Did Scotiabank Just 'Unlock' a New Opportunity for Traders?

Is it time to secure a position in KeyCorp after BNS' 14.9% stake news? Here's how I'm handling my shares.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Even when I am not particularly enthralled with the financials, I always maintain some level of exposure. As I am a fan of Charlie Scharf, and I expect the Fed to ultimately end its restrictions on Wells Fargo WFC one day, that has become my fallback large money center bank. Not a lot of creative thought there. Bland meat and potatoes banking, with an interest in growing what has been a meager attempt to compete in the world of investment banking. Despite the recent tail-whipping, I am still up 13% on the name, so I cannot complain.

My fallback regional bank, on and off for many years now, has been KeyCorp KEY. This is a well-run, in my opinion, Cleveland-based financial services operation with a number of subsidiaries, primary among them, would be KeyBank. The bank runs consumer-focused and commercial-focused segments and has managed to make me money in the past. Besides, banking analyst Mike Mayo of Wells Fargo, who's rated five stars by tip ranks, rates KEY at a "Buy" rating with a target price of $8. Mayo has noted Key's strong backlog in capital markets activities, which has boosted his confidence in the company's ability to meet full year targets.

Readers may recall that for the second quarter, which KeyCorp reported in mid-July, the bank beat unadjusted earnings per share expectations by a penny, but fell short of revenue projections, while seeing a year-over-year contraction on that side of the ledger. The bank cut its guidance for full-year average loan contraction to 7% to 8% from prior a contraction of 5% to 7%. But KeyCorp took guidance for full-year average deposits up to flat from the year ago comp from an expectation for flat to down 2%. KeyCorp also reaffirmed net interest income on a taxable equivalent basis to drop between 2% and 5%.

The $2.88B News

Seemingly out of nowhere, came news this morning that Scotiabank BNS would acquire an eventual 14.9% stake in KeyCorp for $2.88 billion. The equity stake will be purchased through an issuance of common shares (dilution? Yeah, but at a premium) at a price of $17.17 per share, which would be about a 17.5% premium over Friday's closing price of $14.61 and an 11% premium over the volume weighted price for KEY over the past 20 trading sessions.

The shares will be purchased in two tranches, the first will be an initial investment of 4.9% expected to close during the fourth quarter of this year, and the balance (10%) later on, expected to close in fiscal 2025.

The infusion of cash for equity will impact KeyCorp's Common Equity Tier 1 ratio, to the tune of an estimated 185 to 210 basis points when all is said and done, which will provide a nice sized cushion as Basel III requirements are finalized.

CEO Chris Gorman

On the ScotiaBank's investment, Key Corp CEO, Chris Gorman, said "Scotia Bank approached us with a unique opportunity to raise capital on attractive terms. While we continue to be comfortable with our current capital position, we determined that the investment enables Key to accelerate our well-communicated capital and earnings improvement while bolstering our strategic position."

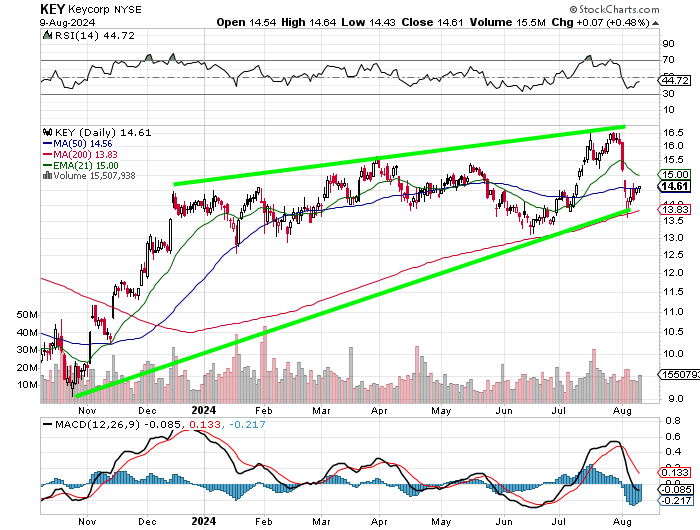

Chart Check

Readers will see that KEY had been building a rising wedge from way back in November up into the present. This is a pattern of bearish reversal that one tries to ride until said reversal occurs. With the stock trading toward the bottom of the range, and struggling to maintain contact with its 50-day simple moving average, I had to wonder if the time was upon us to bail out of this name.

On top of that, both the Relative Strength Index and daily Moving Average Convergence Divergence indicator were postured in an aloof, somewhat negative way. The 200-day simple moving average would have been our downside pivot.

This news obviously renders this setup useless and will likely see the shares break through the upper trendline of the wedge. It is obviously impossible at this time to automatically reset pivots and targets.

But one thing is clear to me. I am now up 69% on this long, and I have switched my thinking from protecting profits already won, to seeing if this infusion driven overnight rally draws in other interest and how far the stock might go. My loose upside target for now will be an even $20 until I get a handle on exactly how the stock price absorbs this news.

At the time of publication, Guilfoyle was long WFC, KEY equity.