Boockvar on 10 Year Treasury Yield; The Knicks Lesson

From Peter Boockvar:

To me, a most interesting price/”The Knicks reminded all of us of something important”

What I believe to be a most interesting price right now is that of the 10 yr Treasury yield at around 4.50% ish. This, even as oil prices have come right back down to about where they stood before the Middle East conflict began, as we know (though we also know that the average gallon of gasoline is currently 27% above the level in late February). On the Friday before the bombing started, the 10 yr yield was 3.94%. Its average over the past year is 4.24%. This, even as inflation expectations as implied in the TIPS market have come in sharply. The 2 yr inflation breakeven at 1.95%, is at the lowest since October 2024. The 5 yr rate at 2.25% is back to where it was last December.

Yes, the market has pivoted by pricing in a rate hike this year, with a slight chance of a second one but is Warsh and Co really going to hike with such a dramatic drop in market based inflation expectations? I really don’t believe so and even Kevin Warsh himself said last week at the central bank gathering in Sintra that “Expectations of future inflation (over the last four weeks) have come down. Inflation risks have come down.”

Are long rates rising because economic growth is robust? As growth is still around 2% with much of the contribution from data center construction, it remains quite mixed. Is it because the labor market is strong? As seen Friday, it’s just ok with pockets of strength (healthcare and social assistance still, along with construction) and holes of weakness.

This said, maybe it’s just as simple as this? On February 27th, right before the war started, the December fed funds futures were pricing in a 100% chance of two cuts this year and a 36% chance of a 3rd vs the current possibility of a hike by year end.

Or maybe this too? While the Treasury market doesn’t ‘speak’ to us directly and we can only guess and imply, I’m going to argue again that debts and deficits matter for developed bond markets around the world and just maybe excessive supply is keeping long rates elevated.

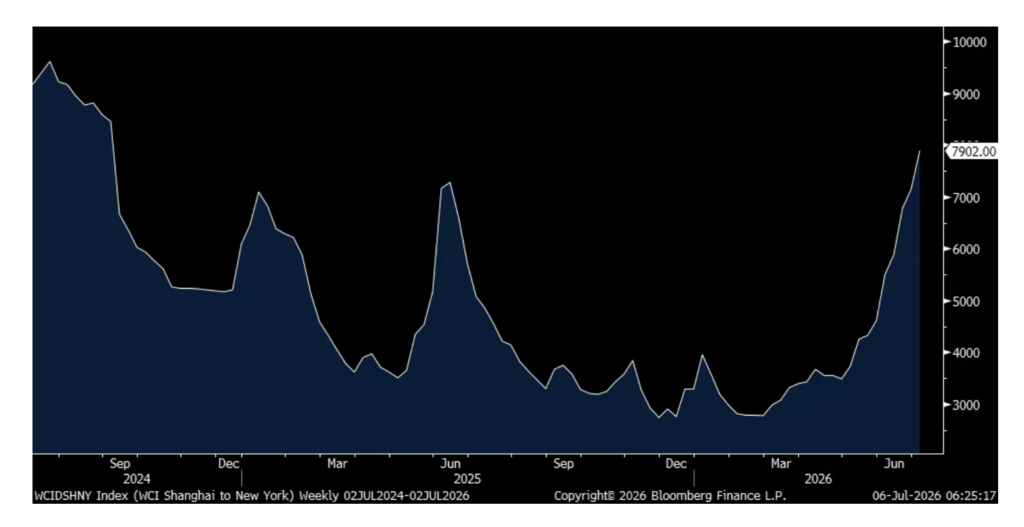

Either way, we can’t rest easily with inflation. The cost of transportation in particular keeps jumping. The World Container Index for the Shanghai to NY route rose another 10.5% last week and stands at the most expensive since September 2024 at $7,902. The journeys to LA and Europe have similar situations. I’m hearing that some of this demand are suppliers and buyers trying to get ahead of another possible round of selective tariffs.

WCI Shanghai to NY Container Price

The Journal of Commerce last week talking about the trucking market said this, “US truck shippers hoping for near term stabilization in truckload or less-than-truckload (LTL) capacity and double digit rate hikes are likely to be disappointed as structural changes to the truckload market send ripples throughout supply chains.”

In the piece they quote a senior analyst at ACT Research who spoke at a conference last week and that said “rates are accelerating still, which is incredible…It’s an extremely tight market. Maybe an acutely tight market would be a better way to describe it.”

When I read about the Meta news last week that they are using some of their excess computing capacity to sell into the market, two things came to mind. One, the moats of the hyperscalers continue to muddy with this another example of one encroaching on the businesses of others. Second, with the Meta news on the heels of SpaceX selling its excess computing power, do we now have too much computing power capacity, notwithstanding the opposite sentiment, which will eventually lead to cuts in CapEx? We’ll see.

