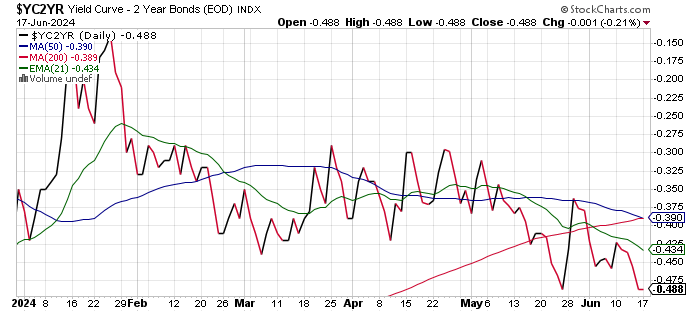

Bond traders did not feel like playing ball on Monday. The US Ten Year Note gave back four basis points as that yield climbed to 4.28%. The yield for the US Two Year Note moved up six basis points to 4.77% as that yield is back at its most inverted levels of 2024....

Note that the 200-day simple moving average for the negative spread between the yields for the US Ten- and Two-Year Notes crossed just below its 50-day SMA. This is what we call a "death cross" and in this case could signal a further deepening of this particular spread. That could be taken as a warning that a slower period of economic activity is at hand, perhaps even a recession.

That, however, is not the message being sent by equity markets at the moment. The S&P 500 gained 0.77% on Monday as the Nasdaq Composite gained 0.95%. This time, most equity indices, even those more specialized in character, rallied as well. The Philly Semiconductors ran 1.6%, as the Nasdaq 100 popped for 1.24%. The KBW Banks gained 1.12%. The Dow Transports and all three of our small to midcap indices added between 0.79% and 0.92%. It was a "risk-on" Monday down at 11 Wall Street and up at Times Square.

Breadth

Did equity traders get a tip that bond traders did not see ahead of Tuesday morning's data for May Retail Sales and Industrial Production? Sure seemed like it.

Eight of the 11 S&P sector SPDR ETFs closed in the green, with three of these funds gaining at least 1% for the day. Discretionaries XLY led the way, up 1.76%, led by the autos that in turn were led by Tesla TSLA. Technology XLK and Industrials XLI finished the day in second and third place. Very interestingly, the three sector SPDRs that closed in the red were all defensive in nature. The Utilities XLU gave up 1.1% on Monday, followed by the REITs XLRE and Health Care XLV.

Winners beat losers at the NYSE by roughly 3 to 2 margin and by just a smidge at the Nasdaq. However, advancing volume took a decisive share of composite action for names listed at both exchanges at 62.8% for Nasdaq names and 60.4% for NYSE names.

It's probably somewhat important to note that aggregate trading volume increased on Monday from Friday by just a bit for NYSE listings and the membership of the S&P 500. More impressively, trading volume increased 21.9% on a day-over-day basis for Nasdaq listings. This does mean that managers were moving money.

The Economy, Stupid

On Monday, there was really just one macroeconomic datapoint released. It would be difficult to credit the June version of the New York Fed's regional Empire State Manufacturing survey with the day's risk-on behavior. The June survey did print better than expected, but overall, conditions still deteriorated from May. That headline print landed at -6.0, after May's -15.6, April's -14.3 and March's -20.9. So, maybe deterioration in the New York region's manufacturing sector is slowing? Maybe as well that there is simply no blood left in the patient.

This survey has now been mired in negative territory for seven consecutive months. New Orders continued to contract, but far less rapidly, as unfilled orders and inventories actually grew. Prices paid and prices received both continued to increase, but at a slower pace, but unfortunately, both number of employees and average workweeks accelerated in their rate of contraction from May. The Philly Fed will publish their similar survey for June this Thursday and has been positive for a couple of months now. That should tell us more.

