Here's How to Keep Generating Healthy Income as Interest Rates Fall

With investors talking about impending rate cuts and election outcomes, these dividend/higher-yielding stocks and strategies will keep you on track.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It’s a virtual lock: The Federal Reserve WILL be cutting interest rates soon. The only questions on Wall Street are “When?” and “By how much?”

Investors who are looking to keep generating healthy income even as yields fall DO have options. This week’s bundle of MoneyShow articles covers some stocks and strategies that will help you out.

Kelly Green Dividend Digest

How a Yield-Focused Investor Should Treat Election-Driven Volatility

As much as my two-pronged dividend strategy works in all markets, we still need to acknowledge that politics influences things. Sometimes it’s a tangible impact like big swings in the price of oil. Other times it’s just investor sentiment moving the market. Either way, it can affect the short-term progress of our portfolio, advises Kelly Green, editor of Dividend Digest.

I’ve seen countless articles trying to spot patterns and make arguments on how to handle your portfolio during an election year. It’s the big question on everyone’s mind. So, is it time for fight or flight?

Before I give you my opinion on that, I first had to search for some numbers. According to Fidelity, US stocks have returned an average of 9.1% in election years since 1950. The S&P 500 has so far done slightly better than that, up 12% year to date.

(Editor’s Note: Kelly Green is speaking at the 2024 MoneyShow Orlando, which runs Oct. 17-19. Click HERE to register)

The S&P 500 has also historically averaged positive returns regardless of which party controlled the White House or Congress. The stock market actually does best with a divided Congress no matter if the president is a Democrat or a Republican (based on data from 1933‒2022, excluding 2001‒2002).

Generally, stocks keep going up over the long term. As the Oracle of Omaha would say, “The stock market is a device for transferring money from the impatient to the patient.” Most of the time we aren’t trying to time the market. The plan is to hold our positions for at least a few years.

We know markets go up and markets go down. And sectors within the overall market go up and down as well. And of course, individual stocks can bounce all over the place. If the goal is to buy low and sell high, then we need to know exactly what “buy low” means so we can be on the lookout for those opportunities.

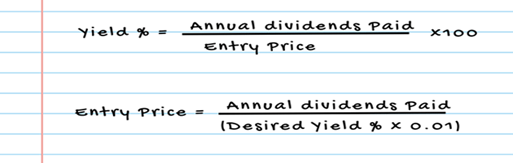

Having an up-to-date watch list means you’re ready to strike when the time is right. Your watchlist should also include your desired entry price for every stock. I calculate this based on the dividend yield I want to get.

Once armed with your desired entry price, it’s just a matter of waiting for the right time to buy. No trying to time the market. When the stock hits our entry price, we buy shares.

Marc Lichtenfeld Wealthy Retirement

One of Several Utilities Worth Targeting as the Fed Cuts Rates

The federal funds futures market is indicating that there’s a 100% chance of an interest rate cut at the Sept. 17-18 Federal Reserve meeting. Interest rate-sensitive sectors like utilities would be some of the biggest beneficiaries of lower rates, including Duke Energy Corp. DUK, suggests Marc Lichtenfeld, chief income strategist at Wealthy Retirement.

Futures markets also show a 74% probability of rates being at least a full percentage point lower by December. Due to the recent rise in unemployment, some have even been calling for an emergency rate cut of as many as 75 basis points (three-quarters of a percentage point) before the September meeting.

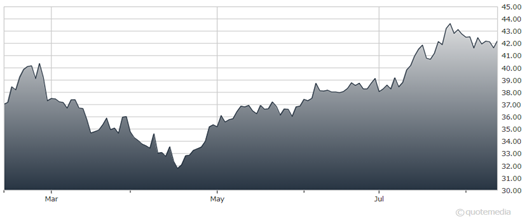

DUK, NEP, NJR (YTD % Change)

If rates do decline, there are certain sectors and stocks like utilities that will surely benefit. Since utilities tend to borrow a lot of money, lower rates mean lower interest payments.

There are plenty of quality utilities to choose from. But I like utilities like DUK that generate some of their power from nuclear power plants. Duke also pays a consistent dividend.

If you’re hunting for bigger yields, you might consider NextEra Energy Partners LP NEP , which I’ve been pounding the table on for months. At recent prices, it paid a 14.5% yield. I also like New Jersey Resources Corp. NJR, which recently announced that it expects earnings growth of 7% to 9% annually over the long term.

Recommended Action: Buy DUK.

Ben Reynolds Sure Dividend

A Healthcare REIT with a Very Healthy Dividend

Universal Health Realty Income Trust UHT specializes in the healthcare sector. The trust’s property portfolio includes acute care hospitals, medical office buildings, rehabilitation hospitals, behavioral healthcare facilities, childcare centers, and sub-acute care facilities. Universal Health was founded in 1986 and has a current market capitalization of $588 million, writes Ben Reynolds, editor of Top 10 REITs.

On July 24, Universal Health announced second-quarter results. Funds from operations (FFO) for the period was $12.4 million, or $0.90 per diluted share, compared to $10.6 million, or $0.77 per diluted share, in the prior year. Universal Health is projected to generate FFO of $3.67 per share for 2024.

Universal Health Realty Income Trust (UHT)

On June 5, Universal Health announced that it was raising its quarterly dividend by 0.7% to $0.73. The stock has an attractive dividend yield of 7%. While such a high yield can be a warning sign, we believe the trust’s dividend is likely safe.

First, Universal Health has grown its dividend for 40 consecutive years, which is the second-longest dividend growth streak among REITs in our coverage universe. The payout ratio has often been high. For example, the expected payout ratio for 2024 is 80%. This is an elevated level, but it is below the 10-year average payout ratio of 84%.

Second, FFO growth is projected to outpace dividend growth, providing a larger margin of safety over time. While we do not believe that Universal Health has significant competitive advantages relative to its peers due to its size, the REIT healthcare space should see tailwinds from an aging demographic. There are more than 70 million Baby Boomers in the US, which should provide ample growth opportunities for this industry.

Shares of the trust are trading at 11.4 times expected FFO for 2024. We believe fair value is closer to 12 times FFO, implying a tailwind from multiple expansion. Reaching our target price-to-FFO ratio by 2029 could add 1% to annual returns over this period.

In total, we forecast that Universal Health can offer a total annual return of 9% through 2029. This projection stems from FFO growth of 2.5%, a starting dividend yield of 7%, and a low single-digit tailwind from multiple expansion.

Recommended Action: Buy UHT.