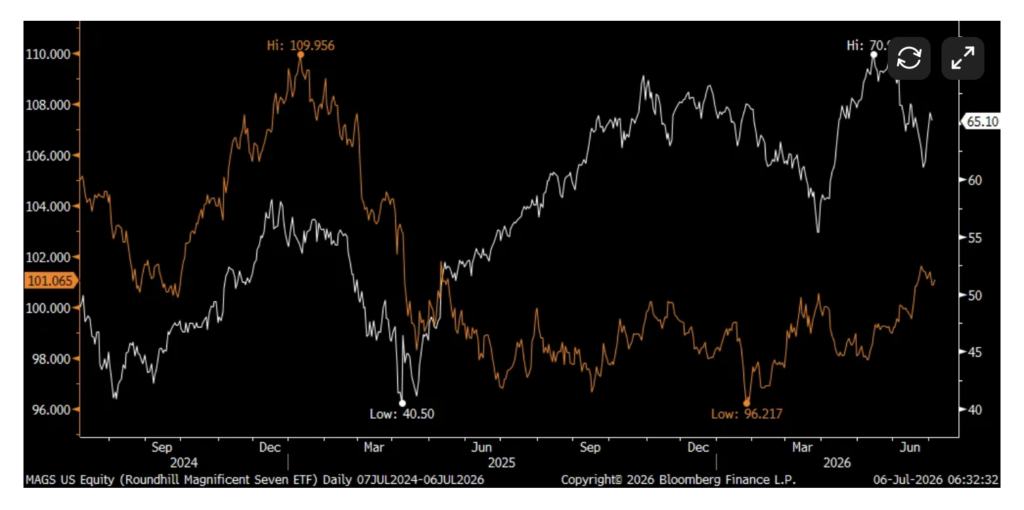

With respect to the US dollar and its direction from here, I made the point early last year that the Mag 7 stocks became essentially a reserve asset for foreign investors and some central banks that own stocks like in Switzerland and Norway. If the Mag 7 continues to underperform, which I expect as they get rerated as cash flow draining, lower return businesses, I’m curious to see whether that eventually weighs on foreign holdings of these stocks and ultimately the US dollar. That along with the big picture global trend of diversifying capital and trade flows which I expect to continue.

MAGS etf in white/DXY in orange

To a few earnings calls from last week.

From Nike, a stock we own that trades at the lowest price to sales ratio since 2009:

“We’re operating in a more complex macro environment where we’re seeing added pressure on traffic and discretionary spending across our geographies.”

“Our fourth quarter financial performance was in line with our expectations. However, the operating environment became more challenging as we progressed through the quarter. After a stronger start in March, especially in North America, by mid-April, we began to see a deceleration in retail sales trends. Our consumer is under pressure around the world, and we can particularly see it having a larger impact on Sportswear, which declined double digits in the quarter, with a similar decline in retail sales.”

The positive story is that North America is stabilizing and they have a game plan for revitalizing its China business.

As a lifelong Knicks fan who was 3 yrs old when they previously won in 1973 with no memory of that, and thus more able to enjoy every emotion of their recent championship, I liked this comparison Elliott Hill gave on the internal positioning he is executing on to best allow Nike to control what they can control.

“Earlier this month, we watched something special happen in New York. The Knicks became NBA champions; a team that had carried the weight or expectations for more than 50 years finally broke through. And when you look at what happened at the final buzzer, the trophy, the celebration, the joy across the city, it’s easy to think that’s where it was won, but it wasn’t. The championship wasn’t built on a single series or even in one season. It was built over time through setbacks and step forwards, through relationships and buying into a system where everyone knows their role.”

“You saw it when it mattered most because every one of those wins in the finals was a fight, double digit deficits. They didn’t flinch, they didn’t panic. They went to work chipping away one stop, one bucket, another stop, again and again. That’s not luck. That’s a team that’s ready. Most importantly, that’s belief, belief in their system, belief in each other. Brunson kept coming, Towns was disruptive at both ends, Hart made hustle plays, different players, one goal, all focused on closing the gap, possession by possession.”

“And that’s what I see in our team. We believe in our system and each other, in the way we’re building this. Not because the work is finished and not because every result is where we want it to be today, but because we know what it’s built on. I see the progress. I see the structural change, I see the foundation getting stronger. I see the sport offense taking hold. I see a team that’s been tested and is ready for what’s in front of us. The Knicks reminded all of us of something important. The real story is never just the celebration. The real story is everything it took to get there. And that’s exactly how we’re building Nike the right way. Because the goal is not one championship. It’s building a team that can do it again and again.” I bolded to emphasize.

From General Mills, a stock that rallied 8.5% last Wednesday after reporting and where the consumer staples stocks, many that we own, are showing signs of life as it’s hard to see them get even worse:

“What we are anticipating is that as we go into this fiscal year, the consumer is going to continue to be pressured. And we do expect to see them continue to change their behavior because of that, being more deliberate in how and where they shop, buying more on promotion and less on everyday prices, making trade-offs between pack sizes and channels, all with value at the forefront. And actually, as we exited our Q4, we saw categories slow down by about a point.”

“And so as we go into this fiscal year, we are not anticipating that to change. We expect the current consumer and category backdrop will continue. But even as we say that, we know that consumers are still willing to pay for benefits that matter most to them, think functional nutrition, bold flavors, etc…” And we know they also appreciate and search for value and many of these consumer product companies provide that.

From Constellation Brands:

“a very strong March out of the gates, and I would say in a more normalized consumer environment, a lot of great interaction with both us and the category, but particularly our brands resonating strongly. And then a massive spike in gas prices, and we did see the consumer respond by slowing down, and I think not to be unexpected, and that’s not just us. I mean, as we’ve talked to even other companies in the consumer field, traffic’s down, a lot of choices being made. And as we ended the quarter, got into the early part of this quarter, and some of those headwinds have moderated, we’ve started to see a modest re-acceleration. I wouldn’t say back to where we were in March, but a healthy return to some growth rates.”

Positions: None.

BY Doug Kass · Jul 6, 2026, 8:35 AM EDT