Readers can expect the Atlanta Fed to revise their GDPNow model for the second quarter later this morning. Currently, the Atlanta Fed sees Q2 GDP at growth of 3.1% (q/q, SAAR), but that model has not been revised since June 7. The other three regional Fed districts that run real-time GDP models revise those models only on weekends. None of those three have been as optimistic as Atlanta. For the second quarter, New York is at growth of 1.91%, St. Louis is at growth of 0.94%, and Cleveland is at growth of 0.67%. So, there is quite a difference in opinion.

Very interestingly, a reader who I would love to credit, but I don't know if she would like that, sent me RBC Wealth Management's weekly letter from this past Friday. Long story short, RBC runs a U.S. recession scorecard that tracks seven categories. Three of these categories are already in recessionary territory, two are in cautionary territory and just two are in expansionary territory.

Perhaps equity market portfolio managers are showing an eagerness to push this rally higher less due to the Fed being free to cut short-term rates after a cool May for consumer and producer-level inflation, but more due to the Fed having to be ready to act. Ready to as a "soft landing" can so easily turn into something worse. Once there, negativity begets more negativity.

As I have told you many times, recessions can depress economic activity for far longer than many understand. The "Great Recession" ended statistically in 2009. Yet, many lower- and middle-class Americans felt that the U.S. economy was still in contraction as late as 2016. Losing jobs, suppressed mobility, and stagnant wages leave scars. Scars change behavior.

Oh, I root for a soft landing. We have to. Yet calling for one, or even what I heard of late described as a "shallow" recession? That's like poking the bear.

The Fed

We have five Fed speakers set for later today, so don't be surprised if there has been a unified message sent by the central bank by late this afternoon.

On Monday, Philadelphia Fed Pres. Patrick Harker spoke publicly. He said: "If all of it happens to be as forecasted, I think one rate cut would be appropriate by this year's end. Indeed, I see two cuts or none, for this year as quite possible if the data break(s) one way or another. So, again, we will remain data dependent."

Harker then added... "I believe that the current policy interest rate, which has been held steady for nearly 11 months, will continue to serve us well for a bit longer, holding us in restrictive territory to bring inflation back to target and mitigate upside risks."

Trading Notes

-- Palantir Technologies PLTR gained 6.15% on Monday to close at $25.02. On Friday, here at TheStreet Pro, I increased my target price for this name from $29 to $31. On Monday, Joseph Bonner of Argus Research, who is rated at five stars by TipRanks, initiated PLTR with a "buy" rating and a $29 target price. PLTR remains a top ten holding of mine.

-- I did add to my long position in SoFi Technologies SOFI on Monday on early weakness. The stock struggled to close unchanged for the session at $6.46. SOFI is also a top ten holding of mine.

-- I reduced long side exposure to ServiceNow NOW on Monday at that stock's 50-day simple moving average (SMA), which is where that stock has hit resistance on four successive trading sessions.

Economics (All Times Eastern)

08:30 - Retail Sales (May): Expecting 0.3% m/m, Last 0.0% m/m.

08:30 - Core Retail Sales (May): Expecting 0.2% m/m, Last 0.2% m/m.

08:55 - Redbook (Weekly): Last 5.5% y/y.

09:15 - Industrial Production (May): Expecting 0.2% m/m, Last 0.0% m/m.

09:15 - Capacity Utilization (May): Expecting 78.6%, Last 78.4%.

10:00 - Business Inventories (Apr): Expecting 0.3% m/m, Last -0.1% m/m.

13:00 - Twenty Year Bond Auction: $13B.

13:00 - Net Long Term TIC Flows (Apr): Last $100.5B.

16:30 - API Oil Inventories (Weekly): Last -2.428M.

The Fed (All Times Eastern)

10:00 - Speaker: Richmond Fed Pres. Tom Barkin.

11:40 - Speaker: Boston Fed Pres. Susan Collins.

13:00 - Speaker: Reserve Board Gov. Adriana Kugler.

13:20 - Speaker: St. Louis Fed Pres. Alberto Musalem.

14:00 - Speaker: Chicago Fed Pres. Austan Goolsbee.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: PDCO (0.82)

After the Close: KBH (1.81)

At the time of publication, Guilfoyle was long XLU. PLTR, SOFI and NOW.